Weekly Checkup

June 5, 2020

The Need for Liability Protection as Businesses Reopen

Last month the Trump Administration began to pivot its messaging toward “reopening” America, encouraging states to start lifting restrictions on population movement and business operations. Reopening among businesses, however, has been slow. With 40 million new unemployment applicants so far during the pandemic, and reason to believe those numbers will grow worse before they improve, businesses are clearly not heeding the White House rhetoric. There are a number of reasons why businesses have been slow to reopen, but one of the foremost is legal liability.

Business owners face a number of headwinds that impede movement toward reopening and rehiring. For one thing, the enhanced unemployment benefits provided by the Coronavirus Aid, Relief, and Economic Security (CARES) Act through the end of July mean that many employees are better off financially if they delay returning to work. For another, many employees will need to care for children who are out of school and have nowhere to go this summer. But before employers can worry about how to bring their employees back, they need to decide how to ensure the safety of their employees once they do return. Businesses, already hurt by several months of quarantine policies and in some cases additional financial impact from the ongoing unrest in most major U.S. cities, must be leery about opening themselves up to lawsuits from employees and customers in the event that someone contracts COVID-19 as a result of their operations.

Around the country, states such as Mississippi, South Carolina, and Connecticut, among others, are beginning to debate liability protections for businesses as they reopen. In other circumstances a state-by-state approach would be preferable, and even in this situation some variation between states and localities given different populations and risk may be appropriate. Amid a global pandemic, however, federal intervention to set minimum standards might be necessary. Senate Majority Leader Mitch McConnell has called for liability protections for employers that take appropriate steps to protect their workers and customers, and the White House has embraced the idea. On the other hand, House Democrats have dismissed the idea out of hand, and there is strong opposition from their union and trial-lawyer allies. Opponents argue that blanket immunity from liability will lead to carelessness and negligence, but no one is actually suggesting blanket immunity.

The Occupational Safety and Health Administration (OSHA)—in cooperation with the Centers for Disease Control and Prevention—has already issued guidance on workplace standards for COVID-19. That guidance, however, is explicitly not a standard or regulation and in OSHA’s own words “creates no new legal obligations.” At the same time, compliance with those guidelines would not necessarily provide legal immunity. OSHA could issue clear, mandatory requirements for employers looking to reopen, and Congress could then tie liability protection to compliance with those or some alternative set of federal guidelines. Businesses that do not take appropriate steps to protect employees and the public should not be protected from the consequences of their negligence, but asking businesses to guess at what courts will find to be sufficient mitigation efforts is equally unfair and will impede any return to economic activity endorsed by public health officials.

Employers will have to shoulder the bill for addressing COVID-19 in the workplace; that’s simply the reality of doing business for the foreseeable future. But Congress and the administration should act, based on the recommendations of public health officials, to clarify what constitutes a safe workplace and to protect already-reeling businesses from frivolous lawsuits that will further impede any economic recovery from the pandemic.

