Research

November 13, 2019

H.R. 1346 – The Medicare Buy-in and Health Care Stabilization Act of 2019

![]()

In recent months, several lawmakers have released various versions of a Medicare buy-in proposal. Nearly all of them include allowing people aged 50 to 64 to buy into Medicare. In the following report, the Center for Health and Economy (H&E) evaluates the impact of one of these bills – H.R. 1346, “The Medicare Buy-in and Health Care Stabilization Act of 2019,” referred to in this paper as “the bill” – beginning in the year 2022.[1] Consistent with other variations of Medicare buy-in, the bill would allow people from 50-64 years old to buy Medicare coverage for a premium based on the cost of their benefits, and it includes many individual market reforms.

Using its Under-65 Microsimulation Model, H&E analyzed the bill’s impact on health insurance coverage, provider access, medical productivity, and the federal budget. This report details the results of that analysis. All impacts projected in this report are relative to H&E’s July 2019 Baseline.[2] As with all projections, the estimates are associated with some degree of uncertainty.

KEY FINDINGS:

- Premium Impact: Premiums are expected to be reduced by 4 to 12 percent in all metal levels with the exception of single-coverage Gold plans – the category that includes the Medicare buy-in plans. This reduction is largely due to the bill’s creation of a reinsurance fund. Notably, the Medicare buy-in plan premiums are expected to grow at a faster rate than individual market plans with comparable value.

- Coverage Impact: These policies are projected to lead to marginal increases in the size of the insured population within the individual marketplace. Initially the bill would lead to an increase in the individual market of roughly 1 million people. By 2029, however, the increase in individual market coverage will be less than 500,000 relative to the baseline.

- Medicare Buy–In Enrollment: Nearly 300,000 people are expected to buy into Medicare in its first year. This number is expected to decrease to less than 200,000 by the year 2029.

- Medical Productivity: The bill would lead to a 4 percent decrease in medical productivity by 2029.

- Provider Access: The bill would lead to a 9 percent decrease in provider access by 2029.

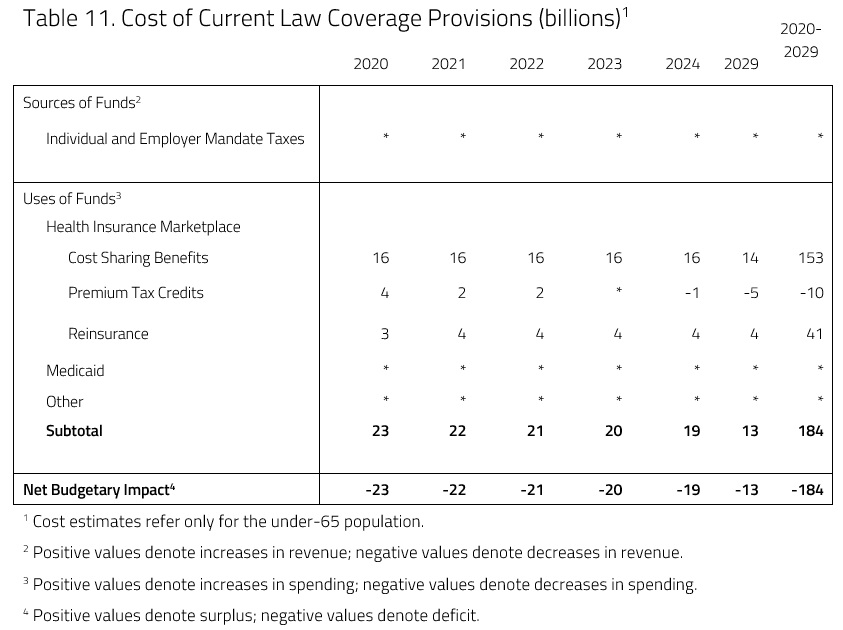

- Budget Impact: The bill is expected to increase spending by $184 billion between 2020 and 2029. The bill does not include any offsetting increases in revenue.

ANALYSIS

This analysis uses a microsimulation model developed for H&E’s use.[3] The model employs micro-data available through the Medical Expenditure Panel Survey to analyze the effects of health policies on the health insurance plan choices of the under-65 population and interpret the resulting impact on national coverage, average insurance premiums, the federal budget, and the accessibility and efficiency of health care. The following provisions from the bill and subsequent assumptions are included in this score.

