Research

November 10, 2021

Key Health Policy Provisions of the Build Back Better Act

Executive Summary

The House of Representatives could vote as early as next week on the Build Back Better Act (BBBA). The BBBA contains a vast array of health policies and spending. This paper highlights some of the most significant health-related provisions.

- The BBBA expands who is eligible for Affordable Care Act premium tax credits (PTCs) and makes those PTCs more generous for everyone. According to the American Action Forum’s (AAF) Center for Health and Economy, these policies would increase the number of insured individuals by 2.2 million in 2022, increasing to 3.9 million in 2025 relative to current law, and would cost $272 billion over those four years. The coverage gains would, however, evaporate in 2026 without further congressional action.

- In a series of last-minute negotiations, Democrats added a number of policies aimed at reducing prescription drug spending to the BBBA legislation. Significantly, the BBBA would allow the Secretary of Health and Human Services to directly negotiate what Medicare pays for drugs for the first time. The details of the proposal make it abundantly clear, however, that this negotiation will amount to little more than government price-fixing.

- The BBBA includes long-sought reforms to the Medicare prescription drug benefit—originally put forward by AAF in 2018—aimed at realigning insurer and drugmaker incentives to hold down Part D costs, and capping Part D beneficiaries’ out-of-pocket spending on drugs.

Introduction

The House of Representatives could vote as early as next week on the Build Back Better Act (BBBA), which is expected to total somewhere between $1.75 trillion to $2 trillion in new spending. The BBBA contains an expansive set of health care policies ranging from a series of initiatives addressing maternal mortality, to a permanent reauthorization of the Children’s Health Insurance Program, to roughly $150 billion in new funding for home health care.

The provisions drawing the most attention are expansions of the Affordable Care Act’s (ACA) premium tax credits (PTCs) paired with an attempt to close the Medicaid coverage gap; a last minute, poorly understood—and arguably poorly crafted—set of policies seeking to constrain drug prices; and reforms to the Medicare Prescription Drug Benefit (Part D) realigning incentives for manufacturers and insurers and capping beneficiary costs. Also noteworthy are the relatively paltry changes to Medicare more broadly, which were scaled back from initially seeking to lower the Medicare eligibility age to 60, to expanding fee-for-service Medicare coverage to hearing, dental, and vision services, to now adding only a limited hearing benefit.

ACA Premium Tax Credit Expansions

The BBBA includes several health policy provisions impacting the individual health insurance market and attempting to extend health coverage to individuals residing in states that have not taken up the ACA’s Medicaid expansion, which the American Action Forum’s (AAF) Center for Health and Economy (H&E) estimates would increase the number of insured individuals by 2.2 million in 2022, increasing to 3.9 million in 2025 relative to current law, at a cost of $272 billion over those three years. The specific provisions are detailed below.

Making Permanent the Enhanced Individual Market Premium Tax Credits

Under the ACA, an individual or family’s PTC for individual market insurance coverage is adjusted based on their household income and the cost of the second-lowest cost Silver plan in their rating area. An individual’s subsidy must be large enough to ensure that he or she does not pay more than a specified percentage of income (detailed in columns 2 and 3 of Table 1), based on household income relative to the federal poverty level (FPL). The American Rescue Plan Act (ARP) reduced these percentages to increase the size of the premium subsidy for 2021 and 2022, as shown.

Table 1.

| Income | 2021 (pre-ARP) | 2021 & 2022 (Current Law) |

| < 133% FPL | 2.07% | 0% |

| < 150% FPL | 3.1% – 4.14% | 0% |

| < 200% FPL | 4.14% – 6.52% | 0% – 2% |

| < 250% FPL | 6.25% – 8.33% | 2% – 4% |

| < 300% FPL | 8.33% – 9.83% | 4% – 6% |

| < 400% FPL | 9.83% | 6% – 8.5% |

| > 400% FPL | N/A | 8.5% |

Under the ACA, subsidies are only available to those making up to 400 percent of FPL; however, the ARP also allowed households with income above 400 percent of the FPL to receive ACA subsidies in 2021 and 2022. The BBBA proposal would extend these policies three years, through 2025. H&E projects that these provisions would increase the number of people enrolled in subsidized individual market coverage by 1.2 million in 2023, 1.4 million in 2024, and 1.7 million in 2025, at a cost of $20-$21 billion annually relative to current law, before reverting to the baseline in 2026.

