The Shipment

August 21, 2025

Don’t Count Your Inflation Reports Before They Hatch

(Not So) Fun Fact: The Trump Administration expanded the 50-percent steel and aluminum tariffs on Monday to include more than 400 derivative products, impacting roughly $180 billion in imports. According to the Shipment’s calculations, these additional tariffs will cost between $768 million and $9.6 billion, depending on the average metal content.

The Producer Price Index Jump Scare

What’s Happening: Last Thursday, the Producer Price Index (PPI) – a measure of inflation for businesses – showed that month-over-month final demand rose 0.9 percent in July rather than 0.2 percent as expected. This marks the largest monthly increase since June 2022 and comes in hotter than 32 of the 39 monthly PPI reports during the COVID-19 pandemic. The 12-month change was not much better, coming in at 3.3 percent, well above the 2.6 percent expected but still in line with PPI reports from earlier this year. After this data release, there was virtually no mention of PPI by President Trump or other members of the administration, in sharp contrast with the upbeat reactions to the rather muted July Consumer Price Index (CPI) report.

Why It Matters: As the Shipment noted ahead of the latest PPI report, those who continue to downplay economic concerns – particularly those arising from tariff increases – shouldn’t celebrate the end of inflation too early. While July CPI came in cooler than expected, it remains elevated from the 2-percent target and points to concerns about rising prices for certain goods. Similarly, PPI is signaling that there are real inflationary concerns that may be tied to tariff policy. As a reminder: PPI measures the average change in the price of domestically produced goods, services, and construction at various steps in the value chain. The price indexes can be broken down by industry, commodity, and whether an output requires further processing or not. Notably, tariff costs are not directly measured because imported goods are excluded from PPI, meaning that domestic producers may be raising prices in response to higher tariffs in order to maximize their revenue and take advantage of the larger barriers to entering the U.S. market. Additionally, a 2018 study shows that tariffs increase input costs for firms, raising domestic producer prices and influencing PPI. Some of the most impacted PPI categories include machinery and vehicle wholesaling, home electronic equipment, computers, aluminum, copper, and iron. Each of these industries was hit heavily by tariffs and is reliant on international trade either for inputs or imported finished products. This suggests domestic producers may be raising prices in response to higher input costs, as well as to match competitors that face greater U.S. protectionism.

