Weekly Checkup

June 12, 2026

Medicare’s Solvency Warning Is Getting Harder to Ignore

The 2026 Medicare Trustees Report has reiterated what policymakers should already know: Medicare’s financing problem is not hypothetical, distant, or self-correcting. The Trustees project that Medicare’s Hospital Insurance (HI) Trust Fund will be able to pay full scheduled benefits only until the second quarter of 2033, after which continuing program income would cover only 89 percent of scheduled benefits. The American Action Forum has reviewed the highlights of this latest report, but in a nutshell – the HI Trust Fund is on a path toward depletion.

Understanding the HI trust fund – which finances Medicare Part A benefits – hinges on the word “insolvency.” But this can make the problem sound more abstract than it is. Medicare will still exist in 2033. Payroll taxes will still be collected. Seniors will still need hospital care. But dedicated Part A financing will no longer be sufficient to pay full scheduled benefits. Under current law, the program cannot simply borrow its way through the gap. At the point of insolvency, Congress would have two options. It could either allow the required benefit cuts, or it could enact legislation crafted under pressure to raise taxes or authorize transfers from the rest of the federal budget. That is no way to govern the largest federal health program.

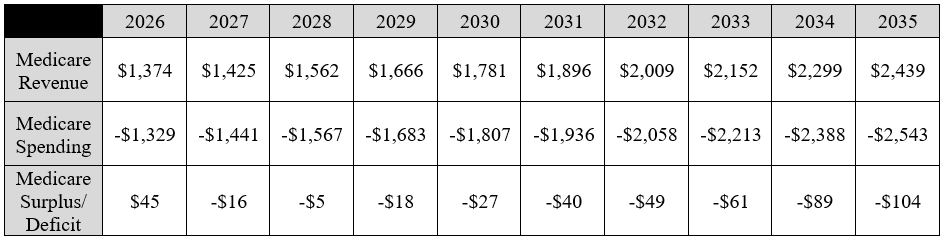

Medicare spent more than $1.2 trillion in 2025 across its HI and Supplementary Medical Insurance trust funds. The Trustees project Medicare costs will rise from 4.1 percent of gross domestic product in 2026 to 6.5 percent in 2050, steadily claiming a larger share of national output, taxpayer resources, and beneficiary income.

Projected Annual Medicare Revenues and Expenditures

Source: 2026 Medicare Trustees Report

The fiscal pressure on the primary health care program for older Americans is not coming from demographics alone. Recent policy choices have added new layers of strain. The Inflation Reduction Act’s Medicare provisions were sold primarily as drug-pricing reforms, but the law also redesigned Part D in ways that shift liability across plans, manufacturers, beneficiaries, and the federal government. The new out-of-pocket cap is valuable to high-cost beneficiaries, but it also changes utilization incentives and plan liability. When policymakers reduce beneficiary cost-sharing, those costs do not vanish. They move.

That movement is visible. Ahead of the 2025 benefit redesign, Centers for Medicare and Medicaid Services (CMS) created a Part D premium stabilization demonstration to suppress premium increases in standalone drug plans. The Government Accountability Office reported that, without the demonstration, monthly premiums for beneficiaries remaining in standalone drug plans would have nearly doubled on average from 2024 to 2025; CMS officials estimated the demonstration would cost $9.8 billion in 2025 and 2026. For 2026, CMS reduced the demonstration subsidy and allowed larger premium increases, while the Congressional Budget Office noted that the average Part D bid amount rose sharply before the effects of premium stabilization.

Those are not signs of a program becoming stable. They are signs of a program using administrative tools to mask cost pressures created by statute and inefficient market behavior. The pattern is clear: Medicare policy increasingly relies on federal intervention to hold premiums, bids, or payments in place, while the underlying cost of the benefit keeps rising.

That dynamic is especially important for Parts B and D. Unlike the HI Trust Fund, the Supplementary Medical Insurance Trust Fund is considered adequately financed because beneficiary premiums and federal contributions from the Treasury are automatically reset each year. That financing structure avoids a formal depletion date, but as Part B and Part D spending rises, premiums, deductibles, coinsurance, and general revenue transfers rise with it.

The right response is neither panic nor denial. Congress need not take a hammer and chisel to create a serious, targeted reform agenda that can reduce waste, improve incentives, and extend solvency without damaging access to care. Reform enacted now can be phased in gradually, but delay compresses every option and makes the eventual policy response more painful.

Medicare’s promise to seniors depends on more than annual reassurance. The Trustees have delivered another warning. Congress should treat it as a deadline.