- This analysis assumes that the bill takes effect on January 1, 2020.[4]

- Those aged 50-64 and not currently enrolled in another government insurance plan are eligible to purchase a Medicare buy-in plan.

- The premiums will be the average annual per capita amount “for benefits and administrative expenses that will be payable under parts A, B, and D in the year for all individuals enrolled,” as per the bill’s language.

- Premiums will be adjusted for geographic variation and ages.

- For this analysis, the average base premium for each individual was calculated using benefits and administration expenses recorded in the 2019 Medicare Trustees Report.[5]

- People enrolled in the Medicare buy-in plan are eligible for all premium reduction and cost-sharing benefits that they would be entitled to under the Affordable Care Act (ACA).

- This analysis assumes that the choice for buying into Medicare is similar to the choice of purchasing a Gold plan with respect to actuarial value.[6]

- An individual market reinsurance fund begins in 2020, with two reinsurance thresholds, as detailed by the bill:

- For 2020-2021, the greater of 80 percent of costs exceeding $50,000, or $450,000; and

- After 2021, the greater of 80 percent of costs exceeding $100,000 or $400,000.

- This analysis assumes that all individual market insurers participate in the reinsurance program.

- The bill calls for increased cost-sharing reductions (CSR) in the individual market. Eligible individuals at each relevant federal poverty level (FPL) will now be able to purchase benchmark Silver plans or Medicare buy-in plans at the following Actuarial Value (AV) levels:

- From 100 percent to 200 percent of FPL: 95 percent AV;

- From 200 percent to 300 percent of FPL: 90 percent AV; and

- From 300 percent to 400 percent of FPL: 85 percent AV.

- This analysis assumes that cost-sharing reduction payments to insurers are re-issued beginning in 2020.

Premium Impact

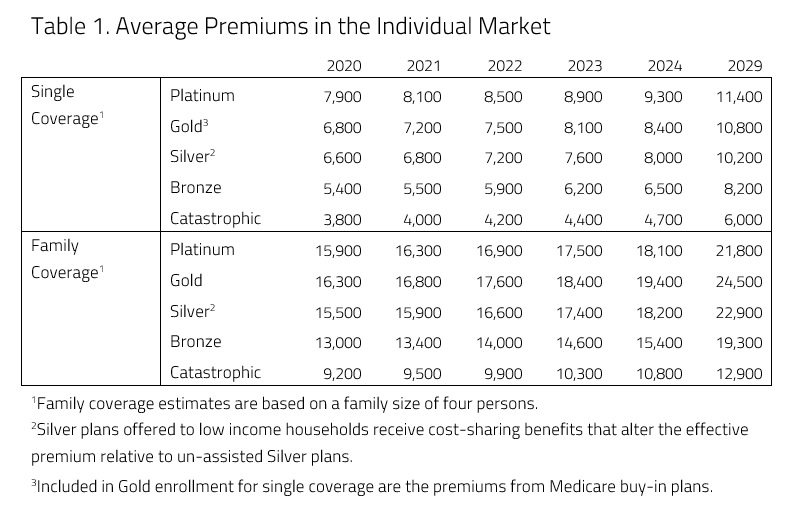

H&E health insurance premium estimates are based on five plan design categories offered in the individual market: Platinum, Gold, Silver, Bronze, and catastrophic. Under current law, the cost-sharing designs of the four metallic categories correspond to approximate actuarial values: 90 percent, 80 percent, 70 percent, and 60 percent, respectively. Catastrophic coverage plans refer to two different kinds of health insurance plans: first, plans that reimburse medical expenses only after members meet a high deductible – a maximum of $7,900 for an individual under current law – and second, Short-Term Limited Duration plans. All premium estimates reflect health insurance prices without any federal subsidies.

Table 1 below presents the average premiums for the purchased plans in each category between 2020 and 2029.

H&E estimates that the bill will lead to lower health insurance premiums in every category. Reinsurance is the main reason that there is expected to be a reduction in premiums, while the existence of the Medicare buy-in plan and the reintroduction of CSR payments are expected to contribute as well.

Current law mandates that insurers offer a Silver plan with reduced cost-sharing for consumers with incomes of 250 percent of the federal poverty level or lower. In exchange for offering plans with reduced cost-sharing, insurers were to receive CSR payments to ease the burden of providing extra benefits. Insurers currently are not receiving these payments, however, resulting in upward pressure on premiums (especially Silver premiums). For this analysis, it was assumed that CSR payments were reintroduced, coinciding with the increase in CSRs in the bill. The reintroduction of CSR payments to insurers is a significant source of premium decreases among Silver plans.

