Insight

March 2, 2026

CMS’ CY2027 MA Advance Rate Notice: Breaking Down Its Components

Executive Summary

- The Centers for Medicare & Medicaid Services (CMS) updates Medicare Advantage (MA) through an annual, highly structured policy and rate-setting cycle that includes the Advance Notice, Rate Announcement, and MA-Part D regulations.

- An important policy signal in this rulemaking process is the Advance Notice, which forecasts CMS’ estimates for any percentage change in capitated rates for MA before the final Rate Announcement in the spring.

- While the Advance Notice is not a final adjudication of what the percentage change in program rates may be, industry relies on the information provided in the Advance Notice to prepare for the yearlong benefit design process for the next plan year.

Introduction

Each year, the Centers for Medicare and Medicaid Services (CMS) begins the Medicare Advantage (MA) payment cycle by issuing an Advance Notice that lays out proposed updates to payment methodology and provides an estimated year-to-year change in plan payments. That estimate is one of the most closely watched numbers in the MA market because it shapes early expectations for plan bids, benefit design, and insurer strategy. After a public comment period, CMS finalizes the policies in the Rate Announcement, which sets the payment parameters plans use as they prepare bids for the upcoming contract year.

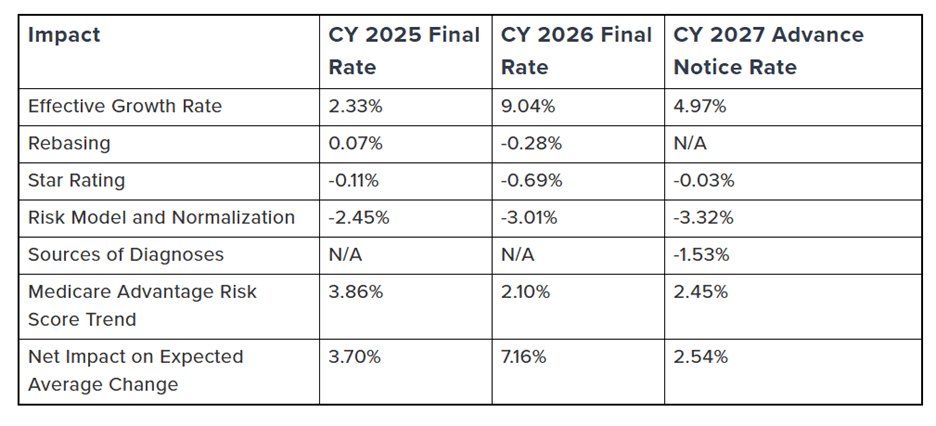

The challenge is that the headline percentage in the Advance Notice is often treated as if it were a single “rate increase” or “rate cut,” when in practice it is neither. It is a net figure built from several moving parts, including benchmark growth, quality payment changes, and risk-adjustment policy updates. In the recently released calendar year (CY) 2027 Advance Notice and accompanying fact sheet, the 0.09-percent expected average change is the product of multiple offsets – some reflecting underlying Medicare cost growth and others reflecting CMS policy choices around payment accuracy and program integrity.

That distinction matters for policy analysis. Before drawing conclusions about whether CMS is tightening or expanding MA payments, it is important to understand what each line in the table is measuring, and what policy objective it is meant to serve. The Advance Notice is also not the ultimate adjudication of that the percentage change in program rates may be, though the industry relies on the notice to adequately plan for the lengthy benefit review and design process.

A Net Calculation, Not a Standalone Input

While the analysis is often focused on the Advance Notice’s topline percentage, its real value is in the component-level methodology, which shows how CMS is balancing benchmark growth, quality incentives, and payment-calibration policies. Read closely, the Advance Notice provides an early map of CMS’s priorities before those proposals are finalized in the annual Rate Announcement. The components include:

Source: The American Action Forum

Even before discussing each line item, one policy lesson is obvious: The table mixes upward trend factors and downward payment-integrity adjustments. In other words, the resultant expected average growth figure reflects offsetting forces, not a flat underlying cost environment. The biggest positive input is benchmark growth, while the largest negative inputs are tied to risk adjustment and normalization, along with the new factor denoted as “sources of diagnoses.”

