The Shipment

August 14, 2025

Inflation Information and Semiconductor Selling

(Not So) Fun Fact: The China tariff pause has once again been extended by 90 days, making the new deadline November 10.

Let’s Look at Inflation

What’s Happening: On Tuesday, the Bureau of Labor Statistics released the Consumer Price Index (CPI) for the month of July, showing that month-over-month prices rose 0.2 percent and year-over-year inflation sits at 2.7 percent. While monthly inflation came in as expected, 12-month inflation came in slightly lower than the expected 2.8 percent. President Trump and Treasury Secretary Bessent took this report as a sign that tariffs are having no discernable impact on consumer prices, meriting a rate cut from the Federal Reserve. Core CPI (which excludes food energy) rose 3.1 percent year over year, which was higher than anticipated and likely influenced by tariff pressures. The inflation picture remains in flux as the latest CPI reads have not shown a significant spike in overall prices but the year-over-year inflation rate has been steadily increasing since April, the beginning of “Liberation Day” tariffs. (See the chart below.) Meanwhile, government tariff revenue – paid for almost entirely by U.S. consumers and businesses – is soaring to record highs, hitting nearly $30 billion in July alone.

Why It Matters: Given the latest CPI report, people may be asking where the massive wave of tariff-fueled inflation is and why there hasn’t been such a large-scale price shock as many economists predicted. The answer is multifaceted. First, inflation remains well above the Federal Reserve’s 2-percent target and the deceleration of the inflation rate has virtually stalled in recent months. Year-over-year inflation declined from 3 to 2.3 percent between January and April but now sits at 2.7 percent as of July. Similarly, core year-over-year inflation declined from 3.3 to 2.8 percent between January and March but has since ticked back up to 3.1 percent. The break in the downward CPI trend roughly corresponds to the March imposition of fentanyl-related tariffs and “Liberation Day” in April.

Second, business surveys and Goldman Sachs analysis indicate that U.S. businesses have absorbed more than 60 percent of tariff costs as of June while foreign exporters have absorbed roughly 14 percent. This means that U.S. consumers have only experienced a fifth of the costs from tariffs thus far. Goldman Sachs anticipates that U.S. consumers will be paying 70 percent of tariffs by October of this year. The Federal Reserve Bank of Atlanta explains that small to medium-sized firms with between 1 and 500 employees are most likely to be stuck with higher input costs while large companies have a greater capacity to pass along higher prices. This could have a seriously negative impact on the 62 million people employed by the 33 million small businesses throughout the United States as they are less able to compete with corporate giants that rely on pricing power, economies of scale, and tariff exemptions. Last, it is important to note that prices of specific products have had substantial increases in recent months, well above headline figures. Cookies, lettuce, ham, infant apparel, tomatoes, women’s dresses, coffee, audio equipment, and citrus fruits were just a few products with month-over-month inflation above 2 percent. Since April, some of the most impacted goods include certain clothing, electronic equipment, fruits, appliances, and toys, all of which are heavily dependent on imports.

Looking Ahead: As the Shipment mentioned last week, it is important to keep in mind that current economic tremors such as the recent jobs report are trickling into the data after the imposition of a universal 10-percent tariff. The full force of the Trump Administration’s tariffs has been on hold since April 2, which means much higher tariff rates have yet to work their way into the U.S. economy and may be less inflationary due to their downward pressure on demand. But combining higher tariffs with businesses passing along to consumers more tariff-related costs as time goes on will almost certainly yield some inflationary pressure, reduced demand, or most likely, some combination of both. Current (and looming) tariffs represent hundreds of billions of dollars in additional taxes that were not in place one year ago. In short, tariff enthusiasts should continue to pay close attention to incoming data before celebrating this week’s mild inflation report too early.

