Weekly Checkup

June 5, 2026

Biotech IPOs: Avoid Crowding Out the Market

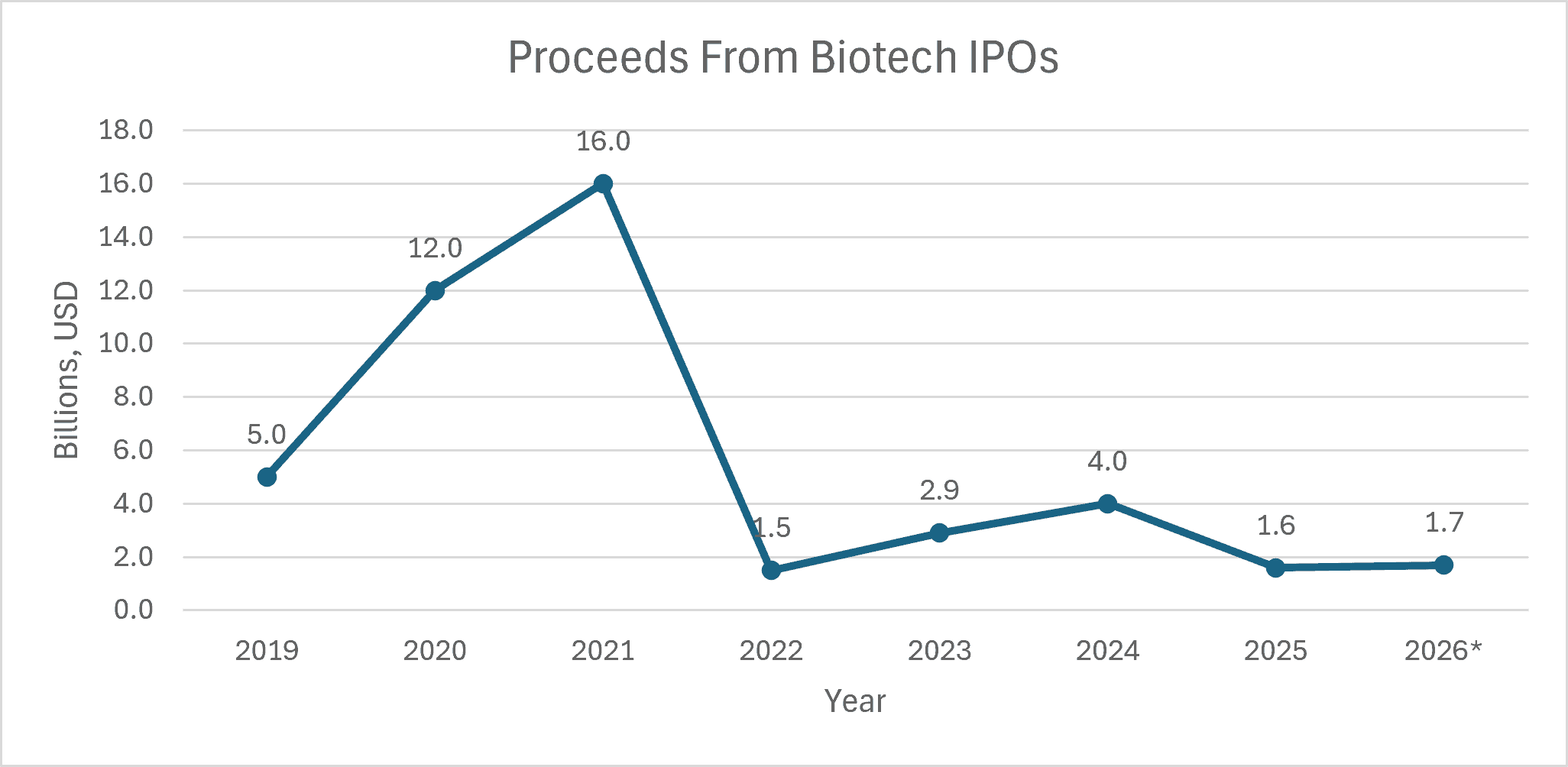

Biotechnology’s initial public offering (IPO) market is showing signs of life again, but it remains a fragile recovery. After the extraordinary 2021 boom (fueled in part by the COVID-19 pandemic) – more than 100 biotech companies went public and raised nearly $16 billion – the door largely shut. Macroeconomic conditions were an obvious drag on biotech IPOs, but policy uncertainty likely compounded the slowdown. A sector dependent on long investment horizons has had to absorb uncertainty around Medicare drug pricing caps, a general regulatory skepticism of industry consolidation, a hostile regulatory posture from the Securities and Exchange Commission (SEC), and broader questions about the future return on biomedical innovation.

