Testimony

June 7, 2023

Testimony on: Prices on the Rise: Examining the Effects of Inflation on Small Businesses

United States House of Representatives Committee on Small Business

* The views expressed here are my own and not those of the American Action Forum.

Chairman Williams, Ranking Member Velázquez, and members of the Committee, thank you for the privilege of appearing today to discuss inflation and its effects on small business. I hope to make the following main points:

- The United States is experiencing persistent inflation that is taxing America’s families and businesses.

- Policy choices have contributed to the recent, rapid acceleration in price levels.

- Federal policy should be oriented around reducing inflationary pressures – and the record has been mixed at best.

Let me discuss these in turn.

The Inflationary Environment

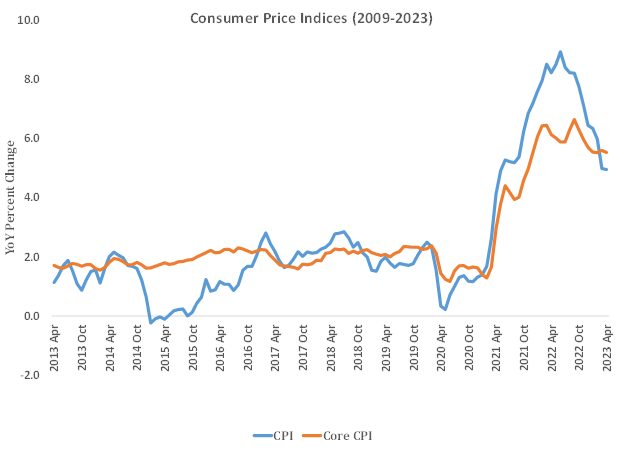

According to the U.S. Census Bureau, the median age in the United States is about 39, which means that a bit more than half of the country has never experienced inflation like what the United States has seen over the last two years. Not since 1980 has the Consumer Price Index (CPI) grown as rapidly as was observed in June of 2022 when yearly inflation topped 8.9 percent.

Stripping out more volatile food and energy price components to isolate core price growth reveals a similar story of rapid, historically aberrant inflation. Notably, one can observe a significant divergence between the two indices around the time of the Russian invasion of Ukraine that significantly disrupted energy markets. It is clear that event moved food and energy prices, but the fundamental story of U.S. price growth is not about the Russian invasion, but the laws of supply and demand.

These laws are in force, and they are taxing small businesses and the households that support them. Over the last two years, yearly price inflation has averaged 2 percentage points higher than yearly wage growth. Wage growth has been substantially elevated over the same period but has nevertheless failed to keep pace with price growth. Put another way, small business and households are falling behind. While inflation is down off of the recent peak, it remains stubbornly elevated at well above the average of recent decades, and more than twice the target rate set by the Federal Reserve.

Thus, even though the U.S. inflation outlook is improved, enduring inflation nevertheless is a significant tax on household finance that will diminish the U.S. standard of living. At the current rate of 5 percent, a family with the median income of $70,784 is paying over $3,500 in price growth.[1] Relative to stable price growth, this is a $2,000 tax right out of household budgets. Food, energy, and shelter prices – which tend to be more volatile but nevertheless represent about half of the average household budget – have been even more elevated, and serves as a uniquely regressive tax.[2]

Recent Macroeconomic History

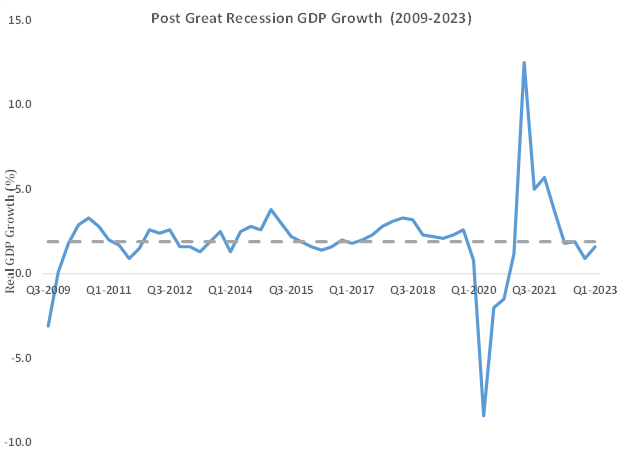

Prior to the onset of the COVID-19 pandemic, there had been a meaningful improvement in the persistence of healthy economic growth over the prior three years. Gross domestic product (GDP) growth, measured as the growth from the same quarter in the previous year, accelerated steadily from a low of 1.4 percent in the 2nd quarter of 2016 to a pre-pandemic peak of 3.3 percent in the 2nd quarter of 2018. Notably, throughout this period, GDP growth remained above the 1.9 percent growth rate that prevailed throughout the 14 years since the Great Recession.