CPI Measures of Inflation: Year over Year

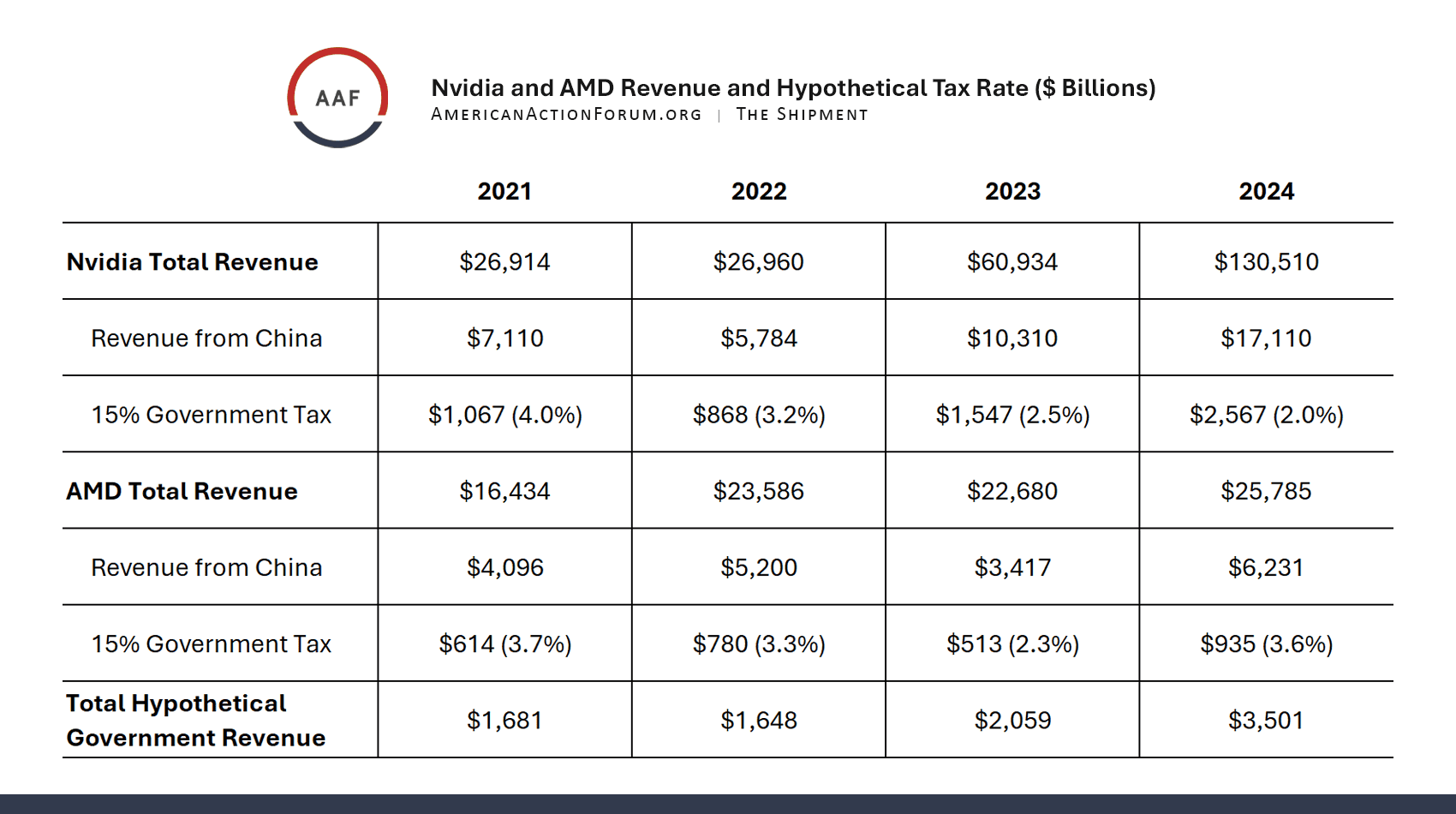

Nvidia and AMD Pay to Play

What’s Happening: The Trump Administration struck a deal with Nvidia and Advanced Micro Devices (AMD) that allows the semiconductor companies to sell their chips in China in exchange for paying the U.S. government 15 percent of the revenue from those sales. This is a complete reversal of the Trump Administration’s own policy to ban the sale of certain chips to China due to national security concerns. More stringent chip policies in regard to China began during Trump’s first term, and escalated during the Biden Administration which crafted a framework for AI export controls on most trade partners. The Trump Administration upheld these policies and expanded upon China export restrictions in April by blocking the sale of the H20 chip which had been specifically designed to be less advanced in order to enter the Chinese market. (See AAF’s Jeff Wrestling’s insight and Douglas Holtz-Eakin’s Dish on this issue.)

Why It Matters: Since this 15-percent revenue tax applies to chips sold in China, it is best categorized as an export tariff rather than a corporate tax, unless the administration seeks to classify this policy as some sort of targeted corporate tax. This agreement effectively marks the first time the Trump Administration has proposed implementing a tariff on exports from the United States, which may pose a legal problem. The Export Clause, Article 1, Section 9, of the U.S. Constitution explicitly prohibits export tariffs. Specifically, it states that “no tax or duty shall be laid on articles exported from any state.” Unfortunately for the administration, most loopholes such as taxes on shipping insurance and certain stamp taxes have already been tried and slapped down by the Supreme Court.

Some authority, however, has been granted to the executive branch surrounding export controls on military equipment and other goods with national security implications, such as chips. The Export Control Reform Act allows the federal government to issue export licenses to companies – particularly those selling goods with national security implications – but it also explicitly states that “no fee may be charged in connection with the submission, processing, or consideration of any application for a license” which may rule this out as a legal defense avenue. It is possible that if this deal faces legal scrutiny, the administration could use a combination of precedence relating to the Export Clause and the Export Control Reform Act. The Supreme Court has upheld that the Export Clause allows a “user fee” to be charged if it is compensating for “government-supplied services, facilities, or benefits” which could potentially be tied to the government’s issuance of licenses. Certain military manufacturers do, in fact, pay annual licensing fees, which may also help the administration’s case.

As for the economic implications, this tax represents roughly 2 percent of Nvidia’s revenue and close to 4 percent of AMD’s revenue. The Shipment estimates that annual U.S. government revenue from this deal is set to be roughly $3.5 billion. If sales trends in China are maintained, that estimate is likely to grow to $5 billion or more in the future. Depending on your perspective, this deal may be positive as it allows U.S. companies to maintain market share, or negative as the potential national security costs may outweigh the added tax revenue. From the chip companies’ perspectives, sacrificing a few billion dollars to have access to the $50 billion Chinese market is a simple cost-benefit analysis.

Looking Ahead: The legality of this 15-percent revenue tax is uncertain, and there will likely be a court challenge from one stakeholder or another – Nvidia or AMD shareholders, rival chip manufacturers, or other interested parties. Going forward, Nvidia and AMD will likely be exempt from a semiconductor tariff of up to 100 percent due to their U.S. investments. This exemption, worth upward of tens of billions of dollars in tariff savings, is further incentive to chip companies to play ball with the Trump Administration as it could easily be taken away.

![]()