Insight

December 15, 2016

Trump Administration Should Prioritize Better Regulatory Information

There are a lot of big numbers in the regulatory world: trillions of dollars in costs and benefits, billions of hours of paperwork, and millions of lost jobs. But how can the public trust the numbers from federal agencies and outside sources? Many of the figures are prospective cost estimates, not real numbers like the national unemployment rate or final Gross Domestic Product figures.

With President-elect Trump’s push for regulatory modernization, getting better data, and real information from retrospective review, should help inform policymakers and lead to more effective regulation in the future. He has pledged to repeal two rules for every new regulation. Although that will be thoroughly denounced by progressives, this form of a regulatory budget is hardly novel. Both Canada and the United Kingdom have adopted similar approaches without catastrophic setbacks for public health and the environment. Unsurprisingly, conservatives and libertarians want both economic growth as well as clean air and water.

To get to a regulatory budget in the U.S., however, regulators or some outside agency will need to determine which old regulations to amend or repeal. How will they accomplish this task? President Obama signed executive orders on retrospective review, but they often resulted in additional regulatory burdens. How can President-elect Trump avoid these pitfalls? Generally, placing an emphasis on sound data and relying on experts other than the regulators themselves should help the process. For a regulatory budget to work in the U.S., regulators themselves or some other designated entity will need to find hundreds of overly burdensome or obsolete regulations that need reform. This is an incredible, but certainly not impossible, task that will require an unprecedented retrospective review effort. The good news is the flaws in the current system are well known and if there is the political will to carry the effort through, there is little stopping President-elect Trump from completing his vision for regulatory modernization.

The Obvious Flaws

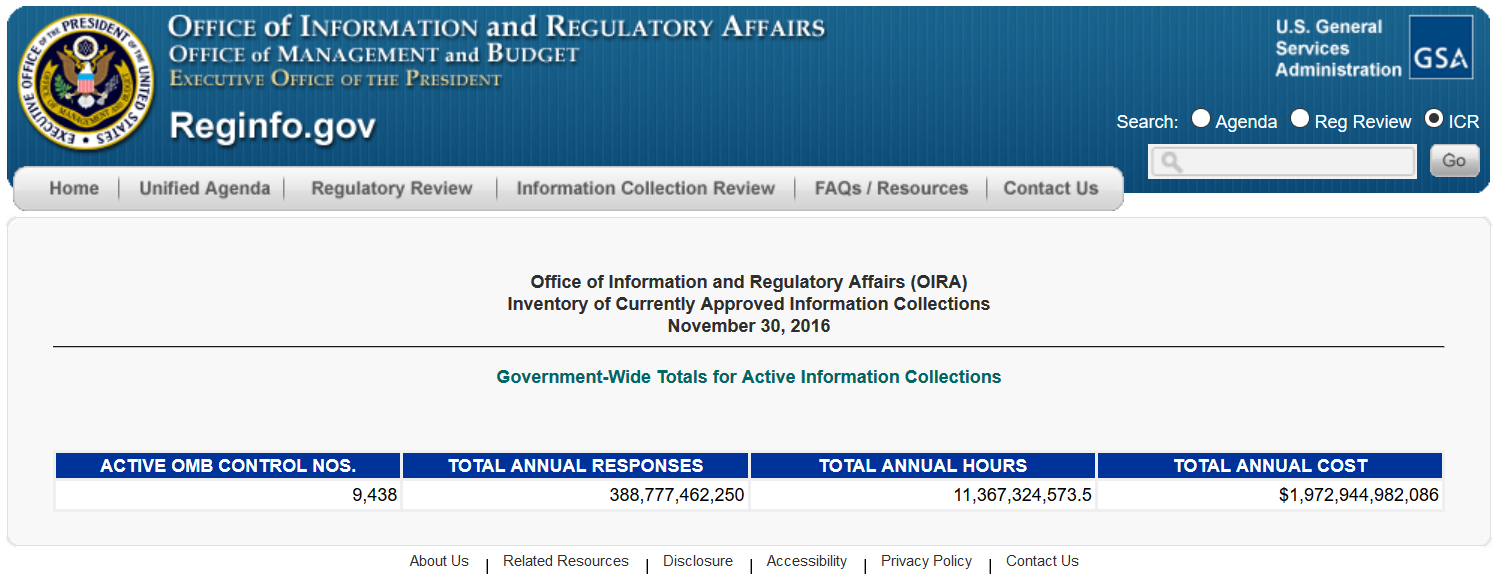

Current regulatory information is often incorrect and nowhere is this more evident than the government’s own numbers on compliance. Below, the Office of Information and Regulatory Affairs (OIRA), lists more than $1.9 trillion in annual costs from paperwork alone (forms and recordkeeping requirements).

Conservatives and libertarians might applaud, noting the administration is finally admitting regulation imposes a significant burden on the U.S. economy. After all, $1.9 trillion is more than the economic output of South Korea. Yet, former OIRA Administrator Cass Sunstein has called these figures an “urban legend.”