Closing the Medicaid Coverage Gap

As of January 2021, an estimated 2.2 million individuals under 100 percent of FPL reside in Medicaid non-expansion states and did not have access to any government assistance for health coverage. In order to extend coverage to this population, Democrats initially proposed establishing a new, entirely federally funded and operated Medicaid-like program beginning in 2025 to cover the expansion population in the 12 states that have not expanded. In the interim, for plan years 2022, 2023, and 2024, the BBBA originally aimed to extend eligibility for zero-dollar premium, individual market coverage to that population.

After pushback from Senator Joe Manchin (D-WV), and amid concerns about getting the program off the ground, the long-term solution of a new, federal Medicaid program has been scrapped, and the legislation instead focuses on providing the coverage-gap population with fully subsidized, individual market insurance coverage through the ACA for four years. H&E finds that covering the 2.2 million individuals in the Medicaid coverage gap through subsidized individual market coverage from 2022-2025 would cost $211 billion relative to current law.

Reinsurance

The BBBA would provide $10 billion in annual funding to the 50 states and the District of Columbia to be used either to establish a state reinsurance program or to provide financial assistance to reduce out-of-pocket (OOP) costs. States would be automatically approved for funds unless the Department of Health and Human Services (HHS) otherwise intervenes, and approval would last for five years unless revoked by HHS for unapproved use. If a state does not apply, HHS would operate a reinsurance program in the state. Non-Medicaid expansion states would not be able to apply for this funding, but HHS would operate reinsurance programs during those plan years.

Impact of ACA Premium Tax Credit Expansions

Collectively these provisions would create a new coverage cliff, as H&E modeling shows that both coverage and spending would revert to current law in 2026. This would leave the same populations the BBBA is intended to help back where they were in 2020 come 2026. It would be left to the 119th Congress and whoever occupies the White House after the 2024 presidential election to address this new coverage cliff.

Drug Pricing Policies

Though left out of the agreement negotiated between the White House and Senate moderates initially, in recent days several policies aimed at restricting the prices of prescription drugs have been added to the BBBA legislative text. These policies have continued to change with some frequency amid intense negotiation, but House Democrats seem to have settled on the following policies.

Medicare Negotiation of Drug Prices

Democrats, and some Republicans, have long championed the idea that Medicare should negotiate directly with manufactures for discounts on prescription drugs; Medicare is explicitly prohibited from doing so under current law, however. While this seems illogical, the prohibition exists because Medicare would not have the leverage to obtain discounts in a traditional negotiation. In the Medicare Part D program, plan sponsors negotiate with manufacturers for discounts in exchange for formulary placement, and beneficiaries can pick between dozens of plans to find a formulary that meets their specific needs. Since Medicare has no drug beneficiaries itself and does not restrict access to a limited subset of drugs, the program has no leverage to negotiate additional discounts. Similarly in Part B, drug discounts can only be negotiated if Medicare were to restrict access to certain drugs to incentivize price cuts. Restricting access to treatments has long been a political impossibility, making negotiation something of fool’s gold.

The BBBA would get around this obstacle by effectively forcing manufacturers to sell their drugs at government-set prices. Under the proposal, beginning in 2025, the Secretary of HHS would be authorized to “negotiate” the prices of up to 10 “negotiation-eligible drugs.” In 2026 and 2027, the cap increases to 15 drugs annually, and rises to 20 drugs in 2028 and beyond. Part B drugs would be exempt until 2027. All insulin products would be able to be negotiated in addition to the stated yearly caps.

A negotiation-eligible drug is a small-molecule or biologic (including authorized generics) treatment that has had Food and Drug Administration (FDA) approval for at least seven years for a small-molecule drug or 11 years for a biologic—these numbers have shifted several times in recent days—that is among the 50 single-source drugs with the highest total expenditures in Part B or Part D. Orphan drugs or “low-spend” drugs are excluded, with low-spend being defined as a drug or biologic on which Medicare spends less than $200 million annually (adjusted by the consumer price index in future years). The reduced prices would be effective after an additional two years, meaning small-molecule drugs would have prices reduced 9 years after approval and 13 years for biologics.