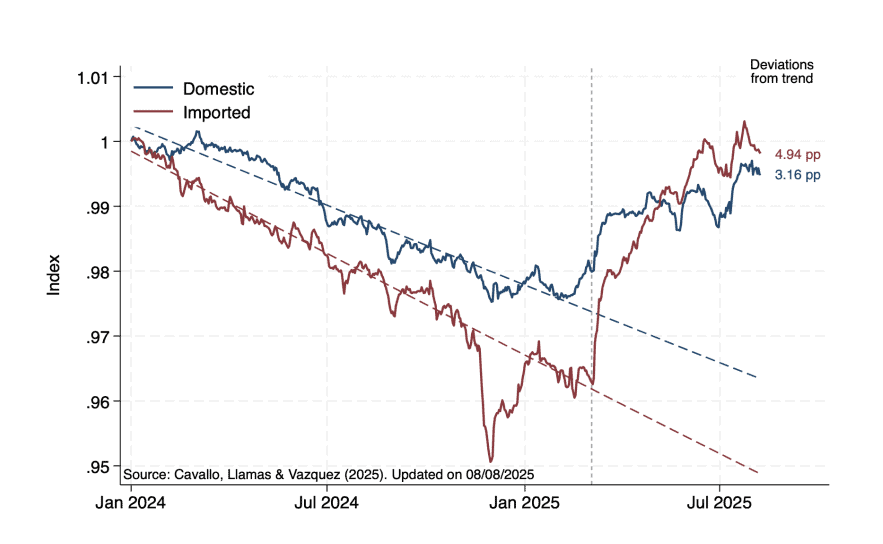

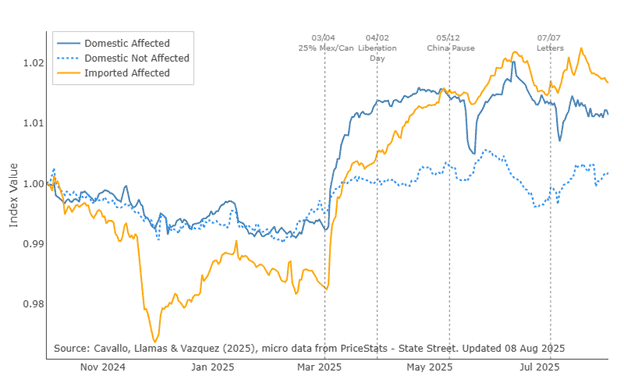

The Pricing Lab tariff tracker at Harvard, alongside a paper published by Alberto Cavallo, supports the claim that prices are on the rise, whether the goods are domestically produced or imported. Figure 1 displays retail price data from five large U.S. retailers broken into domestic and imported categories and normalized to 1, representing the first observation date. Also shown is the pre-tariff trendline from January 2024 until March 2025, which marked the imposition of large-scale tariffs on China, Canada, and Mexico. In the immediate aftermath, retail prices of both imported and domestic prices rose and broke the downward trend. Imported products cost 5 percent more, and domestic products cost 3 percent more, than they otherwise would without President Trump’s tariffs. Figure 2 goes a step further and differentiates domestic goods that are directly or indirectly impacted by tariffs. While directly impacted goods clearly had a sharper price hike, indirectly impacted domestic goods still rose from pre-tariff trends, albeit at a slower and less substantial pace.

Looking Ahead: That domestic firms are charging higher prices is a feature and not a bug of tariff policy. As is widely discussed, tariffs raise the cost of foreign inputs, which eventually hits U.S. consumers unless firms shift to domestic sources. Tariffs also protect the profit margins of U.S. manufacturers that can afford to worry less about competitive prices from foreign firms. The data coming in are beginning to align with orthodox economic theory, which does not bode well for economic growth, inflation, and the prospect of hastened interest rate cuts. The U.S. economy will not only have to deal with direct tariff costs – estimated to be over $380 billion annually, according to the Shipment – but also higher prices from U.S. producers that might go under the radar. These price hikes won’t be picked up as additional government revenue and therefore won’t be touted by the administration, which appears to be otherwise proud of having taken in record import tax revenue. The surprise PPI data will also put Federal Reserve Chairman Powell in a sticky situation when deciding whether to cut interest rates in September, as he will have to balance stubborn CPI, rising PPI, and a weaker job market. For now, markets expect an 85-percent chance of a 25-basis point cut (down from 95 percent a week ago) and a 15-percent chance rates remain the same (up from 0 percent a week ago). Chairman Powell will likely provide insight into his thinking when he speaks tomorrow at the annual economic policy symposium.

Figure 1: U.S. Retail Price Indices With Pre-tariff Trends – Domestic vs. Imported

Figure 2: Daily Price Indices for Different Good Categories

An Update on the European Union Trade Deal

What’s Happening: The White House and European Commission released a joint statement today on the agreed-upon terms of the U.S.-EU trade deal.

Why It Matters: As the Shipment noted on July 31, the previous trade deal factsheets of the United States and the European Union did not align with one another, with numerous differences on what would actually be addressed regarding tariffs, non-tariff barriers, and investments. Today’s joint statement provides a much more unified framework that more closely resembles the original EU factsheet, with only a few minor tweaks and additions.

Looking Ahead: This trade agreement will still require a majority of EU countries to ratify it, so it may be months or years before a final, binding trade deal is complete. The new statement sheds light on what a final deal might look like, however, and provides a bit more hope that a formal end to this trade war can be declared, even if higher U.S. trade barriers will remain in place.

![]()