The Shipment

September 25, 2025

Manufacturing Foreshadowing and Visa Fees

U.S. Manufacturing and Consumer Spending

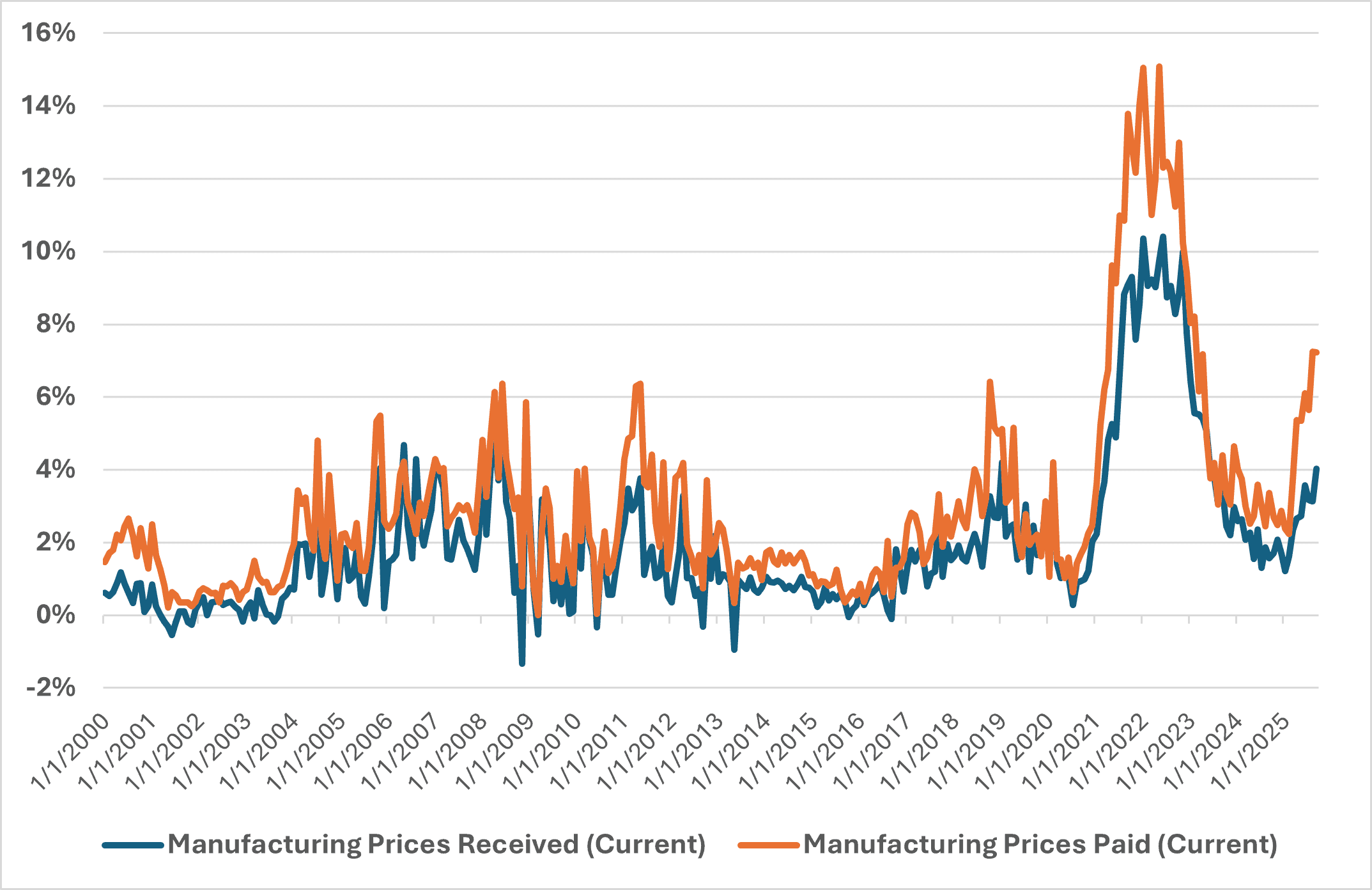

What’s Happening: On Tuesday, the Federal Reserve Bank of Richmond released its monthly survey of manufacturing activity within the Fifth Federal District. This survey tracks business responses to questions relating to orders, backlogs, inventories, various expenditures, and more in order to create an index for activity. The overall index fell from -7 in August to -17 in September, showing a softening in U.S. manufacturing activity. The prices paid (input costs) rose in September, reaching a 7.22-percent increase over the past 12 months. During the same period, the prices received (manufacturer sale price) increased by 4.02 percent. Meanwhile, overall consumer spending as of September is stable, but most categories impacted by tariffs are experiencing weakness. According to data from Apollo Global Management, there is falling consumer-spending momentum for clothing, electronics, appliances, and furniture. While these are all discretionary categories, other discretionary categories such as air transportation, food services, and non-store retailers have seen rising momentum.

