Research

September 25, 2020

Severance Taxes: A Case Study Analysis of Alaska’s Ballot Measure 1

Executive Summary

- Of the 34 states that have severance taxes – essentially production taxes paid by private energy producers – Alaska is particularly reliant on them.

- Alaskans will vote on a ballot initiative in November, Ballot Measure 1, which would increase the effective tax rate on oil per barrel by an average of 188 percent at a time when global oil markets are severely distressed.

- This tax increase would reduce future investment activity by over 14 percent.

- The reduced investment would risk the jobs of over 6,300 workers directly and indirectly employed by petroleum producers.

Introduction

Among its other wide-ranging economic impacts, the COVID-19-related recession resulted in an unexpected and significant decline in oil and gas demand. Coupled with the long-term prospects for fossil fuel extraction, this demand decline may lead states that impose severance taxes on oil and gas production – essentially production taxes paid by private energy producers to the government – to enact minimum severance taxes to ensure consistent revenues. A previous American Action Forum paper discussed the short-sightedness of reliance on severance taxes, and this paper discusses in detail the important case study of Alaska.[1] A ballot initiative seeking to raise oil taxes in that state illustrates the problems and challenges inherent in severance taxes.

In August of 2019, an advocacy group filed an application with the State of Alaska to put an initiative to raise taxes on Alaska oil production on the ballot for Alaska’s general election this November. Alaska is the only state that does not have a sales or income tax, but rather relies substantially on taxing petroleum production and related earnings. The Alaska economy in general relies substantially on the oil and gas industry, with as much as a quarter of the state’s wage and salaried workers tied to this industry. Accordingly, both the state’s fiscal picture and economy are uniquely exposed to policies and market forces affecting the oil and gas industry.

This study examines the major elements of the proposed tax and estimates the effective tax changes on Alaska oil production. Based on the relevant literature, it further assesses the effect of this tax on Alaska workforce and oil production activity. It finds that the tax would reduce employment by over 6,300 workers, suppress investment activity by 14 percent, and deliver less than half of the revenue supporters have previously claimed.

Policy

In November, Alaskans will vote on two ballot initiatives, one concerning primary elections, and the other on raising taxes on Alaska oil producers. Ballot Measure 1, or “190GTX,” in election legalese, would make several changes to the current state oil production tax regime. Under current law, Alaska depends substantially on royalties and corporate, property, and production taxes on the oil and gas industry to fund government services. In fiscal year (FY) 2019, the State of Alaska collected $2.043 billion in petroleum revenue, which comprised 38 percent of funding for the state’s general fund. 53 percent of the general fund revenue arose from a transfer from the state’s Permanent Fund.[2] As these figures show, oil revenue does not cover government expenses, and it has been insufficient to fund government programs since FY 2014. From FY 2010 to FY 2014, petroleum revenues contributed an average of about $6.4 billion. Due to a collapse in oil prices, however, from FY 2015 through FY 2019 petroleum revenues contributed an average of about $1.5 billion.

The most significant tax on oil production in Alaska is the production tax.[3] Oil and gas produced and sold from lands within Alaska are subject to this “severance” tax. The tax applies to oil and gas produced from any area within the boundaries of the state. The tax only applies to petroleum sold by producers, so it excludes state royalties and certain other exclusions.

The current production tax is a multi-tiered levy that includes an alternative gross minimum tax and a net production tax against which certain costs can be deducted or otherwise credited. Essentially, a 4 percent tax is applied to what is known as the gross value at the point of production when the price of oil is greater than $25 per barrel. This is the value of taxable oil – the production taxes do not apply to royalty barrels and other exempt production – less transportation costs. 4 percent of this value is subject to the gross minimum tax. This is a “gross” tax because, unlike a conventional income tax, producers may not deduct the costs of production. This tax, however, is only an alternative minimum tax, designed to ensure some revenue is collected from petroleum producers irrespective of investment and other costs that are otherwise deductible.

