Insight

July 16, 2017

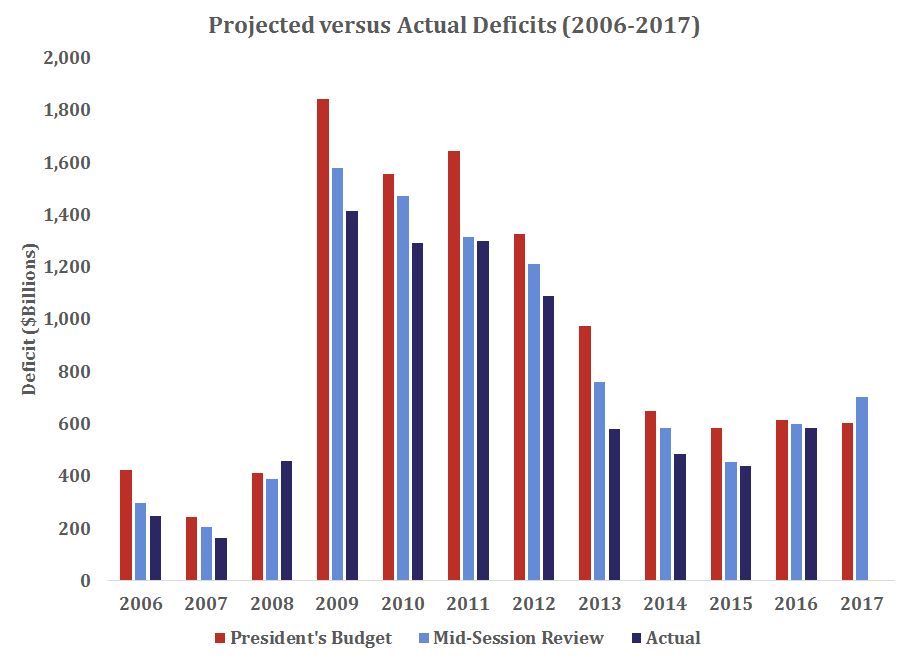

Trump OMB Bucks the Trend

On Friday, the Trump Administration quietly released the “mid-session” budget update and defied years of tradition by projecting a deficit worse than that contained in the president’s budget. Friday’s release met the July 16 deadline for updates to the administration’s budget, but it was a release the administration probably would have been happy to forgo.[1] The mid-session review projects a $702 billion deficit for FY2017, a deterioration of $99 billion from the $603 billion deficit projected in the president’s budget released just two months ago. This downward revision is remarkable in its scale, but also for its context: the mid-session review has always projected a better deficit than that projected in the president’s budget.

It appears to have been bipartisan “company policy” at the administration’s Office of Management and Budget (OMB) to build in a little room for a positive deficit surprise in the mid-session review, and for an end of year deficit figure that’s a little better still. As the chart below demonstrates, in recent history, the mid-session review has projected a lower deficit than that contained in the president’s budget every single time. With one exception, the actual deficit has ended up being even lower than the deficit projection in the mid-session review – essentially allowing 23 opportunities for administrations to claim that the deficit was lower than predicted. That one exception was at the end of the Bush Administration when the economy was taking a dive beyond any cushion that OMB would have given itself. Friday’s release broke that streak, and did so by a country mile – nearly $100 billion or over 16 percent of the deficit projected in the president’s budget.

The explanation for this large revision lies in lower actual tax receipts than those projected in the president’s budget. Regardless of the reason for the big miss in the administration’s initial deficit projections, it belies the fact that the U.S. budget is awash in red ink and absent fundamental policy reforms will remain so. It has been tradition that following the “good news” in the mid-session review, the year-end actual deficit number is even better. If anything, the “surprise” in Friday’s budget release means that the FY2017 deficit is as likely to worsen than it is to get better.

[1] 31 U.S. Code § 1106