In March of 2020, the COVID-19 pandemic precipitated a historic shuttering of the economy. The broadest measure of economic wellbeing – real quarterly GDP growth – reflected the devastation. The Bureau of Economic Analysis (BEA) estimated that that the economy contracted 8.4 percent between the 2nd quarter of 2019 and the 2nd quarter of 2020 – the single largest drop in real GDP since the Depression-era.

The public policy response was robust, with the combined monetary, fiscal, and administrative actions estimated to be on the order of $11 trillion.[3] The most conspicuous of these actions was the series of bipartisan measures that were enacted in 2020. Through a combination of public policy, effective vaccines, and more than a fair amount of grit from the American public, the nation and the economy recovered rapidly, such that the economy as measured from the 2nd quarter of 2020 to the 2nd quarter of 2021 had expanded by 12.5 percent. The pace of growth has somewhat tempered in real terms since.

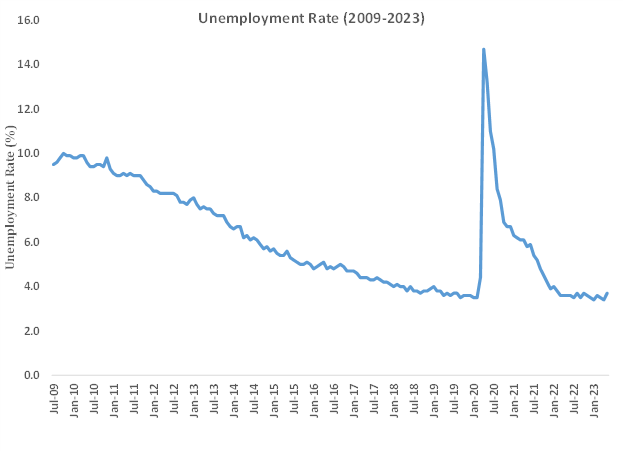

A somewhat similar story can be told of the U.S. labor market. U.S. unemployment gradually moderated over the last decade, before finally bouncing near historic lows. In February of 2020, the regular unemployment rate stood at 3.5 percent. Just one month later unemployment had shot up to 14.7 percent, the highest rate and largest monthly increase in dataset going back to 1948.[4]

But robust policy actions by Congress and the Federal Reserve combined with an improved public health outlook provided for a rapid recovery in the labor market from the depths of the pandemic. Yet somewhat differently than the pace of real GDP, the labor market remains quite tight such that as recently as last month the unemployment rate remained at lows not seen since the 1960s.

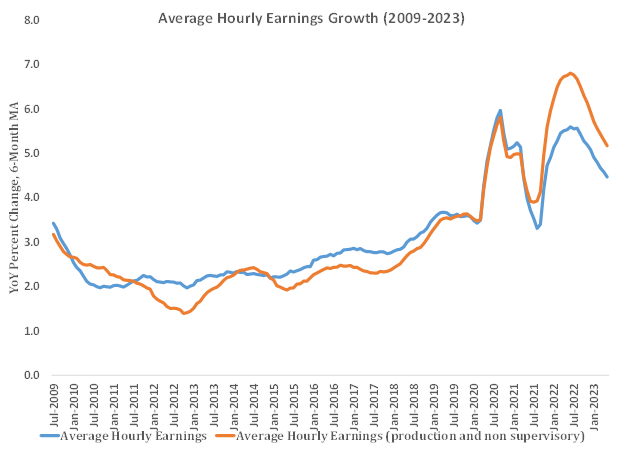

A more nuanced economic history is borne out by the evolution of the pace of nominal average hourly earnings.

Here, we see a somewhat similar trajectory to other major economic indicators over the last decade, reflecting slow building wage growth. Unlike employment, however, earnings growth did not crater but rather have cycled between high and very high rates of growth. This is a feature of a very tight labor market. In the presence of historically high inflation, it reflects an economy running hot.

Rising Inflation and Policy Design

On the fundamental questions as to whether the current inflationary cycle is a function of excess demand or insufficient supply, the answer, of course, is “yes.” Unquestionably, the pandemic imposed somewhat unique challenges on the economy. It was the deliberate policy of the United States to essentially shutter commerce for a significant period of time. The disruptions rippled through every institution in the United States, from government, to schools, to businesses and households.