CHART REVIEW: Forced Disenrollment From Medicare Advantage

Evan McLaughlin, Health Policy Intern

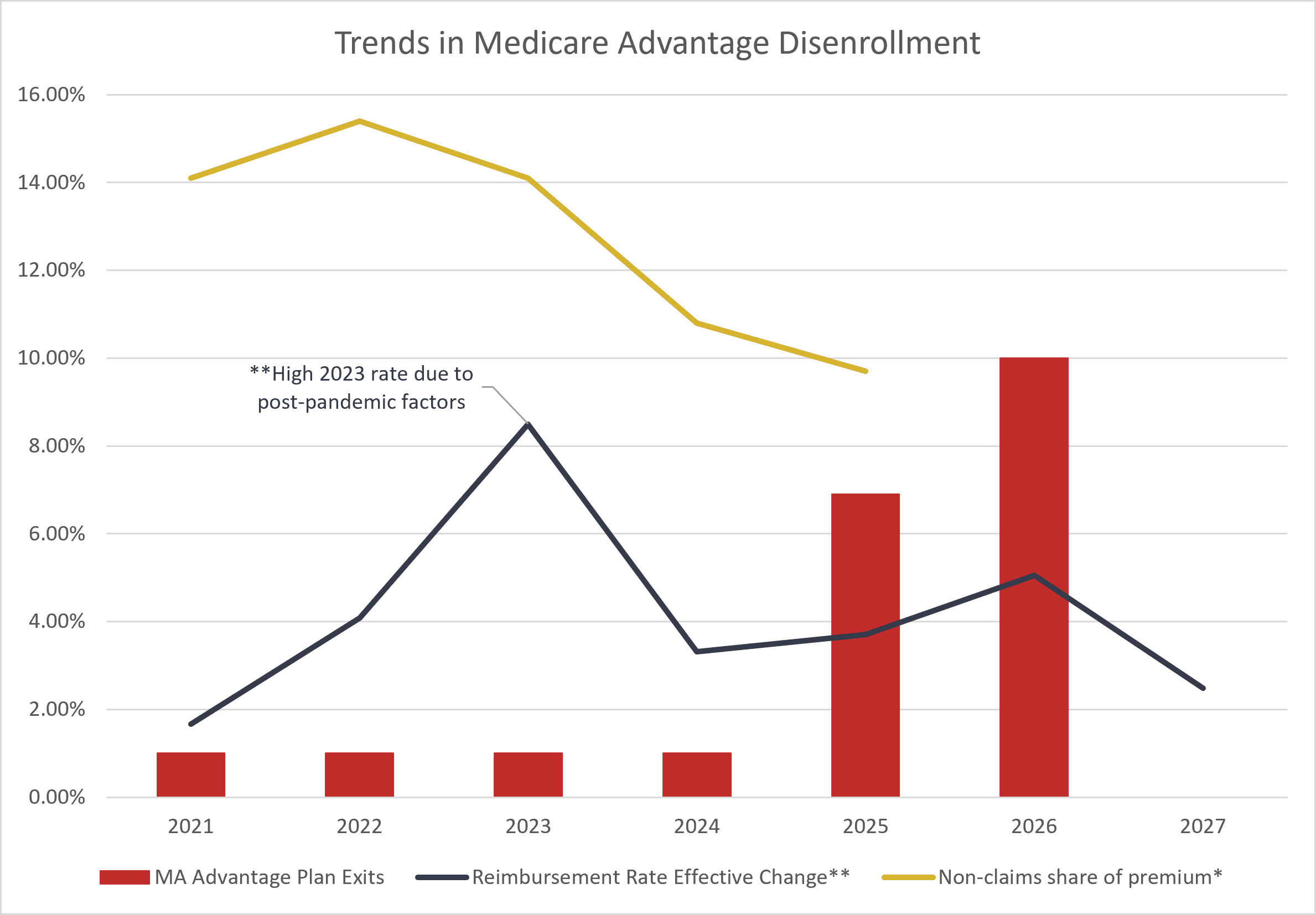

Forced disenrollment from Medicare Advantage (MA) has increased sharply from its historical average of 1 percent of beneficiaries between 2018–2024 to 6.9 percent in 2025 and 10 percent in 2026, according to recent research published in JAMA. Forced disenrollment occurs when beneficiaries must leave their MA plan because the insurer terminates the plan, exits a market, or reduces its service area – thus requiring enrollees to seek a new MA plan or shift to traditional Medicare.

Although multiple factors likely contributed to the sharp rise in forced disenrollment during the past two years, the timing of these developments suggests a plausible relationship between insurer financial pressure and plan availability. The national share of premium revenue after medical claims were paid for MA plans declined from 15.4 percent in 2022 to 9.7 percent in 2025. This reduction reflects a post-pandemic increase in medical utilization and rising health care costs. As margins have narrowed, insurers may rethink plan offerings or exit unprofitable markets. Moreover, some argue that reimbursement rates offered by the Centers for Medicare and Medicaid Services (CMS) have not kept pace with rising nationwide medical costs. Following recent industry feedback, CMS increased the overall expected average rate change for MA plans in 2027 to 2.48 percent, up from the initially proposed rate of 0.09 percent. Still, major insurers have contended that payment increases remain insufficient to offset growing costs and utilization. Without policy solutions, millions of beneficiaries could be required to seek new coverage.

*Non-claims share of premium data from the National Association of Insurance Commissioners.