Weekly Checkup

June 26, 2026

Criminalizing Insurance Decisions Creates Unworkable Law

Few parts of health care generate more public anger than a denied insurance claim. Patients meet coverage rules at the worst possible moment: after a diagnosis, before a procedure, or while trying to fill a prescription. Physicians complain that prior authorization and utilization review interrupt care and bury clinical practice under paperwork. Frustration may be justified, but frustration is not a criminal-law standard, and anger at insurers is not a substitute for workable health policy.

This simple fact is the initial (but not sole) problem with Pennsylvania House Bill 2611. The proposal would create a new offense, “aggravated assault of an insured,” aimed at the chief executive officer – or highest-ranking decision-maker – of a health insurer when an insured person receives an adverse benefit determination for a medically necessary benefit, and that determination results in serious bodily injury or death. Supporters say that this is accountability for insurers that put profits ahead of patients. Instead, it is a reckless attempt to shoehorn a disputed coverage decision into a violent crime.

Pennsylvania already regulates fully insured health coverage through insurance law, and patients have appeal rights, including external review when a plan denies care. These processes can be too slow or opaque, but they are designed for the actual question at issue: whether a service is covered, medically necessary, supported by the record, and required under the policy. HB 2611 would move that dispute from insurance regulation into criminal prosecution.

That shift raises immediate legal problems. Criminal law typically requires personal culpability. Aggravated assault is not supposed to punish a bad corporate outcome; it is supposed to punish conduct that is intentional, knowing, or sufficiently reckless to justify a serious charge. Yet insurance denials are rarely made personally by CEOs. They are made through plan terms, medical policies, utilization management protocols, clinician reviewers, delegated vendors, employer benefit designs, and state and federal rules. Holding a CEO criminally liable because that process produced a disputed denial collapses management responsibility into criminal guilt.

Causation would be just as difficult to prove. A patient’s injury or death after a denial does not prove that the denial caused the harm. Disease progression, provider delay, incomplete documentation, treatment risk, coverage exclusions, clinical disagreement, and alternative covered therapies may all be relevant. Prosecutors would have to reconstruct medical necessity, coverage, timing, and causation after the fact. That is a poor fit for aggravated assault law.

The bill also risks vagueness. “Medically necessary” may sound straightforward, but it often depends on evidence, diagnosis, setting, clinical criteria, benefit design, and the information submitted at the time. “Adverse benefit determination” can include several types of denials or payment disputes. If Pennsylvania wants to impose criminal punishment, it must define the prohibited conduct with far greater precision than a retrospective conclusion that a denied service was necessary and harm later followed.

The proposal’s reach is likely to be uneven. Large employer self-funded plans are generally governed by federal Employee Retirement Income Security Act of 1974 (ERISA) rules, not ordinary state insurance mandates. That means the bill may hit some insurers while missing many coverage arrangements that patients experience as “insurance.” A criminal statute that cannot reach much of the market is not a coherent patient-protection strategy.

The practical effects could be damaging. Insurers would have an incentive to approve marginal or incomplete requests – not because the care is appropriate, but because denial creates legal risk for corporate leadership. That might sound like a victory until the costs arrive in higher premiums, weaker cost controls, and more pressure on families. The insurer is not a public benefactor with unlimited resources; it administers pooled funds that patients, employers, and taxpayers ultimately finance. Companies facing criminal exposure may also add legal review, escalation, and defensive bureaucracy, leaving patients with a system that is more expensive, more rigid, and no more responsive.

There are better answers. Pennsylvania can tighten prior authorization deadlines, require clearer denial notices, strengthen expedited appeals, expand external review, audit high-denial plans, publish denial and reversal data, and impose civil penalties for repeated violations. Those reforms target the real problem: a coverage-review process that too often feels opaque, slow, and stacked against patients.

HB 2611 is dangerous, punitive symbolism masquerading as reform. Pennsylvania may want to improve insurance accountability, but it should not criminalize coverage disputes or pretend that aggravated assault law is a tool for health care administration. This bill would make bad incentives worse, invite litigation, and leave patients with a system angrier, costlier, and no more humane.