Why It Matters: The combination of data that show weakening consumer spending and weaker manufacturing activity points to the underlying and slow-moving economic impact of tariffs. The manufacturing activity survey shows that rising input costs for U.S. businesses have not been fully passed on to U.S. consumers. Figure 1 shows the annualized percentage change in the prices paid by manufacturers for inputs and the prices manufacturers receive for their products. There is usually a small difference or gap between the change in a manufacturer’s costs and the sales price. Since 2000, the median gap has been 0.83 percentage points and the average gap 1.07 percentage points, meaning the annualized percentage change in input costs is slightly higher than prices received. This includes the volatile COVID-19 period during which the median and average percentage-point gap was 1.92 and 2.28, respectively. Currently, the September 2025 gap is 3.2 percentage points. If the gap were to return to historic levels, prices received by manufacturers would rise by roughly 6.4 percent annualized. This is a more than 2-percentage point increase from the current 4-percent annual increase in manufacturing sales prices. This suggests that U.S. manufacturing customers – whether other U.S. businesses or U.S. consumers – should expect to see further price inflation as the year progresses. Given that consumption is already stalling, further price hikes would likely only exacerbate falling demand from hard-hit U.S. consumers. Moreover, the incoming data do not make the Federal Reserve’s job any easier, as a slowing economy mixed with higher inflation puts the Fed’s two goals of balancing employment with price stability at odds.

Looking Ahead: As the Shipment continues to emphasize, business surveys show that most of the added tariff costs have yet to be passed along to consumers. Tariff passthrough is expected to pick up in the coming months. Tariff-related price increases should fully conclude by the end of 2026, according to Fed Chair Powell. The Shipment’s analysis of the recent manufacturing activity survey further supports the claim that businesses are not done shifting the cost burden to U.S. consumers this year. Powell reiterated this week that the Fed is determined to ensure tariffs are a one-time price hike rather than an inflationary trend that might un-anchor consumer price expectations. It is important to continue monitoring the Consumer Price Index (CPI) and Producer Price Index (PPI) as multiple hot readings could deter the Fed from reducing rates more aggressively.

Figure 1: Manufacturing Prices Paid vs Prices Received (Annualized Percent Change)

Source: Federal Reserve Bank of Richmond

Let’s Look at Visas

What’s Happening: Last Friday, President Trump signed an executive order (EO) to increase to $100,000 (up from between $2,000 and $5,000, depending on the size of the company) the fee on H1-B visas, which are given to foreign workers with advanced degrees and distributed via a lottery system. The administration argues that the H-1B visa program has been exploited by employers to replace U.S. workers with lower-paid, lower-skilled foreign workers. The EO points out that the number of foreign STEM workers more than doubled between 2000 and 2019, to 2.5 million H1-B holders, representing 1.5 percent of the labor force. Furthermore, the administration specifically calls out the information technology sector for outsourcing U.S. employment to foreign labor.

