The Shipment

July 3, 2025

Pre-tariff Deadline Edition: Liberation Day Strikes Back

Fun Fact: The elimination of Canada’s 3-percent digital services tax will save U.S. companies an estimated $2 billion in retroactive payments and nearly $1 billion annually going forward.

The End of the Tariff Pause Is Coming

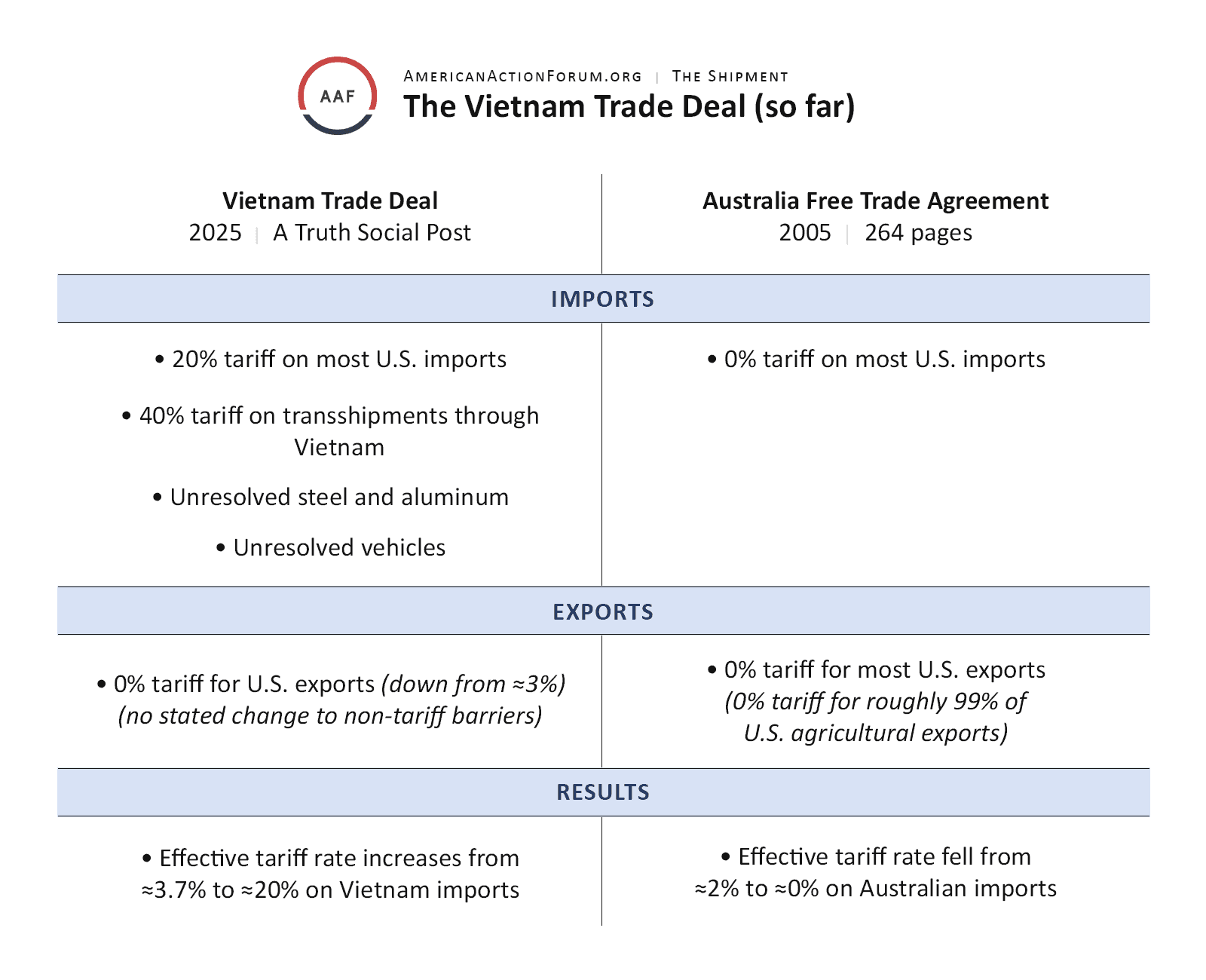

What’s Happening: On July 9, President Trump and his trade team will determine the degree to which “Liberation Day” tariffs snap back into place on U.S. trade partners. These tariffs, first imposed on April 2 using the International Emergency Economic Powers Act (IEEPA), were put on hold April 9 to allow time for trade negotiations to take place. While the intention was to strike 90 deals in 90 days, there has only been one published trade deal – which is only about four pages long – with the United Kingdom. There has been limited progress with the most consequential U.S. trade partner, China, as new tariffs have been lowered from 145 percent to 30 percent, and a “trade framework” has materialized after multiple rounds of negotiations. These actions have only partially de-escalated trade tensions to the previous status quo, but the Trump Administration has until its deadline of August 12 to figure out the end game for China tariffs. The European Union (EU) remains hopeful that a deal can be struck before a 50-percent tariff strikes, although EU retaliatory tariffs still remain on standby. Perhaps the administration’s greatest trade achievement happened this week with the announcement that Canada would rescind its planned digital services tax in exchange for a tariff pause extension until July 21 and more favorable odds at striking a deal with Trump. Furthermore, President Trump announced a trade deal with Vietnam on Wednesday, specific details of which have not yet been released.

Why It Matters: The initial “Liberation Day” tariffs unilaterally imposed by President Trump via IEEPA would have been equivalent to a roughly $370 billion-increase in costs for U.S. consumers and businesses, according to American Action Forum research. It is worth a reminder that a universal 10-percent baseline tariff has remained in place since “Liberation Day,” estimated to cost every American consumer between $1,700 and $2,350 annually. Trump’s tariffs have not yet impacted consumer goods inflation, which has reinforced the administration’s zealous belief that tariffs are an inherently good economic policy. As the Shipment noted last week, business