Insight

February 29, 2016

What Is the Real Economic Impact of TPP?

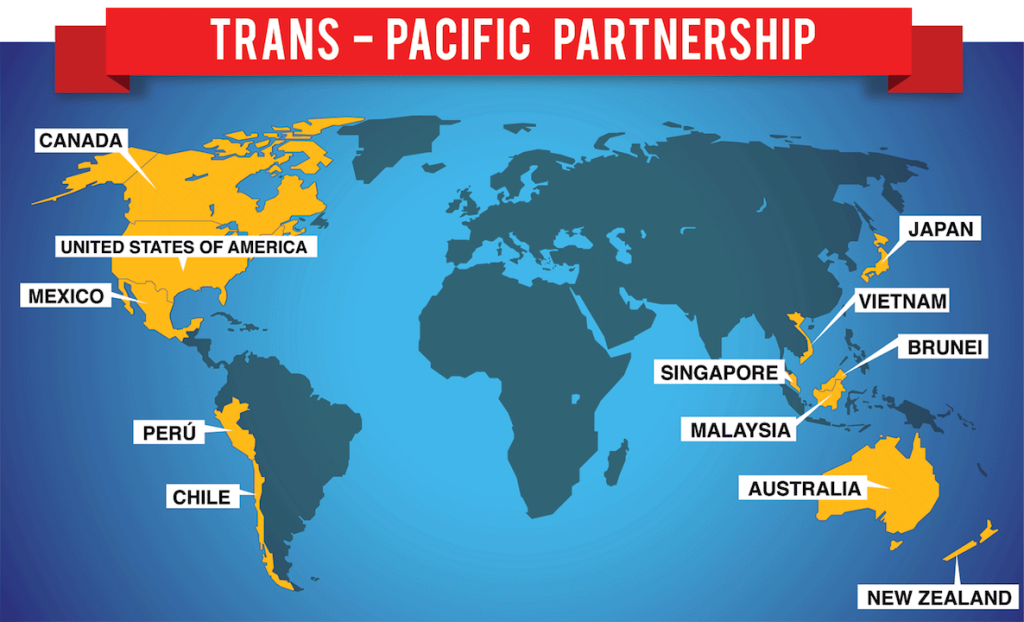

The Trans-Pacific Partnership (TPP) if ratified would be the largest trade agreement in history. As a part of the Obama Administration’s “pivot to Asia,” TPP lowers trade barriers between the U.S., Japan, and 10 other nations on the Pacific Ocean. Nearly 75 percent of goods tariffs would be eliminated immediately after TPP comes into force, with 99 percent eliminated over 30 years. Arguably more significant would be TPP’s impact on non-tariff and foreign direct investment (FDI) barriers, such as regulations and trade quotas, that particularly impede services trade.

There have been many attempts to estimate TPP’s potential economic impact on the United States. Before the deal was finalized, the United States Trade Representative speculated that by 2025 TPP could raise the national income by $77 billion per year and boost exports by $124 billion. These estimates, which came from a 2012 study by the Peterson Institute for International Economics (PIIE), were recently updated to reflect the final details of the agreement. PIIE’s new analysis found that, by 2030, the U.S. can expect annual income gains of $131 billion and export gains of $357 billion. This equates to a 0.5 percent increase in GDP. Delaying a TPP vote by just one year, they suggest, would result in $94 billion in lost revenue for the U.S. economy.

Another study, performed by researchers at Tufts University, found precisely the opposite: TPP would be responsible for a 0.5 percent decrease in GDP by 2025. They also project nearly 450,000 U.S. job losses and a consequent rise in income inequality, represented by a decrease in labor’s share of total income.

Activists on both sides of the TPP debate have cited these studies in their advocacy efforts. And both PIIE and Tufts University have provided commentary defending their study against the other. Since these scenarios cannot both be true, how do we know which one to believe?

To thoroughly answer this question, each study’s methodology should be evaluated to determine which model is more realistic. While PIIE assumed that the labor market is flexible and that the U.S. economy would trend toward full employment over ten years, the Tufts University researchers made no such assumptions. Instead, they expected a drop in domestic production to result in job losses that would not be replaced in other sectors of the economy. And while researchers from Tufts University utilized a Global Policy Model to estimate the macroeconomic impacts of shifting trade volumes, PIIE employed a different model designed to project global growth and trade in response to lower non-tariff barriers, higher FDI, and increased specialization.

Economic models are built on assumptions that drastically influence the results. Even if a consensus can be reached on the general economic effects of TPP, future changes to the agreement and fluctuating global conditions make it difficult to forecast its exact impact. It may however be wise to examine how other nations have fared under free trade. In China, for instance, 680 million people have been lifted out of poverty since the country opened itself up to trade in 1979. Chile instituted its own free market, pro-trade reforms in the 1980’s and saw a similar reduction in poverty. The story is the same: foreign trade allows for more efficient, specialized production that enables nations to begin accumulating greater wealth.

Economic forecasts are tricky. Differences in methodology and ideological assumptions have allowed for two competing theories on TPP to surface, with findings that are completely contradictory. However, if history is any indication, expanding free trade will most likely benefit all parties involved. TPP is expected to spark significant economic growth in poorer nations that would open their markets to foreign competition for the first time, and its potential benefits for the U.S. should not be discounted.