H&E estimates that the presence of a Medicare buy-in option would put downward pressure on premiums due to the types of consumers that are eligible for a Medicare buy-in: people between the ages of 50 and 64. Even though the number of people expected to purchase Medicare coverage are marginal (as seen in Table 5), with the Medicare buy-in attracting these patients out of the individual market risk pool, the individual market becomes younger and healthier, leading to reduced premiums.

As can be seen in Table 2, the premiums for the Medicare buy-in are expected to be higher than comparable plans (Gold) in the individual market, as shown in Table 1. The bill calculates the Medicare buy-in premium based upon the average, annual per-capita amount for benefits and administrative expenses for people enrolled through the buy-in. As this group is expected to be less healthy, on average, than the rest of the individual market, the Medicare buy-in premium is expected to be more expensive than individual market plans with comparable AV.

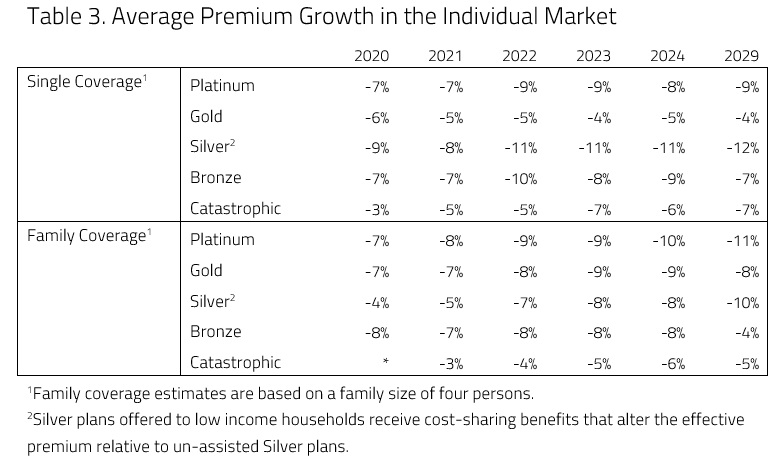

The policy that is expected to have the greatest effect on premiums is reinsurance.

Reinsurance would provide payments to insurers that enroll high-cost beneficiaries, thereby offsetting some of the risk that insurers take on for enrolling such beneficiaries. In this analysis, it is assumed that insurers would receive payments for the costs they incur for patients in the 95th percentile of cost – i.e., the most expensive beneficiaries. Relative to the 2019 baseline projection, H&E expects reinsurance to put downward pressure on premiums in every metal level. Table 3 below shows the overall changes in premiums due to both CSRs and reinsurance relative to the baseline.

Coverage Impact

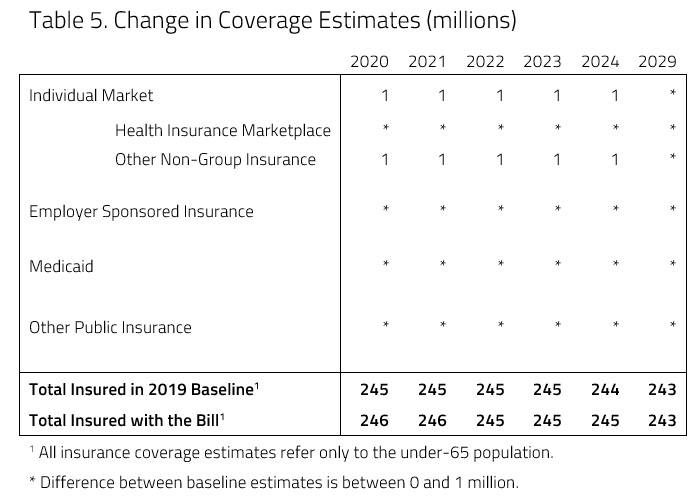

H&E insurance coverage estimates reflect health insurance choices for the under-65 population. H&E estimates that the bill would result in marginal increases in the insured population, with 1 million more consumers obtaining insurance in the year 2029 relative to the 2019 baseline projection. Table 4 below shows the overall projected insurance levels.

Within the individual marketplace, H&E expects enrollment to increase most outside of the Health Insurance Marketplace created by the ACA, as Table 5 shows below. The bulk of this increase is the result of reduced premiums caused by the healthier risk pool and reinsurance. The bill’s enhanced CSRs are also expected to contribute to the small increases of insured in the Health Insurance Marketplace.

