Insight

March 26, 2025

CBO Estimates Long-term Fiscal Impact of a Permanent TCJA

Executive Summary

- In a recent letter, the Congressional Budget Office analyzed two alternative scenarios and their impact on the nation’s long-term fiscal outlook: One scenario examined the fiscal impact of a permanent, unpaid-for extension of the Tax Cuts and Jobs Act of 2017 (TCJA) and the other examined the fiscal impact of an unpaid-for permanent TCJA and higher interest rates than projected under current law.

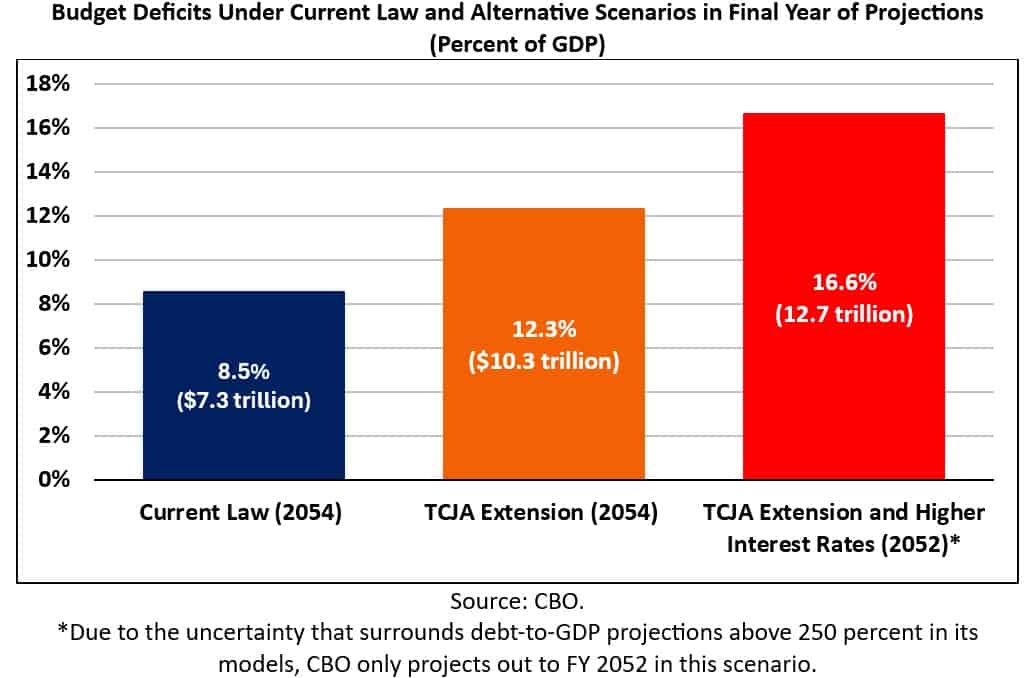

- The first scenario would increase budget deficits by $37.2 trillion through fiscal year (FY) 2054 and as a result debt would rise to 214 percent of GDP by the end of FY 2054, the budget deficit would total 12.3 percent of GDP, and interest payments would grow to 8.6 percent of GDP.

- The second scenario would increase budget deficits by $60.9 trillion through FY 2052 and as a result debt would rise to 246 percent of GDP by the end of FY 2052, the budget deficit would total 16.6 percent of GDP; and interest payments would climb to 12.5 percent of GDP.