Once a producer calculates this potential liability, it must also determine its liability under the net production tax, which allows for deductible expenses, such as lease operating expenditures and capital investment. The value of taxable oil produced, net of these deductions, is known as the production tax value, against which a 35 percent tax rate is applied to determine a producer’s liability under the net production tax. Credits may be applied by eligible producers to reduce the ultimate tax liability.

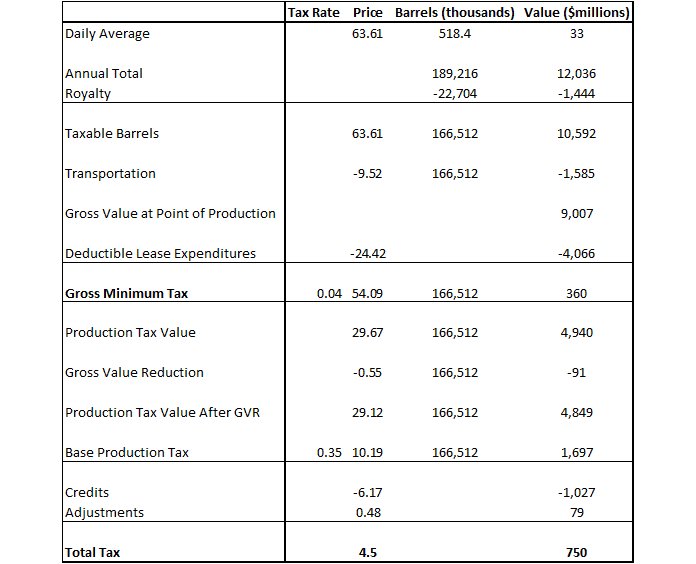

The worksheet below provides a determination of FY 2018 production tax revenues in the aggregate. Based on the calculation below, the net tax calculation results in $750 million of tax, which is greater than the gross minimum tax calculated at $360 million.

FY 2018 Production Tax Calculation[4]

Ballot Measure 1

Under the proposed ballot measure, new taxes would apply to North Slope “fields” (north of the 68th parallel) that have cumulative production in excess of 400 million barrels and in the prior calendar year produced in excess of 40,000 per day. This production includes Alaska’s aging legacy fields (Prudhoe, Kuparak, and Alpine) and has been estimated to cover 80-90 percent of all Alaska oil production.[5]

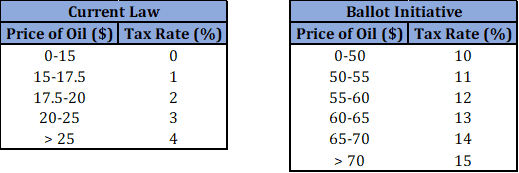

These new taxes would apply at multiple levels of the Alaska production tax regime. First, this proposal would implement an alternative gross minimum tax of 10 percent (up from 4 percent) on production when prices are below $50 per barrel, rising at a rate of one percent for every $5 increment above $50 per barrel, to a maximum of 15 percent for prices at or above $70 per barrel. As under the current gross minimum tax, production costs are not deductible under this tax.

Proposed Ballot Measure Minimum Tax Structure[6]

In addition to increasing the minimum tax, the proposal would apply 15 percent of additional production tax on the difference between Production Tax Value and $50, if the Production Tax Value is greater than $50 per barrel.

The proposal would eliminate Alaska’s per-barrel credit, among other provisions.

It is important to note that there is a great deal of uncertainty that attaches to the practical implementation of the proposal as drafted. Alaska’s attorney general observed that the measure is “difficult to interpret and raises a number of implementation and constitutional questions,” before proceeding to document a number of drafting and legal concerns.[7] Two analytic firms engaged by the state legislature reached similar conclusions.[8] In a presentation to the state legislature one of the firms observed, “in general, the initiative lacks necessary specificity, making it improbable that a common interpretation could be reached.” Last, the state Office of Management and Budget examined the proposal and found that it would cost the state over $8 million to implement the proposal were it enacted. Most of these costs would be borne by the Department of Revenue, which expects it “will take at least one year and most likely longer” to implement the proposal and cost the department $7.5 million in new programming, testing, auditing, personnel, and technology costs.[9]