surveys and the Federal Reserve chairman’s comments indicate that the cost of tariffs will be passed along to consumers, raising prices in the coming months. Even if only half of the “Liberation Day” tariffs are re-imposed next week, the impact would fuel inflation concerns within the Federal Reserve, thereby reducing the odds of an interest rate cut and raising uncertainty in the markets. As of now, 97.9 percent of U.S. imports could be stuck with tariff rates ranging from 10–50 percent. The Canadian deadline was extended until July 21, and the Chinese deadline is August 12, meaning two of the largest U.S. trade partners are confirmed to be off the table next week. Additionally, the preliminary trade deal with Vietnam prevents “Liberation Day” Part Two tariffs from snapping back on the country’s imports, although those goods are now subject to a 20-percent tariff, double the 10-percent baseline and five times 2024 levels. All told, 68 percent of the total value of U.S. imports are still at risk of higher tariffs.

Looking Ahead: Many of the trade partner deals that were predicted to be signed early have not yet come to fruition, such as with India, South Korea, and Japan. Indeed, Japan was recently targeted by President Trump, who this week stated he will send the country a letter that includes its final tariff rate – suggesting a pause is out of the question – owing to Japan’s failure to accept U.S. rice exports. If this is any indication, it signals that the Trump trade team is, in some cases, prepared to introduce tariffs on countries that are not meeting its expectations. The combination of a deadline extension for Canada, and the intention to re-introduce tariffs on Japan, provides weight to the middle-of-the-road scenario the Shipment anticipated on June 20: Countries close to a deal may receive a tariff pause extension while tariffs snap back on other countries that are further from a deal. There is still time for the administration to announce a flurry of trade deals in the days ahead, in which case it is likely such deals follow a pre-determined trade template wherein countries fall into different buckets depending on certain criteria. In any case, the ability of countries to fully avoid higher tariffs seems improbable, with the best-case scenario being the mitigation of greater tariff costs. Even after the economically earthshattering Liberation Day test run, markets appear to have relaxed in their planning for the reality of higher, more entrenched tariff rates.

![]()