The BBBA would set a ceiling for negotiated price of between 40-75 percent of the non-federal average manufacturer price (AMP), scaling down depending on how far the drug is past its initial exclusivity period. Of note, however, and a significant change from even Speaker Pelosi’sH.R. 3 proposal, there would be permanent floor below which the government could not demand further price concession. In 2028 and 2029, there would be a temporary floor of 66 percent of the non-federal AMP for select small biotech companies.

Unlike H.R. 3, the negotiated price would not be applied to the private health care market, but the negotiated rate or “maximum fair price” would be made publicly available.

Perhaps the most significant provision in terms of long-term impact is the establishment of an excise tax on drug sales. To address the lack of leverage the secretary would have in negotiations, the legislation would implement this excise tax specifically on sales of a drug which the secretary has targeted for negotiation but for which the manufacturer has not agreed to the secretary’s target price. The excise tax would be applied for any period in which the manufacturer is in “non-compliance.” The tax would start out at 65 percent of the sales for the first 90 days of non-compliance, increasing at regular intervals until topping out at 95 percent for any period of non-compliance beyond 270 days.

Inflation Penalties

The BBBA would aim to prevent drug manufacturers from increasing their prices faster than the rate of inflation, a frequent complaint of advocates for drug pricing reform. Under Part B, if a drugmaker’s price increases faster than inflation—pegged to September 1, 2021 and adjusted by CPI-U for each quarter thereafter—the manufacture would pay a penalty of 106 percent of either the average sales price or the wholesale acquisition cost for the calendar quarter (whichever is less) times the total number of billing units sold, excluding Medicaid. Under Part D, the rebate will be set as the total number of units sold (excluding Medicaid) multiplied by the amount by which the annual manufacturer price exceeds the CPI-U adjusted allowable payment amount.

Inflation rebates would not be included in calculating Medicaid Best Price or the Average Manufacturer Price. And under both Part B and Part D manufacturers face civil monetary penalties for delays in paying their inflation penalties.

Insulin Policies

The BBBA specifically targets insulin prices, making all insulin products subject to Medicare negotiation regardless of whether the product would otherwise be subject to negotiation.

Under Medicare Part D, the BBBA would limit cost-sharing for insulin to $35 per month.

Additionally, the BBBA would intercede in the group and individual insurance markets to limit patient insulin costs. Starting in 2023, health insurers offering group or individual health insurance coverage would be required to provide coverage for at least one of each insulin dosage form (vial, pump, or inhaler) of each type of insulin (rapid-acting, short-acting, intermediate-acting, long-acting, and premixed). Further plans would be required to limit patient costs for insulin to no more than either $35 for a 30-day supply, or an amount equal to 25 percent of the negotiated price of the insulin product for a 30-day supply—net all price concessions—whichever is lower.

Implications of BBBA Drug Pricing Policies

The BBBA seeks to constrain the cost of prescription drugs for patients and reduce federal spending—, but without curtailing access to treatments for patients. This is a circle that simply can’t be squared. The BBBA diverges from Democrats’ past drug pricing proposals in several ways, but despite the framing of these changes as compromises, in many cases they have exacerbated the problems of past proposals. For example, unlike H.R. 3—a fundamentally flawed proposal that would have also wreaked havoc on pharmaceutical innovation—the BBBA does not set a floor for the price Medicare can require of drug manufacturers. Under H.R. 3, the secretary and manufacturers were required to negotiate a price no greater than 120 percent of an Average International Market (AIM) price. But while 120 percent of AIM served as a price ceiling, the secretary was also required to accept any offered price below AIM, in effect setting a floor for negotiations of 99 percent of the AIM price. Under the BBBA, the ceiling price could drop as low as 40 percent of the AMP, but there would be no floor below which the secretary cannot force the manufacturer to go. Paired with the 95 percent excise tax for failure to agree on a negotiated price, manufacturers would have absolutely no leverage to prevent the secretary from arbitrarily picking any price.