Alaska and the Petroleum Economy

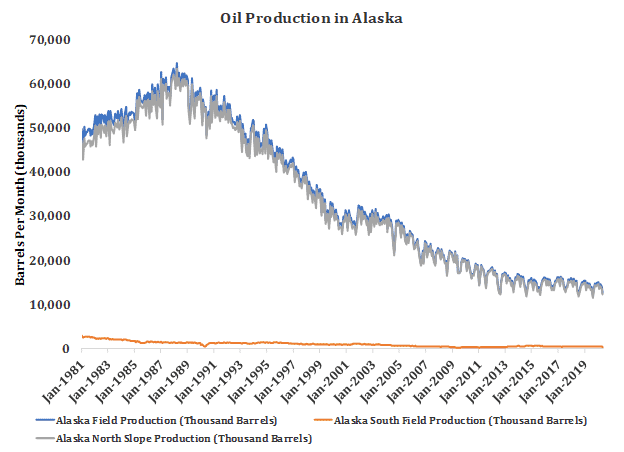

Alaska is home to both onshore and offshore drilling on lands subject to state and federal jurisdiction. A large majority of oil produced in Alaska is extracted from the North Slope, as can be seen in the chart below, a geographic area lying north of 68 degrees north latitude that includes the oil fields impacted by the ballot initiative.

Source: U.S. Energy Information Administration

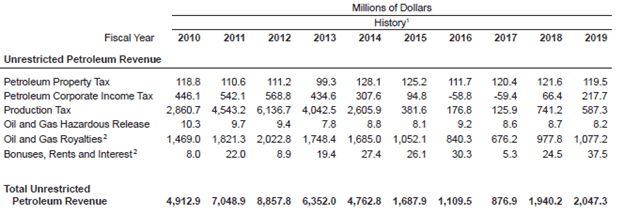

Since the 1950s, oil has been produced in Alaska and its production has been subject to state production taxes. These taxes, in combination with royalties, property tax, and income tax, have proven to generate a significant portion of Alaska’s unrestricted general fund revenues, up to 80 percent. In recent decades, production in Alaska has declined. In late 2014, oil prices began declining, bottoming out in early 2016 after falling from over $110 per barrel to $30 per barrel. As a result, annual unrestricted revenue to the state declined from $4.9 billion in 2010 to under $0.9 billion in 2017, as seen in the table below.[10]

Alaska Unrestricted Petroleum Revenue

Source: Alaska DOR 2019 Fall Revenue Source Book

Several years of oil production and price growth were stalled in 2008 with the onset of the Great Recession. In the years that followed, the Shale Boom resulted in increased production throughout the continental United States. Reduced prices in Alaska, however, brought on a second wave of recessionary effects in 2015 due to a marked decline in revenue compared to the previous year, as can be seen above. While Alaska has since seen some recovery, the full effects of the COVID-19 pandemic have yet to be seen. Demand for oil plummeted in the spring of 2020, and futures prices hit historic lows due to the shelter-in-place orders throughout the world. Growing quantities of oil and refined products were no longer consumed by the transportation sector as commuting and air traffic steeply declined. Simultaneously, Saudi Arabia and Russia increased the quantities of oil they were bringing to market, creating a supply glut that led to historically low negative futures prices. Russian and Saudi flooding continued until the Organization of the Petroleum Exporting Countries as well as the United States and others came to an agreement to reduce production, and since then the market has recovered.

Oil Employment in Alaska

Between 2015 and 2018, the Alaska economy lost 11,700 jobs due to the recession, of which 4,800 were oil and gas industry jobs. In 2018, the “primary” companies engaging in oil production and transportation in Alaska, as defined by a McDowell Group study, employed 4,111 Alaska residents, and supported 5,800 jobs in the oil and gas support-services sector, and 31,900 indirect and induced jobs in other private and public sectors.[11] Including those supported by revenue from the oil and gas industry, there are 77,600 jobs in Alaska that can be attributed to oil production.