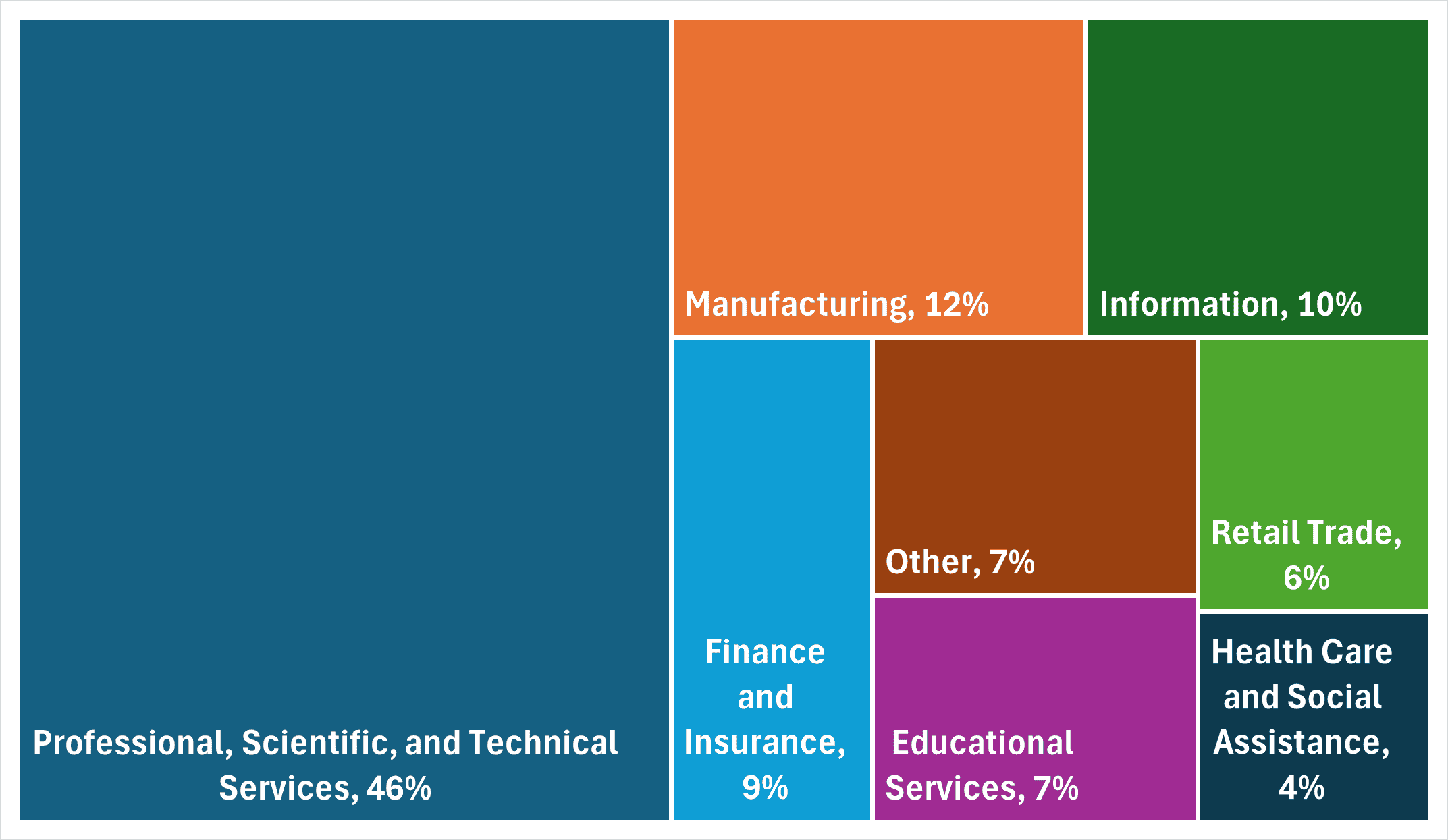

Why It Matters: About 85,000 new applicants are given a visa annually under the lottery system. More likely than not, the number of firms that will be able to afford a nearly 2,000-percent price hike for a visa will decline substantially. Accordingly, companies will either hire fewer (or no) foreign employees or they will lower salaries and other benefits to shift some of the added cost burden. It is also likely that some industries, such as information technology, will forgo hiring expensive labor and accelerate a shift to alternatives such as artificial intelligence where they can. Notably, as this is a one-time fee for new applicants, current visa holders will be even more valuable to U.S. businesses, and the policy is likely to result in less labor turnover for H1-B visa holders as companies try to hold onto these workers – an outcome antithetical to the EO authors’ intention. It is also interesting to note that nearly 12 percent of H1-B applications in 2025 came from the U.S. manufacturing industry. Less availability of skilled manufacturing labor could damage the Trump Administration’s ability to boost U.S. manufacturing prowess.

Looking Ahead: The ramifications of this move will undoubtedly take years to fully understand as it will have impacts on specific firms, the availability of foreign labor, the U.S. education system, the choices of American workers, the rate of business creation, and more. There may be some benefits for available U.S. workers, who would face a less competitive environment for select jobs. Even if skilled American workers fill this void, there would still likely be a lag time between the training of U.S. workers and their entrance into the slow-moving labor pool. Furthermore, the attractiveness of U.S. higher education will also decline for foreign students, as high achievers no longer have a clear path to work, innovate, and live in the United States. Education services is one of the largest U.S. exports, totaling $50 billion in 2024.

Figure 2: H1B Visa Applications by Industry (2025)

Source: U.S. Department of Labor

![]()