Weekly Checkup

January 10, 2025

Bad Credit, Worse Care: CFPB’s New Rule

On Tuesday, the Consumer Financial Protection Bureau (CFPB) issued a final rule amending Regulation V – a CFPB regulation implementing the Fair Credit Reporting Act that aims to protect consumers from identity theft and other harmful data practices – to prohibit creditors from assessing consumers’ medical debt and lenders from considering consumers’ medical information when making lending decisions. This new rule is marketed as a solution to lighten the burden of medical debt on U.S. consumers, but it does not eliminate medical debt in any way. It merely hides it.

This will backfire. Hiding such information creates an incentive to pay anything but medical debt. Faced with non-payments, providers will reduce access to health care in the long-term. Let’s review how this rule would work and why it may lead to worse health care outcomes.

The CFPB’s final rule amends two components of Regulation V. First, it removes a creditor’s ability to assess consumers’ medical debt by prohibiting reporting agencies from including this information in credit reports and credit scores shared with lenders. Second, the rule prohibits lenders from considering consumers’ medical information when making lending decisions, preventing lenders from assessing consumers’ medical devices as collateral for loans.

While this final rule will improve the credit scores of some consumers by hiding their medical debt (increasing their probability of qualifying for improved loans and mortgages), it will also likely cause consumers to drastically increase all non-health care spending, while decreasing the likelihood that they pay down their medical debt. In response, doctors and other providers would likely shift the costs of their services from a credit repayment model to an upfront cash payment model to ensure they continue to receive compensation. While this shift likely won’t alter the actual cost of health care services, the same subprime consumers this rule was designed to help will likely bear the largest impact of this shift. A cash-upfront model would ensure that only patients with disposable cash receive priority care. Patients with poorer credit – who likely don’t have disposable cash – would lose access to timely and quality care.

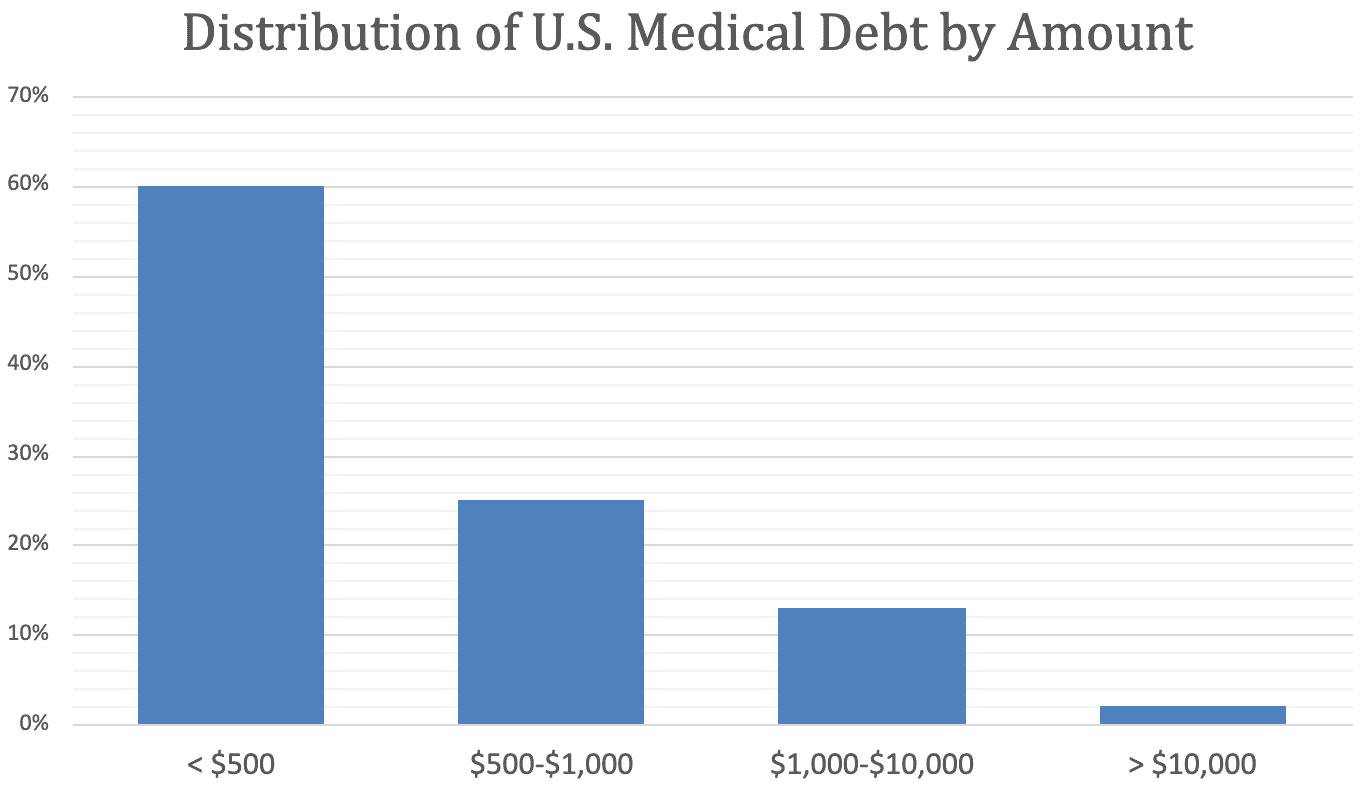

What’s more, as shown in the chart (below), it is not clear that U.S. medical debt is truly the national emergency lawmakers and activists claim. As of June 2021, roughly 60 percent of medical debt was below $500, and about 85 percent was below $1,000. Even if it is a sincere attempt to address the burden of consumer medical debt, the CFPB’s new rule makes risk assessment worse and access to medical care more difficult. It should not see the light of day.

Chart by Parth Dahima, Health Care Data Analyst

Source: CFPB data as of June 2021

Source: CFPB data as of June 2021