Oil production contributes a considerable number of jobs, both directly and indirectly, to the Alaska economy even after the declines associated with the recession. Each job created by a primary company is matched by 8 additional jobs supported by primary company activity in Alaska, and 7 additional jobs supported by oil-related taxes and royalties. And each dollar of a primary company employee’s wages is matched by $4 in additional indirect and induced wages in Alaska.[12]

Analysis of Ballot Measure 1

Supporters of Ballot Measure 1 assert that had this provision been in place in FY 2018, the state would have raised an additional $1.1 billion in production tax revenue.[13] Using the same approach for determining (aggregate) production tax revenue under the current system, one can roughly approximate major elements of the proposal and replicate the $1.1 billion claim. But this hypothetical one-time revenue increase is only achievable with an effective production tax increase of over 140 percent in a single year and depends on oil prices that are substantially above prevailing and forecasted prices.

As discussed in greater detail below, however, the $1.1 billion claim is unachievable under current oil prices. Under Alaska’s current revenue forecast, the price of oil never approaches $60 per barrel over the coming decade and is only projected to exceed $50 by 2028. Moreover, substantially all of the hypothetical new revenue available in FY 2018 comes from eliminating the per barrel tax deduction, which were valued at roughly $1 billion in FY 2018, but fall to an average of about $220 million per year over the next decade because at the current price outlook the industry is expected to pay the gross minimum tax that does not allow for any credits or deductions.

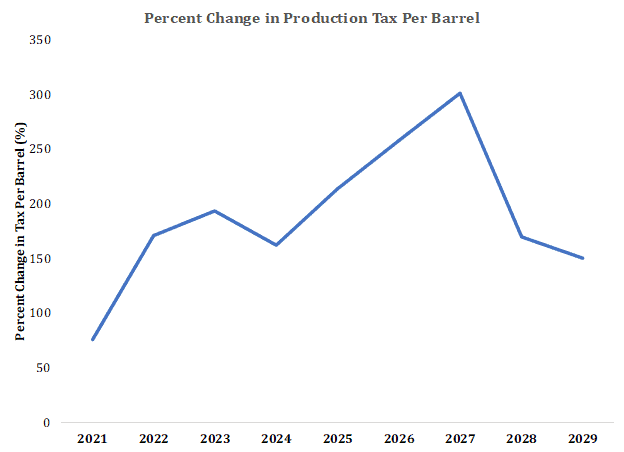

To examine the potential effects of this tax going forward, this study calculates effective tax rates per barrel under the proposal, and under current law, based on the most recent revenue forecasts from the Alaska Department of Revenue.[14] It finds that the proposal would increase the effective tax rate on oil per barrel by an average of 188 percent over the rest of the decade. This would double-down on an already anticompetitive tax regime, which is already “one of the least competitive ones within US and international peer groups.”[15] At low oil prices, Alaska oil production investment is largely uneconomic – the ballot measure would exacerbate this effect. As oil prices recover, an essential condition to the recovery of the oil and gas industry, Ballot Measure 1 becomes more pernicious to energy development in Alaska, cutting the return to energy investment by as much as 79 percent, driving investment to the lower 48 or foreign countries.

Projected Tax Increase

Set against a substantially declining oil price environment, the significant increase in effective tax rates per barrel still fails to collect the revenue advocates have cited in more favorable times. Projecting this tax increase over the next decade yields only 47 percent of the revenue that would be collected if the advocates’ claim of $1.1 billion in new revenue were collected annually. To the extent that advocates have claimed the new revenue could fund initiatives based on a higher level of assumed revenue collection, those claims would need to be at least halved.

Against substantially lower projected oil prices, this analysis finds that major elements of the ballot measure largely never enter into force, because the price of oil does not cross relevant threshold valuations for additional tiers of taxation. Instead, it finds that substantially all of the projected revenue under the proposal would stem from the proposal’s increase in the alternative gross minimum tax. The alternative gross minimum tax is designed as a tax floor that, among other aspects, ensures the state collects some revenue in a given year from producers, irrespective of deductible investment. The proposed ballot measure would disincentivize investment by increasing this tax and, to the extent that oil prices recover sufficiently to be subject to the net production tax regime, would also reduce the after-tax return to oil investment.