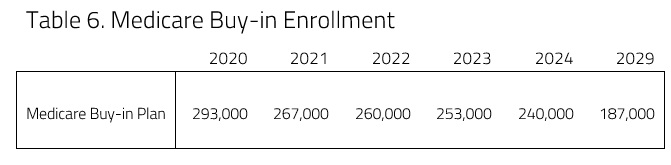

As can be seen in Table 6, roughly 300,000 consumers are expected to purchase insurance through the Medicare buy-in in 2020. This number is expected to decrease to less than 200,000 toward the end of the time considered in this analysis. Because of the cost of the plan relative to similar AV plans in the individual market, very few consumers are expected to purchase Medicare without the help of tax credits and CSRs. Because of the cost, H&E does not expect Medicare buy-in to lead directly to increases in the number of insured people.

Productivity and Access

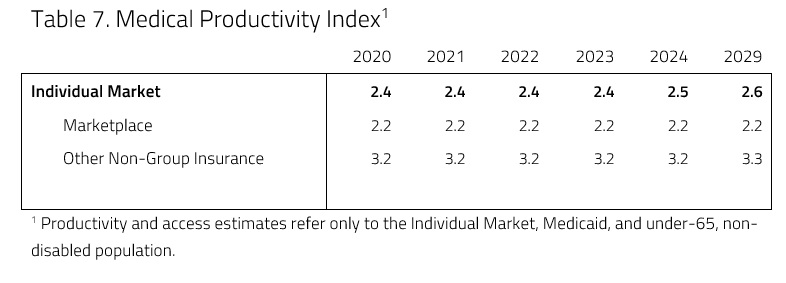

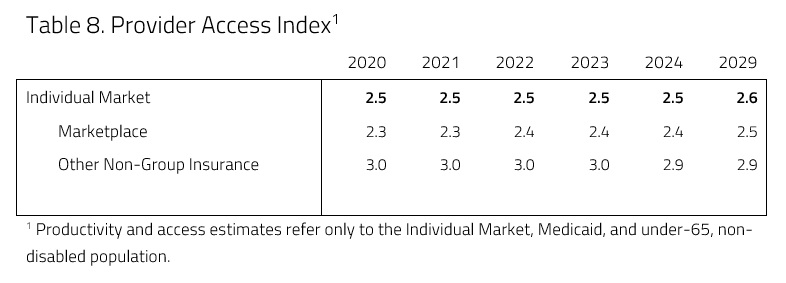

In an attempt to evaluate access and productivity in the health care system, H&E estimates the Medical Productivity Index (MPI) and the Provider Access Index (PAI). Health insurance plan designs are associated with varying degrees of access to desired physicians and facilities, as well as incentives that promote or discourage efficient use of resources. H&E estimates each index by attributing productivity (i.e. efficiency) and access scores to the range of plan designs available and uses the changes in plan choices to project the evolution of health care quality. These scores for the bill’s impact on the entire health care system are provided in Tables 7 and 8, below.

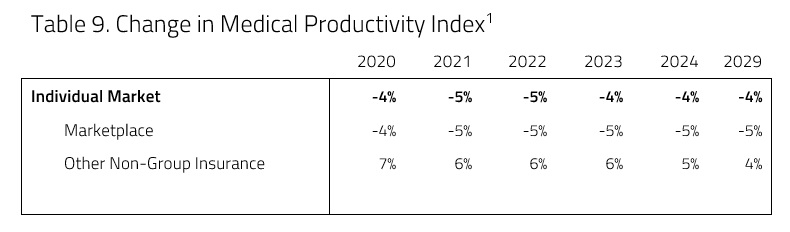

H&E expects medical productivity to decrease relative to the 2019 baseline projection as a result of the bill, as Tables 9 below demonstrates. The increased enrollment in Medicare and corresponding decrease in premiums is expected to result in a larger proportion of consumers insured in higher AV plans with lower cost sharing. Lower cost sharing means lower medical productivity (or efficiency), as people are more likely to pursue health care services. By 2029, medical productivity is expected to decrease by 5 percent relative to conditions under current law.