Introduction

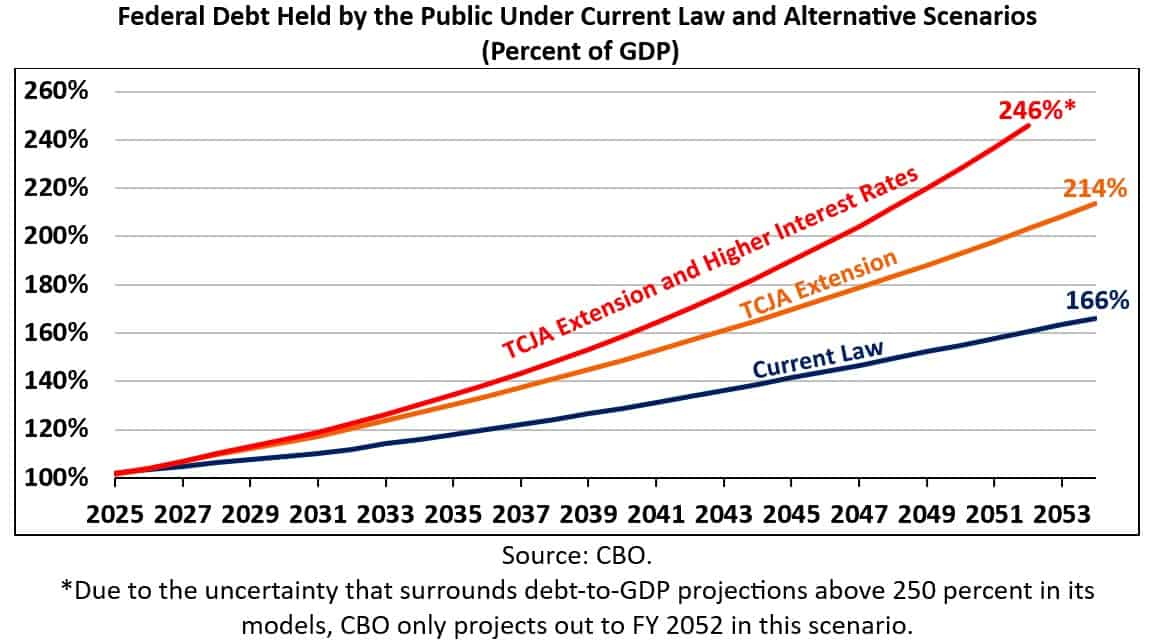

The Congressional Budget Office’s (CBO) March 2024 Long-Term Budget Outlook projects that federal debt held by the public will rise from 102 percent of gross domestic product (GDP) at the end of fiscal year (FY) 2025 to 166 percent of GDP by the end of 2054 under current law. Meanwhile, the budget deficit will grow from 5.5 percent of GDP ($1.8 trillion) to 8.5 percent of GDP ($7.3 trillion) and interest payments on the national debt will climb from 3.3 percent of GDP ($951 billion) to 6.3 percent of GDP ($5.4 trillion). In a recent letter, CBO analyzed two alternative scenarios to show how changes in budgetary and economic conditions would affect the long-term fiscal outlook. The first scenario examined the fiscal impact of a permanent, unpaid-for extension of the Tax Cuts and Jobs Act of 2017 (TCJA). The second scenario examined the budgetary impact of a permanent, unpaid-for TCJA that’s accompanied by higher interest rates than projected under current law. Both scenarios would increase debt, deficits, and interest costs substantially relative to current law.

The Long-term Fiscal Impact of an Unpaid-for TCJA Extension

The TCJA made significant changes to the federal tax code by lowering individual and corporate income tax rates, increasing the standard deduction, doubling the child tax credit, and reforming the international tax regime, among other reforms. In an effort to mask the true cost of these changes and fit them within cost limits, a majority of the TCJA’s individual income and estate tax provisions are set to expire on December 31, 2025. CBO estimates that making the TCJA’s individual and estate tax provisions permanent without offsets would increase budget deficits by $37.2 trillion through FY 2054. As a result, federal debt held by the public would rise to 214 percent of GDP, the budget deficit would total 12.3 percent of GDP ($10.3 trillion), and interest payments on the national debt would climb to 8.6 percent of GDP ($7.2 trillion). Economic output in 2054 would be 1.8 percent ($1.5 trillion) lower and the average interest rate on debt held by the public 30 basis points (0.3 percentage points) higher.

In the second scenario, CBO assumed a permanent, unpaid-for extension of the TCJA’s individual and estate tax provisions and an increase in the average interest rate on federal debt held by the public until it was 100 basis points (one full percentage point) higher than under current law. To do this, CBO incorporated a five-basis-point (0.05 percentage points) annual increase in the average interest rate until it was a full percentage point higher, inclusive of macroeconomic feedback. CBO estimates that a permanent, unpaid-for TCJA that’s coupled with higher interest rates would increase budget deficits by $60.9 trillion through FY 2052. As a result, debt would rise to 246 percent of GDP by the end of FY 2052, the budget deficit would total 16.6 percent of GDP ($12.7 trillion), and interest costs would jump to 12.5 percent of GDP ($9.5 trillion). Debt-to-GDP would eclipse 250 percent by the end of 2054, though the uncertainty that surrounds debt-to-GDP projections above 250 percent in CBO’s models prevented the agency from providing an exact estimate. Economic output in 2052 would be 3.5 percent ($2.8 trillion) lower and the average interest rate on debt held by the public 150 basis points (1.5 percentage points) higher.

Conclusion

CBO’s latest projections show that a permanent, unpaid-for TCJA extension would significantly worsen the long-term budget outlook. As policymakers work to address the TCJA’s looming expiration, they should make an honest effort to offset any extensions.