To assess the economic effects of such a tax increase, this study applies the relevant literature on production taxes. Specifically, it relies on the finding in a 2019 study by Newell and Prest that the important margin for the price response is drilling, and from a 2014 study by Anderson et al. that “drilling activity and costs, however, do respond strongly to prices.” [16] It relies on historical and projected lease expenditures as a proxy for drilling and costs associated with new production.[17] Last, it relies on the response to tax increases on drilling activity observed in a 2020 study by Brown et al. to calculate the response to a production tax increase.[18]

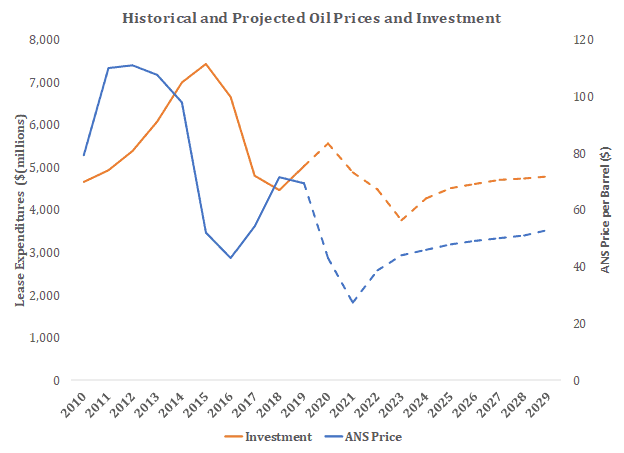

In 2019, there was $5.031 billion in lease expenditures invested in petroleum production in Alaska.[19] This study projects lease expenditures activity based on historical price relationships to establish an investment baseline. It recognizes that considerable uncertainty attaches to such a projection. It projects that over the 2021-2029 period, the oil and gas industry would invest nearly $41 billion in operating and capital lease expenditures.

Investment

According to the 2020 study by Brown et al., “a one-dollar increase in the severance tax paid per barrel leads to an 8.1 to 15.7 percent decrease in the number of wells drilled.” This current study uses the lower-bound estimate for a conservative estimate that over this period, the projected tax increase would lead to a corresponding reduction in investment activity over that period of 14.8 percent, which would amount to nearly $6 billion in lost investment over the period 2021-2029. This assumes the new tax structure directly constrains operating and capital spending on legacy fields, but also constrains investment in other existing fields and fields under development, as a result of a generally weakened Alaska investment environment.

Investment substantially supports employment in the oil and gas industry. According to analysis by the McDowell Group, $100 million in investment supports nearly 1,000 direct and indirect jobs.[20] Based on this linkage, the study finds the average projected $660 million annual loss in investment due to the proposed tax could lead to the loss of 6,300 jobs. For comparison, this study applies the relative decline in investment to the 9,364 production workers and oil field services workers employed in Alaska, implying a direct annual loss of 1,378 workers.[21] If the proportional 14.8 percent loss is applied to all oil and gas industry-related employment in Alaska (excluding jobs associated with taxes and royalties), the proposed ballot initiative would lead to an overall employment decline of 6,100 workers in Alaska.[22]

Conclusion

The proposed Ballot Measure 1 would impose a substantial effective tax increase on a declining tax base, harming an industry that supports the employment of about a quarter of Alaska’s workforce. A global price war and the COVID-19 pandemic have led to a dramatic decline in global oil prices, substantially impacting Alaska’s economy. A new tax would further impact the economy and risk the employment of thousands of Alaskans, while simultaneously failing to deliver an effective and stable revenue model for the state. This proposal illustrates the dangers inherent in severance taxes – both the temptation among policymakers and interest groups to manipulate it to achieve greater revenue, as well as the instability inherent in it relying on oil revenue to fund government programs.