Additionally, by allowing government price-setting for small molecule drugs with more than seven years of exclusivity and biologics with more than 11 years of exclusivity, the legislation would undermine many of the incentives that have led to broader application of existing therapies to additional conditions. Manufacturers would be disinclined to expend the resources necessary to obtain FDA approval for new indications if the price of the drug is limited to the lower, government-set price, particularly for small patient populations where there is no chance to make up the costs through volume. Additionally, the legislation could have a detrimental impact on biosimilar and generic development. Companies considering bringing a generic or biosimilar product to market may not be able to undercut the government-set price of the reference product enough to obtain market share sufficient to offset the costs of bringing the generic to market. This could also have negative impacts on the group and individual markets where plans will not be paying the lower Medicare price and will have fewer generic and biosimilar options to drive down prices overtime.

Medicare Part D Reforms

The BBBA also undertakes a significant redesign of the Medicare Part D program, beginning in 2024, aimed at realigning plan and manufacturer incentives to constrain drug prices and to limit beneficiaries’ OOP costs. The broad framework of the proposal was originally outlined by AAF’s Tara O’Neill Hayes in 2018, and has garnered bipartisan support, while there have been partisan differences over some of the details.

AAF’s Proposal for a Part D Redesign

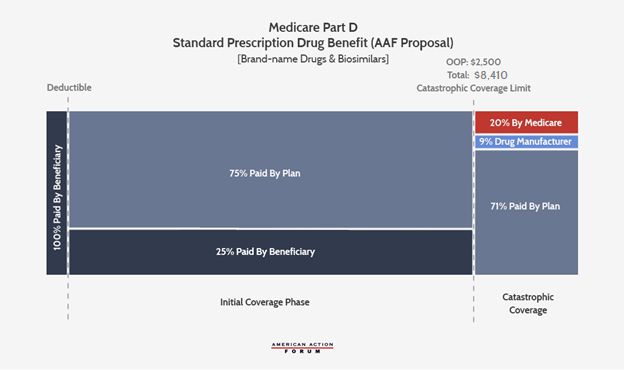

The original Part D redesign proposed by AAF would impose a beneficiary OOP cap, considering various thresholds ranging from $2,500 to $4,000. The proposal would eliminate the coverage gap and move manufacturer liability to the catastrophic phase; the new manufacturer liability would equal 9 percent of all costs for brand-name drugs and biosimilars in the catastrophic phase. Government reinsurance would fall to 20 percent and insurer liability in the catastrophic phase would increase to 71 percent for brand-names and biosimilars. This proposal did not specify whether government reinsurance or insurers would be responsible for the remaining 9 percent liability for generic drugs, though past insights have commented on the benefits of having insurer liability equal for generics and brand-name drugs.

Build Back Better’s Part D Redesign

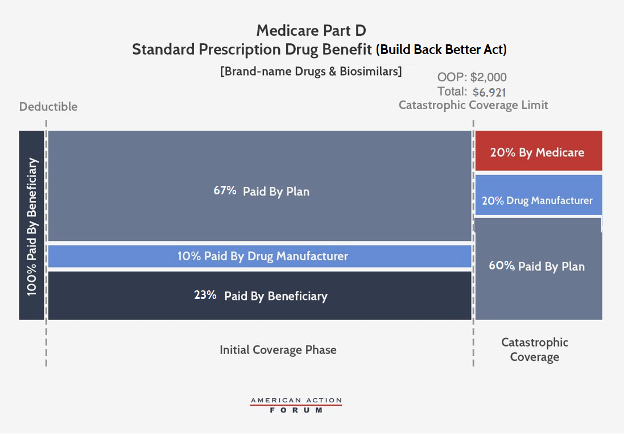

Under the BBBA, brand-name and biosimilar drug manufacturers would become liable for 10 percent of costs in the initial coverage phase and 20 percent in the catastrophic phase. Government reinsurance would fall to 20 percent for brand-name drugs and biosimilars and to 40 percent for generic drugs. Insurer liability in the catastrophic phase would increase to 60 percent for all drugs. The catastrophic phase would begin at $2,000 in OOP costs, capping beneficiary costs at that point, just as in H.R. 3.

The BBBA would also reduce beneficiaries’ coinsurance liability to 23 percent in the initial coverage phase (from 25 percent currently) and their premium liability to 23.5 percent (from 25.5 percent currently). Consequently, the federal premium subsidy rate would rise to 76.5 percent (from 74.5 percent) and insurer liability in the initial coverage phase will be 77 percent for generic drugs and 67 percent for brand-names and biosimilars.