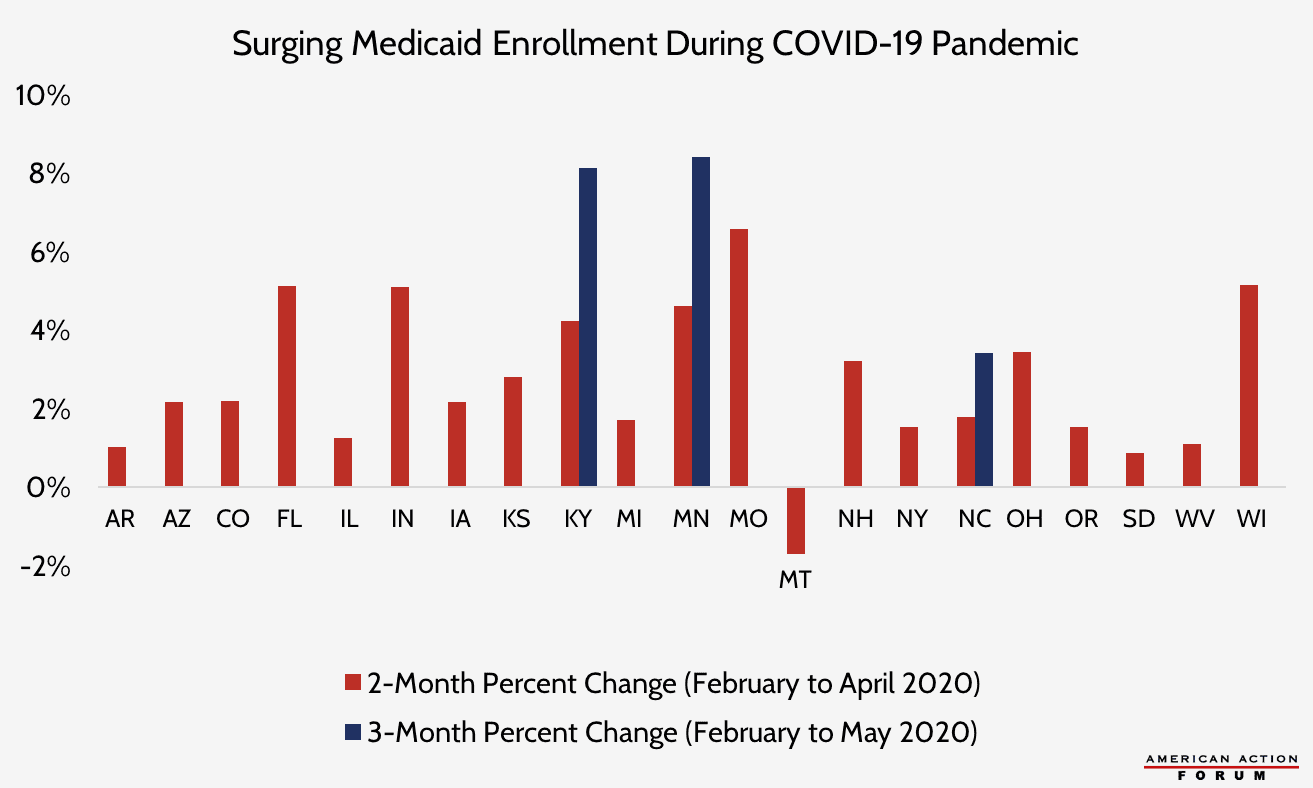

Chart Review: Surging Medicaid Enrollment During the COVID-19 Pandemic

Margaret Barnhorst, Heath Care Policy Intern

With millions losing employer-sponsored insurance (ESI) because of the COVID-19 pandemic, the Kaiser Family Foundation predicts that Medicaid will be the most important public source of coverage following this loss. Of the estimated 26.8 million people losing ESI, nearly half—12.7 million—will become eligible for Medicaid. This figure likely does not capture the total surges in Medicaid enrollment as a result of the pandemic, however, as many low-wage workers did not have ESI to begin with but could still become eligible for Medicaid following job loss. Medicaid enrollment data from 21 states show that total enrollment increased, on average, by 2.8 percent between February and April 2020—much higher than the 0.2 percent increase seen during this same time period in 2019. Missouri had the largest increase (6.5 percent) and South Dakota had the smallest (0.9 percent); Montana was the only state to see a decline in Medicaid enrollment over this period. Three states have released Medicaid enrollment data for May 2020, with increases as high as 8 percent over the 3-month period suggesting continued enrollment surges in the coming months. In response to these anticipated surges in Medicaid enrollment, the Families First Coronavirus Response Act instituted a freeze on involuntary disenrollment until after the national emergency is lifted, as well as increased the federal government’s share of Medicaid expenditures. A previous AAF analysis estimated these changes will increase federal Medicaid spending by $11 billion per quarter that the public health emergency declaration remains in effect.

Data obtained from individual state Medicaid websites, compiled by Georgetown University Health Policy Institute

Worth a Look

Health Affairs: Varying Trends In The Financial Viability Of US Rural Hospitals, 2011–17

Reuters: U.S. working with manufacturers to boost flu vaccine availability, top official says