[1] https://www.americanactionforum.org/insight/severance-taxes-prove-to-be-a-poor-choice/

[2] For more on the budgetary treatment of the Permanent Fund transfers, see: http://tax.alaska.gov/programs/documentviewer/viewer.aspx?1573r

[3] Royalties are both the largest source of non-tax oil industry revenue and the largest source of oil-industry.

[4] http://tax.alaska.gov/programs/documentviewer/viewer.aspx?1532r

[5] https://www.aoga.org/sites/default/files/news/10_16_19_km_presentation_to_palmer_chamber_final.pdf

[6] http://www.akleg.gov/basis/get_documents.asp?session=31&docid=60272

[7] https://ltgov.alaska.gov/wp-content/uploads/sites/3/10.14.2019-19OGTX-Attorney-General-Opinion.pdf

[8] See https://lba.akleg.gov/download/oil-gas-2020/lba/Report-Analysis-of-Ballot-Initiative-19OGTX.pdf; https://lba.akleg.gov/download/oil-gas-2020/house_resources/Presentation-Ballot-Initiative-19OGTX.pdf

[9] https://www.elections.alaska.gov/petitions/19OGTX/19OGTX%20-%20Statement%20of%20Costs%20DOR.pdf

[10] https://www.aoga.org/sites/default/files/mcdowell_group_aoga_report_final_1-24-2020.pdf

[11] https://www.aoga.org/sites/default/files/mcdowell_group_aoga_report_final_1-24-2020.pdf Primary Companies include Alaska Gasline Development Corporation, Alyeska Pipeline Service Company, BlueCrest Energy Inc., BP Exploration (Alaska) Inc., Brooks Range Petroleum Corporation, Chevron Corporation, ConocoPhillips Alaska Inc., Eni US Operating Co. Inc., ExxonMobil, Furie Operating Alaska LLC, Glacier Oil & Gas Corporation, Hilcorp Alaska LLC, Marathon Petroleum Company, Oil Search (Alaska), LLC, Petro Star Inc., Shell Exploration & Production Company, and Repsol SA.

[12] https://www.aoga.org/sites/default/files/mcdowell_group_aoga_report_final_1-24-2020.pdf

[13] https://alaskasfairshare.com/summary/

[14] See https://keepalaskacompetitive.com/wp-content/uploads/2020/05/DOR_Memo_5.12.2020.pdf; http://www.tax.alaska.gov/programs/documentviewer/viewer.aspx?1583r; http://www.tax.alaska.gov/programs/documentviewer/viewer.aspx?1573r

[15] https://www.alaskajournal.com/sites/alaskajournal.com/files/cwn-forum-090220-irena-agalliu-1-1.pdf

[16] Richard G. Newell and Brian C. Prest, 2019. “The Unconventional Oil Supply Boom: Aggregate Price Response from Microdata,” The Energy Journal, International Association for Energy Economics, vol. 0(Number 3); Anderson, Soren T. and Kellogg, Ryan and Salant, Stephen W., Hotelling Under Pressure (July 15, 2014). Resources for the Future Discussion Paper No. 14-20, Available at SSRN: https://ssrn.com/abstract=2537827 or http://dx.doi.org/10.2139/ssrn.2537827

[17] See http://www.tax.alaska.gov/programs/documentviewer/viewer.aspx?1573r

[18] Brown, J.P., Maniloff, P., Manning, D.T., Spatially variable taxation and resource extraction: The impact of state oil taxes on drilling in the US, Journal of Environmental Economics and Management (2020), doi: https://doi.org/10.1016/j.jeem.2020.102354

[19] http://tax.alaska.gov/programs/documentviewer/viewer.aspx?1583r

[20] https://www.aoga.org/sites/default/files/mcdowell_group_aoga_report_final_1-24-2020.pdf;

[21] https://live.laborstats.alaska.gov/qcew/

[22] Based on https://www.aoga.org/sites/default/files/mcdowell_group_aoga_report_final_1-24-2020.pdf