Last, the BBBA would allow for beneficiaries’ OOP costs to be “smoothed” over the course of the year, rather than potentially having to pay as much as $2,000 in a single month.

While the BBBA version of the Part D redesign retains the 10 percent manufacturer share in the initial coverage phase that was added in the H.R. 3 version of the proposal, the legislation would lower the manufacturer share in the catastrophic phase from 30 percent in H.R. 3 to 20 percent, while AAF initially proposed 9 percent (note that AAF used 9 percent because that was determined to be the rate at which pharmaceutical companies would be responsible for the same level of costs—at the time the original analysis was done, while AAF was neutral on whether manufacturers’ share of costs should increase).

Implications of the BBBA’s Part D Redesign

The $2,000 OOP threshold will be significantly less than what beneficiaries are expected to pay before moving into the catastrophic phase under current law. By 2024, the catastrophic threshold is currently expected to be $7,800; beneficiaries reaching catastrophic coverage would spend $3,250 OOP to get to that threshold, at which point they become responsible for just 5 percent of any remaining costs.[1] With a $2,000 OOP limit, total spending to reach that threshold (with the expected $530 deductible and 23 percent coinsurance) would be $6,921. Thus, relative to current law, the $2,000 OOP limit would be expected to save beneficiaries who would have reached the original threshold at least $1,250; in 2019, 1.5 million beneficiaries reached this point.[2] Beneficiaries with as much as $900 less in spending—who wouldn’t have reached the current law threshold—would also surpass $2,000 OOP and see savings, as well. The lower OOP limit also has implications for each stakeholders’ liability in the catastrophic phase—particularly drug manufacturers. More beneficiaries will reach the catastrophic phase and a greater share of overall costs will occur in that phase, meaning the higher 20 percent liability for manufacturers will apply to more drug costs than what is currently spent in the catastrophic phase.

The Incredible Shrinking Medicare Expansion

The BBBA—at least in its current form—would not lower the Medicare eligibility age, nor would it expand fee-for-service (FFS) Medicare coverage to dental or vision services. The legislation does, however, provide a new hearing benefit in Medicare FFS. (It is worth noting that Medicare beneficiaries can already access comprehensive vision, dental, and hearing services by enrolling in a Medicare Advantage plan).

Beginning in 2023, Medicare will cover audiology services, and the BBBA would authorize coverage for specific types of hearing aids designated by the Secretary of HHS with a prescription from a hearing specialist. The benefit would be limited to one hearing aid per ear, per 5-year period.

Conclusion

In sum, the BBBA would grossly enlarge the federal footprint in health insurance by expanding access to taxpayer-funded premium tax credits at both ends of the income ladder, while making those subsidies much more generous and therefore expensive. The Congressional Budget Office has argued that the expansion of ACA PTCs into higher-income populations and the increased generation of the subsidies will lead to many employers dropping health insurance coverage and denying their employees the option to retain their existing coverage. But because of the time-limited nature of these policies, millions of Americans will face a coverage cliff in 2025 when, having become dependent on the federal government for subsidized coverage, those subsidies will lapse.

The BBBA would further insert the federal government into the private market by establishing government price-setting in Medicare, with potentially dire consequences downstream for access to follow-on treatments in the private market due to distorted incentives, fewer new therapies, and reduced incentives for drugmakers to document new indications for existing therapies.

The BBBA falls far short of progressive goals to expand Medicare eligibility and benefits, but advocates can take heart that beneficiaries can access vision, dental, and hearing services through Medicare Advantage.

Finally, the BBBA would undertake some positive reforms of the Medicare Part D program, realigning incentives to control drug spending in the program and protecting beneficiaries from endless OOP costs in a manner that has received largely bipartisan support, and that is based on a proposal originally circulated by AAF.

The BBBA scores well on the last point, but the needed Part D reforms are insufficient to make up for the detrimental health policies strewn throughout the bill.

[1] https://www.cms.gov/files/document/2021-medicare-trustees-report.pdf

[2] https://www.kff.org/medicare/issue-brief/millions-of-medicare-part-d-enrollees-have-had-out-of-pocket-drug-spending-above-the-catastrophic-threshold-over-time/