Weekly Checkup

April 10, 2026

CY 2027 MA Rate Announcement: A Bigger-Than-Expected Increase, but Not a Blank Check

This week, the Centers for Medicare and Medicaid Services (CMS) released the much-anticipated Calendar Year (CY) 2027 Medicare Advantage (MA) and Part D Rate Announcement. It was a materially different outcome than the industry was bracing for, with CMS projecting a net impact on expected average change of 2.48 percent – amounting to more than $13 billion in additional payments to MA plans. This is dramatically higher than the .09 percent increase it had projected in January. Rather than approaching MA as a program to be upended, redesigned, and squeezed for savings, the administration seems to have opted for some stabilization while still subjecting plans to targeted payment-integrity constraints.

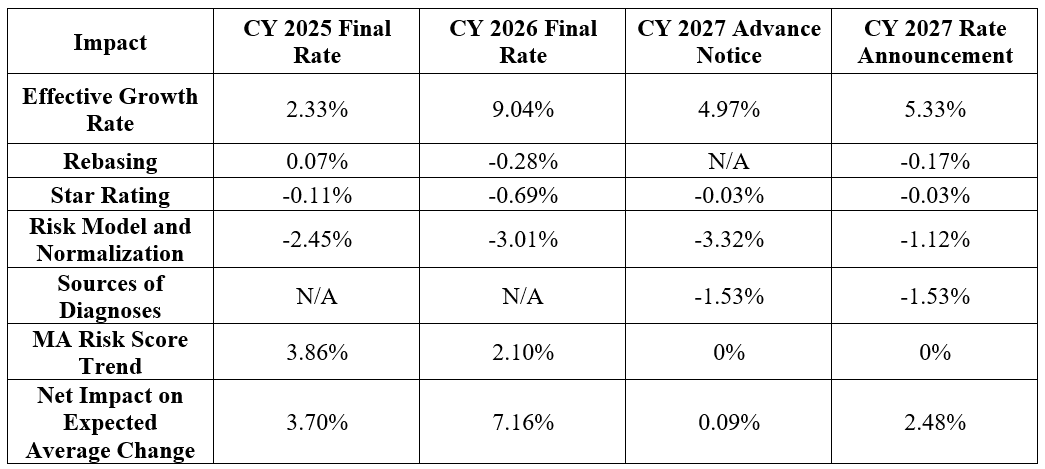

Below is a table showing the various components that make up the Rate Announcement and demonstrating the percentage change by year. The American Action Forum has previously broken down each of these factors here and here.

Source: Centers for Medicare and Medicaid Services

Source: Centers for Medicare and Medicaid Services

The biggest reason for the percent jump from the Advance Notice to the final Rate Announcement is not simply better underlying growth data, though that helped. CMS’ substantially lighter final treatment of the “risk model and normalization” category, which improved from -3.32 percent in the Advance Notice to -1.12 percent in the final policy, was key in mitigating an exorbitant cut to MA payments. The effective growth rate increased, rising from 4.97 percent to 5.33 percent. The “sources of diagnoses” adjustment remained fixed at -1.53 percent, while the Star Ratings effect remained unchanged at -0.03 percent and MA risk score trend stayed at 0 percent. In other words, the final payment improvement was driven chiefly by a much less punitive risk model and normalization adjustment, not by a wholesale retreat from CMS’ coding-integrity agenda. At the same time, the agency chose not to implement the updated 2027 CMS Hierarchical Condition Categories (CMS-HCC) risk adjustment model and instead will continue using the 2024 model for CY 2027, explicitly citing concerns about stability in the MA market and the desire to give plans more time to adjust to the completed phase-in of the 2024 model.

This balance of payment amount versus policy change is important context; the improved $13 billion figure should not be read simply as a windfall for insurers. It is better understood as a signal that CMS recognizes the extent to which MA has become too central to Medicare to destabilize casually. MA enrollment has surpassed 35 million people, and more than half of eligible Medicare beneficiaries now receive coverage through the program rather than fee-for-service Medicare. Against that backdrop, a near-flat update would have risked further plan exits, benefit retrenchment, and more disruption after a year in which insurers were already trimming offerings in some markets. The final notice therefore suggests that CMS is trying to preserve plan participation and bid stability for 2027, even while leaving in place several policies intended to limit inappropriate payment growth.

That, in turn, is what this Rate Announcement may portend for the future of Medicare Advantage. The final notice should not be mistaken for a return to the more generous payment environment of recent years. The broad direction is supportive, but not permissive. CMS states outright that the final policies are intended to support the program while advancing “a sustainable and credible Medicare Advantage program in the long run,” and that the targeted risk-adjustment policies are meant to promote “greater competition and more accurate payments.” In other words, the future of MA under this framework is unlikely to be one of retrenchment. But it is also unlikely to be a return to an era in which plans could count on sustained support for growing enrollment. Today’s announcement seems to affirm that MA will continue to grow and remain important, but that growth will increasingly be paired with more scrutiny of how plans document risk and justify payment.

The most notable example of the payment versus program integrity balance is underneath the headline payment increase. CMS finalized its proposal to exclude diagnoses from unlinked chart review records, while carving out an exception for beneficiaries who switch from one MA organization to another. The CMS fact sheet indicates that this sources-of-diagnoses policy still carries a -1.53 percent impact on average, and CMS’ economic analysis estimates that excluding diagnoses from audio-only services and unlinked chart review records, with the switcher exception, will generate $6.84 billion in net Medicare savings. That is a significant policy choice. Even while increasing benchmark payments overall, CMS is continuing to go after coding pathways it views as less reliable or less consistent with program integrity.

Several other items in the publication are worth watching. Rebasing and repricing now carry a modest -0.17 percent effect, and the drag from Star Ratings changes remains relatively small at -0.03 percent. CMS also notes that, without the switcher exception, the impact of excluding unlinked chart reviews would have been even steeper, at -1.78 percent. And while diagnoses tied solely to audio-only encounters will be excluded, CMS says the average payment effect from that specific change is 0 percent, suggesting the agency views it more as a technical and documentation-consistency issue than as a major savings lever. These details reinforce the larger theme: The final announcement is more generous on aggregate payment, but it is still calibrated to preserve CMS’ leverage over risk adjustment and coding policy.

CMS appears to have settled, at least for now, on a governing posture toward Medicare Advantage that combines accommodation with constraint: more money up front, more program rigor underneath. That likely means the future of MA remains one of continued enrollment growth and policy centrality, but also of continued fights over risk adjustment, coding intensity, audits, and the appropriate boundaries of plan payments. The increase is therefore best seen not as agency capitulation, but as the price of maintaining stability in a program that has become too large for policymakers to squeeze and too contentious to leave unscrutinized.