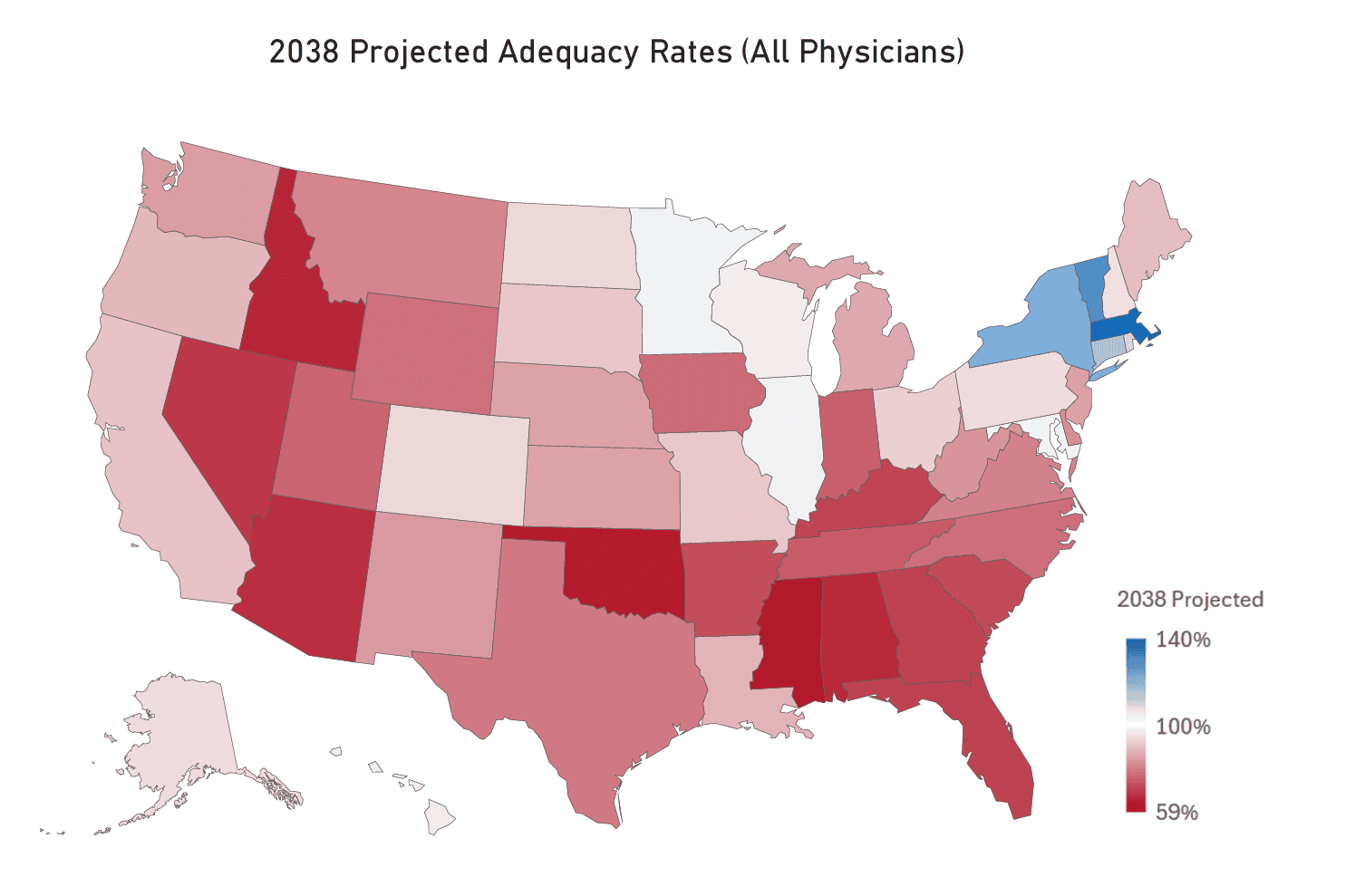

Chart Review: Widening Physician Shortage Threatens Access to Care Across America

Evan McLaughlin, Health Policy Intern

The United States is currently experiencing a physician shortage that is projected to worsen significantly, with a disparate impact across the country. The Health Resources and Services Administration (HRSA) projects a national shortage of 141,160 physicians by 2038, at which time the vast majority of states will have a physician adequacy rate under 100 percent. Those facing the worst shortages are concentrated in the Deep South and Mountain West in states such as Idaho, Mississippi, Nevada, and Oklahoma, as seen on the map below. HRSA projections also indicate a growing divide between metropolitan statistical areas (MSAs) and non-MSAs, with MSAs projected to have a 95-percent adequacy rate compared with just 42 percent in non-MSAs.

Broader workforce trends suggest these shortages may be difficult to address, with roughly a third of currently active physicians expected to retire in the next decade. At the same time, growth in residency training capacity remains constrained because of the federal cap on the number of residency positions that can be funded by Medicare. The federal government helps fund more than three-quarters of medical residencies nationwide – making this a key channel for shaping physician workforce supply. Geographic disparities compound the problem: Just 2 percent of Medicare-funded residencies occur in rural areas due to a high concentration of medical education in urban teaching hospitals. Without reform, these trends could significantly reduce health care access in many rural and underserved communities.