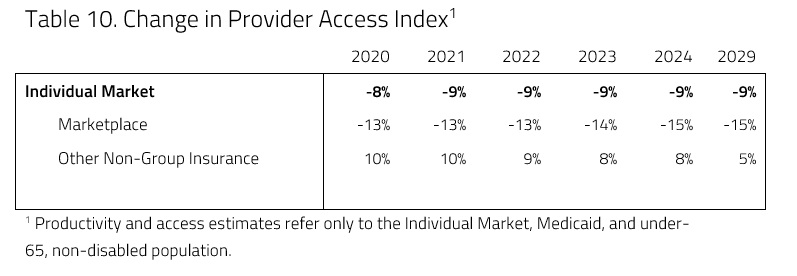

Provider access is also expected to decrease under the plan. This decline is primarily due to consumers shifting from Gold plans to Silver. This largely results from the assumption that CSR repayments would be reissued to insurers. The reinstatement of CSR payments and the immediate decrease in Silver plan premiums would result in a shift of consumers from Gold plans to Silver plans. Therefore, though a Medicare buy-in would draw some consumers into the greater provider access that comes with Medicare, the shift of consumers from Gold to Silver plans would be greater, resulting in an overall drop in provider access.

Budgetary Impact

H&E projects that the bill will lead to a $184 billion net increase in the budget deficit relative to the current H&E baseline over the next decade. H&E does not assume any new tax; therefore there is no revenue-raising mechanism in this score. Reinsurance and CSR payments are both federal payments to insurers, and the combination of the two payments would result in roughly $194 billion in added spending.

H&E expects, however, a decrease in individual market insurance subsidies to offset that spending by $10 billion. Reinsurance, by itself, would likely have a greater impact on premium subsidy spending. The bill allows premium subsidies to be spent on those purchasing Medicare coverage, however, offsetting much of the reduction. After spending increases and decreases interact, the result is a net spending increase.

Uncertainty in Projections

H&E uses a peer-reviewed microsimulation model of the health insurance market to analyze various aspects of the health care system.5 As with all economic forecasting, H&E estimates are associated with substantial uncertainty. While the estimates provide a good indication on the nation’s health care outlook, there are a wide range of possible scenarios that can result from policy changes, and current assumptions are unlikely to remain accurate over the course of the next 10 years.

Aside from the potential policy changes, the magnitude of premium changes in the individual market are a specific area of uncertainty in this report. The introduction of a substantial, federally funded reinsurance program would reduce risk for insurers in the individual market and put downward pressure on premiums; it is unclear, however, how much premiums will change – especially in the earlier years of the budget window considered. It is possible that insurers would be more cautious in setting premiums in the earlier years of such a program.

H&E also assumed no effect on negotiated rates between insurers and providers as a result of moving roughly 200,000 individuals from the individual marketplace into Medicare. Presumably such action would place upward pressure on premiums in the individual market as hundreds of thousands of people become covered at Medicare rates rather than private rates.

Next, the bill authorizes the Secretary of Health and Human Services to charge a fee from insurers that wish to participate in the reinsurance program. The bill does not stipulate, however, how the Secretary should implement it, the amount of the fee, or whether the Secretary must charge this fee in order to establish a reinsurance program. Due to this ambiguity, this analysis does not include this portion charged to insurers.

There are many implications of this assumption. Any fee that would be charged to insurers for the establishment of such a program would likely result in increased premiums. Increased premiums would then lead to lower individual market enrollment, or higher federal spending on subsidies, or both.

Another substantial source of uncertainty stems from implementation of the bill’s increased CSRs. In 2017, CSR payments to insurers were discontinued. While these payments are still included in current law, they are not appropriated. The bill does not specify whether CSR payments to insurers will recontinue. For this analysis, it was assumed that CSR payments to insurers would recommence for the sake of consistency. If the bill were passed yet insurers were not reimbursed for CSR payments, premium levels, enrollment, and costs to the federal government would all be impacted.

[1] Bill text can be found at: https://www.congress.gov/116/bills/hr1346/BILLS-116hr1346ih.pdf

[2]https://www.americanactionforum.org/research/health-and-economy-baseline-estimates/

[3] More information on the H&E Under-65 Microsimulation Model can be found at http://healthandeconomy.org/models/under-65-microsimulation/

[4] H.R. 1346 begins implementation in the year 2019. For this analysis, it is assumed that implementation begins in 2020. That is the only assumption that contradictory to the timeline stipulated by the bill.

[5] https://www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-Trends-and-Reports/ReportsTrustFunds/Downloads/TR2019.pdf

[6] https://www.kff.org/wp-content/uploads/2013/01/7768-02.pdf