The U.S. policy response in 2020 was rapid, appropriately sized, and included policies that were well-tailored to the challenge – the Paycheck Protection Program loans are a conspicuous example. The first pandemic-era response, the Families First Coronavirus Response Act (H.R. 6201) was signed into law on March 18th and offered over $300 billion in emergency support for paid family and sick leave for workers and employers. This law was followed soon after by the enactment of the CARES Act, which provided more than $2 trillion in relief and support to households, government agencies, and businesses. Follow-on legislation enacted on a bipartisan basis throughout the year variously extended certain programs to maintain federal support for families and business and ensure government functioning. The last such legislation was the Consolidated Appropriations Act of 2021, which featured about $900 billion in additional relief and support largely modeled on policies in the CARES Act. At the time, inflation as measured by the CPI was 1.4 percent year-on-year and real GDP grew 3.9 percent on an annualized basis in the 4th quarter of 2020.[5]

Subsequent policy changes marked a break from the bipartisan tradition that largely characterized the congressional response to the pandemic. On March 19, President Biden signed into law the American Rescue Plan Act, which injected on the order of $1.9 trillion into the economy. Setting aside the policies within the Act, which were somewhat inconsistent in design with past coronavirus-response measures, the Act was quite simply too big.

According to the Congressional Budget Office (CBO), the gap between the capacity of the U.S. economy to grow and actual economic performance – known as the output gap – was about $380 billion for the rest of the year.[6] At the time, the U.S. economy was growing at 6.3 percent annualized. The upshot is that Congress and the administration gave a massive injection of fiscal stimulus at a time when it needed it least – within two months inflation had nearly doubled before doubling again in the subsequent months. It is important to note that while other global economies faced rapid inflation – the United States was a conspicuous frontrunner subsequent to the enactment of the American Rescue Plan. That excessive stimulus uniquely contributed to U.S. inflation has been found in research published by Federal Reserve banks.[7]

Unquestionably there are global forces at work that can and ultimately do swamp the effects of temporary legislation. There is a temptation to identify a single cause of America’s inflation challenge. The reality is that it is a challenge with myriad interactions and lags. Economies around the world have been grappling with the same challenges that confronted the United States. Many of these challenges are beyond the direct control of policymakers. Accordingly, while I want to emphasize that no single policy change is responsible for the current inflation challenge, to the extent legislation is within the direct control of policymakers, the American Rescue Plan stands out as a significant policy error.

And it was a foreseeable error. As noted, the output gap was about $380 billion at the time. According to the nonpartisan Committee for a Responsible Federal Budget, the American Rescue Plan was plainly excessive, and was sufficient to close the output gap “two to three times over.”[8] The analysis, which assessed the tradeoffs in such a policy identified the risks of inflation and noted that CBO may have overestimated the relevant output gap. If nonpartisan analysis was an insufficient deterrent, Congress could have availed itself of the warnings from key members of President Obama’s economic team and other well-known “doves” that the ARP was excessively large.[9]

Policy Considerations in an Era of High Inflation

The Federal Reserve, as per its dual mandate, is charged with maintaining price stability. The Central Bank’s rapid tightening of monetary policy, and eventually improved public comments on the likely course of monetary policy have done and will continue to do most of the work in bringing stubborn inflation under control. This body nevertheless has an important role to play by pulling in the same direction.

Congress has a somewhat uneven record since the enactment of the American Rescue Plan.[10] The Inflation Reduction Act, for instance, was found to have no effect on inflation by CBO and Penn Wharton.[11] Policies such as the CHIPs Act must be balanced against the risk of additional inflationary measures. Most recently, the Fiscal Responsibility Act could modestly reduce inflationary pressures through deficit reduction, largely deriving from the Act’s spending caps.[12]

Thank you very much, and I look forward to addressing your questions.

[1] https://www.census.gov/library/publications/2022/demo/p60-276.html

[2] https://oversight.house.gov/hearing/inflation-a-preventable-crisis/dhe-testimony-house-oversight-final-3-9-23-holtz-eakin/

[3] https://www.covidmoneytracker.org/

[4] https://www.bls.gov/opub/ted/2020/unemployment-rate-rises-to-record-high-14-point-7-percent-in-april-2020.htm

[5] https://www.bls.gov/news.release/archives/cpi_01132021.htm; https://www.bea.gov/itable/national-gdp-and-personal-income

[6] https://www.cbo.gov/system/files/2021-02/51135-2021-02-economicprojections.xlsx

[7] https://www.frbsf.org/economic-research/publications/economic-letter/2022/march/why-is-us-inflation-higher-than-in-other-countries/; https://www.federalreserve.gov/econres/notes/feds-notes/fiscal-policy-and-excess-inflation-during-covid-19-a-cross-country-view-20220715.html#:~:text=Our%20back%2Dof%2Dthe%2D,ppt%20in%20the%20United%20Kingdom.

[8] https://www.crfb.org/blogs/how-much-would-american-rescue-plan-overshoot-output-gap

[9] https://www.crfb.org/blogs/voices-skeptical-size-19-trillion-covid-relief-plan

[10] https://www.americanactionforum.org/insight/is-congress-helping-or-hurting-inflation/

[11] https://budgetmodel.wharton.upenn.edu/issues/2022/8/5/inflation-reduction-act-comparing-cbo-and-pwbm-estimates

[12] https://www.americanactionforum.org/insight/highlights-of-the-fiscal-responsibility-act/