So why has government published this figure for months online? It is because of a mistake that was ratified on April 6, 2016, after spending just one day under review. According to IRS, the mere summary of benefits on coverage for health insurance plans costs Americans $1.7 trillion annually, up from $5 million in the previous estimate. There is little doubt the summaries, part of the Affordable Care Act, are expensive, but they aren’t equal to the GDP of South Korea, not even close.

This is a mistake, but it isn’t obvious how regulators made the mistake. In its supporting statement, which is still in track changes form, indicating there indeed was a rush, IRS lists a cost of $34.7 million for the requirement, but nowhere is there a discussion that mentions billions or trillions of dollars in potential costs. The word trillion isn’t even listed in the document. So, how did government arrive at the figure of $1.7 trillion? We don’t know, but we do recognize it’s not the only major error regulators have made in the recent past.

Recently, the Securities and Exchange Commission (SEC) approved a regulation that purportedly costs $38,000 … per hour. A simple requirement for securities brokers and dealers to maintain client records used to cost $16.9 million, from 2.7 million hours of paperwork. SEC then revised this requirement and now 2.7 million hours will cost the financial industry more than $105.9 billion, or $38,348 per hour.

As with the example above, how SEC and OIRA arrived at this exact figure is a mystery. The support document notes some compliance time might cost $400 per hour, a far cry from $38,000. In addition, with large broker-dealers, much of the compliance is automated. Nowhere in the document is a claim total compliance will cost $105 billion. There isn’t even a mention of the word “billion.” According to the analysis, “The total cost burden associated with Rule 17a-3 is approximately $44,254,361 per year.” The footnote indicates this is a combination of annual postage costs and equipment and development costs. Any hint of $105 billion in costs, a 6,270-fold increase over the previous estimate, is omitted.

Strangely, the “short statement” hints at a cost decrease from fewer public respondents. This is accurate, but again, it doesn’t explain how a relatively minor collection from slightly more than 4,000 entities could generate $105 billion in costs and impose $38,000 in hourly burdens. Either there is something OIRA and SEC are omitting or this is a grave mathematical error, both of which illustrate the paucity of accurate regulatory information today.

There is recent precedent for laughable miscalculations from regulators. In 2013, the National Credit Union Administration (NCUA) published a notice that it would impose 43 billion hours of paperwork on just a few thousand credit unions. A conservative estimate on costs would mean one requirement imposes more than $1.3 trillion in costs.

Unlike the two examples above, NCUA’s supporting statement did justify this figure with math. However, that math was grossly incorrect. After Politico highlighted AAF’s work, NCUA received calls from Capitol Hill questioning the dramatic increase. They quickly issued a correction, which AAF highlighted here. For several months, however, it went uncorrected and that error, multiplying instead of adding, drove what was supposed to be a seven-million-hour burden to more than 43 billion hours. If mistakes like this are rampant, and just in the paperwork world of regulation, how many other false assumptions and erroneous calculations exist in the 80,000 pages of rules issued annually?

Retrospective Review

President-elect Trump’s pledge to enact a form of a regulatory budget will offer his administration an opportunity to review hundreds of past major rules to determine if they are duplicative, ineffective, or if they impose more costs than benefits. This is not an easy task, but AAF’s RegRodeo offers a searchable database of more than 800 major rules that have been issued since 2005. There will doubtless be some standouts for rules that could be amended initially, but to fully implement a regulatory budget, there will need to be a more searching review of older rules and better information about previous rules that once looked good on paper but, upon further review, have demonstrated their need for withdrawal or amendment.

For example, of the five most expensive regulations issued since 2005, all but one has been discussed as a possible target for amendment or repeal. The Department of Labor’s “Fiduciary Rule” and efficiency standards for cars and heavy-duty trucks have all been mentioned as possible repeal targets. Although there are some obvious sunk costs from old regulations, those four rules would represent “on paper” repeal benefits of $268 billion. That would go a long way toward establishing a regulatory budget if those measures wind up “out” in a “one-in, two-out” regulatory budget.

Finally, retrospective review is not only important for examining past rules, but also for future success. President Obama’s executive orders called on agencies to incorporate plans for measuring the success of regulations in the future. How does the government know efficiency standards are achieving their objectives or if greenhouse gas standards are stemming climate change? Unfortunately, as the George Washington Regulatory Studies Center has found, regulators don’t often incorporate these plans or provide metrics for success. In the future, every federal agency, including independent regulators, should demonstrate to the public how they know a particular rule is effective. What are the benchmarks in years one, three, and five? How can the public know a regulation has effectively addressed a real problem in society? Answering these questions is the least the public can expect from federal regulators.

Conclusion

President-elect Trump and his cabinet secretaries have bold goals to achieve meaningful and lasting regulatory reform on the federal level. Since this has not occurred in a generation and past legislative attempts at regulatory reform have been largely toothless, the task of trimming a significant amount of red tape faces tough odds. However, it has been successful internationally, in Canada and the United Kingdom, and both President Carter and President Reagan were able to cement their regulatory reform legacies. To achieve a durable regulatory modernization for the future, President-elect Trump must utilize retrospective review and the best information available to weed out obsolete old rules and ensure regulators and the public constantly scrutinize new rules.