In 2025, only 11 drugmakers priced initial public offerings. Thankfully, the early 2026 market looks more propitious. Six drugmakers that went public in the first quarter raised a combined $1.7 billion, and the median biotech IPO raised $287.5 million – the highest quarterly median since 2021. Investors are returning, but mostly for companies with later-stage programs, clearer clinical proof, and a more credible path to value creation, demonstrating a more cautious approach relative to the rest of the market.

*2026 values through Q1; Source of valuations: Biopharma Dive

*2026 values through Q1; Source of valuations: Biopharma Dive

An IPO is far more than a mere vanity milestone for any company, especially a biotech firm. It is often a necessary stage in company maturation. Public capital can extend cash runway, reduce dependence on tightly negotiated private rounds, strengthen a company’s bargaining position in partnership or acquisition talks, and allow management to fund clinical development on a scientific timeline rather than a survival timeline.

Strong capital markets also change the way a biotech company can plan. Drug development is not an incremental software iteration. Promising therapies still must pass toxicology assessments, endpoint selection, dose selection, patient recruitment in clinical trials, manufacturing controls, Food and Drug Administration (FDA) review, and payer adoption. Each step consumes capital long before revenue exists. For a company trying to move from Phase 1 signal to Phase 2 proof of concept, or from Phase 2 data to a pivotal trial, access to deeper capital markets can determine whether the next study is launched, delayed, narrowed, or abandoned.

Recent biotech IPOs have been larger and more clinically mature than the offerings of the past several years. Nearly all of this year’s IPO class has had drugs in Phase 2 or Phase 3 testing, with many raising $250 million or more. That is exactly what the public market should be doing: funding companies that have moved beyond early discoveries and now need serious capital to deepen research, advance trials, and test whether promising science can become real medicines.

There is a risk that this delicate reopening could be overwhelmed by a very different kind of IPO. SpaceX, OpenAI, and Anthropic are being discussed as the defining public-market events of 2026. The shock factor is difficult to overstate. SpaceX has a reported plan to raise $75 billion at a $1.75 trillion valuation. OpenAI has reportedly prepared for an IPO that could value the company at up to $1 trillion. Anthropic, meanwhile, has confidentially submitted a draft S-1 – a company’s initial pre-IPO filing to the SEC – and recently announced a $65 billion funding round at a $965 billion post-money valuation.

Those numbers are breathtaking. They also raise practical capital-market questions: How much investor attention can the IPO market absorb at once? And how many investor dollars will still be available in the second half of 2026?

In theory, public markets are deep enough to fund many sectors simultaneously. In practice, IPO windows depend on risk appetite, liquidity, portfolio allocation, and narrative momentum. A trillion-dollar technology debut does not merely compete for dollars; it competes for attention. Growth funds that might otherwise consider investing in a Phase 2 immunology company, an oncology platform, or a rare-disease developer may instead reserve capital for the next AI or aerospace infrastructure giant. Generalist investors, whose participation is often needed to make larger biotech offerings work, may be pulled even further toward technology.

The result may not be a closed biotech window, but a narrower one. A narrow window means fewer issuers, lower valuations, smaller proceeds, more dilutive offerings, and longer waits for companies that are ready to go public but cannot command attention. Some companies will stay private longer and raise more expensive venture rounds. Others may cut programs, delay trials, or seek acquisition before their science has had time to mature. For biotech, delayed capital formation can become delayed clinical development.

There is also a broader policy point. Policymakers frequently talk about U.S. leadership in biotechnology, domestic innovation, biomedical preparedness, and the need to convert innovative medical discoveries into treatments. Those goals require more than National Institutes of Health funding, FDA efficiency, or the avoidance of price caps. They also require functioning capital markets. If the public market becomes overwhelmingly organized around a handful of spectacular technology narratives, it becomes less useful for financing diversified innovation.

To be clear, companies such as SpaceX, OpenAI, Anthropic – or the next Kailera Therapeutics – should be able to access public capital. That is one of the United States’ core capitalist strengths. But their scale may test whether the 2026 biotech IPO recovery is broad-based or merely a rotation toward a few extraordinary names. A functioning IPO market helps bridge the gap between scientific promises and commercial viability, funding both the next dominant technology platform and the next generation of medicines. If it cannot do both, the cost will not simply be fewer biotech tickers. It will be fewer opportunities to capitalize on innovation for patients waiting for treatments.