Analysis of MA Advance Notice Rate Components

Effective Growth Rate Is the Macro Driver

The 4.97-percent Effective Growth Rate is the largest positive component in the table and functions as the core macro-level driver of the update because it is largely tied to growth in fee-for-service (FFS) Medicare per-capita costs as estimated by the Office of the Actuary. That makes this factor fundamentally different from the risk-adjustment and diagnosis-source entries elsewhere in the table. It reflects broad Medicare spending trends rather than plan coding behavior or administrative policy changes, and it is therefore the starting point for understanding the payment update before CMS applies the other adjustments that narrow the net figure. When people talk about whether MA is being funded more generously or more tightly in a given year, they often focus on this line first – but in 2027, it is only one part of the story because other policy changes materially offset it.

Rebasing/Re-pricing Comes Later

While the topline expected average change from the Advance Notice is published as an important market signal, one important but easy-to-miss detail is that Rebasing/Re-pricing is listed as “TBD.” This line depends on finalization of the average geographic adjustment index and is provided in the final Rate Announcement. The rebasing/re-pricing factor is where CMS translates raw FFS experience into a policy-adjusted benchmark base, which means it is often the best indicator of how much “payment trend” is being driven by underlying utilization and pricing versus by technical recalibration of the county rate book itself. Rebasing means CMS updates the historical FFS data window used to build county costs (for CY 2027, CMS moves to a five-year rolling period of 2020–2024 and drops 2019), while re-pricing means CMS takes those historical claims and revalues them using the most current payment rules so the data are comparable to the upcoming payment year. For CY 2027, CMS says that it includes repricing inpatient, outpatient, skilled nursing facilities, and home health claims with current wage indices, repricing physician claims with current geographic practice cost indices, applying durable medical equipment, prosthetics, orthotics, and supplies program repricing rules, and updating uncompensated-care payment treatment.

Star Ratings Is a Small Factor, But Reflects Quality Bonus Policy

The -0.03-percent change in Star Ratings entry is relatively small in magnitude, but it reflects a separate policy channel from benchmark growth and risk-adjustment updates because it captures the estimated effect of changes in Quality Bonus Payments tied to MA Star Ratings. In practical terms, this line is a reminder that the year-to-year percent change table is not solely an actuarial exercise. It also incorporates CMS’ quality incentive framework, which means the overall payment update blends cost trends, technical payment calibration, and quality-based payment policy into one compressed set of percentages.

Risk Model Revision and Normalization Is the Central Policy Lever

The -3.32-percent Risk Model Revision and Normalization line is the most consequential downward component in the CY 2027 table and, from a policy perspective, the clearest signal of CMS’ continued focus on payment calibration within MA. CMS presents risk model revision and normalization together because the two interact substantially, and it also notes that normalization alone would have a smaller impact (about -1.50 percent) absent the model update. It is a composite effect tied to risk-adjustment design, calibration, and normalization. CMS also notes elsewhere in the fact sheet that it is proposing updates to the Part C risk model using more recent FFS Medicare data while continuing to use the V28 clinical classification framework. This line item is not simply a blunt budgetary adjustment, but a combined methodological change tied to how risk scores are calculated and scaled for payment purposes.

“Sources Of Diagnoses” Is a Payment-accuracy and Integrity Decision

CMS’ CY 2027 Advance Notice introduces a notable MA risk-adjustment change by proposing that diagnoses from unlinked chart review records (CCRs) – that is, diagnosis submissions not tied to a specific beneficiary encounter – would no longer count toward risk score calculation. The -1.53-percent Sources of Diagnoses line reflects the proposed value of this new policy. CMS makes clear that MA organizations could still submit unlinked CRRs, but those submissions would not be used for risk scores. That makes this one of the most clearly policy-driven entries in the table, because it directly addresses the evidentiary basis CMS is willing to use for payment and therefore sits at the center of ongoing debates about coding intensity, documentation standards, and payment accuracy in MA rather than simply reflecting underlying medical-cost growth.

An Important Caveat: the Usual Advance Notice Table Excludes the Underlying Coding Trend

Perhaps the single most important interpretive point is in CMS’ footnote to the total. CMS states that the 0.09-percent expected average change does not include the underlying coding trend in MA. For CY 2027, CMS expects MA risk scores to increase by 2.45 percent on average due to the underlying coding trend, and CMS separately notes that the expected average change in payments is 2.54 percent when the estimated risk score trend driven by coding practices and population changes is considered.

The Resultant Rate May Still Be Low

Even though CMS says the expected average payment change rises from 0.09 percent to 2.54 percent once the estimated MA risk score trend from coding practices and population changes is included, that larger figure may still fall short of what some plans need in the current MA environment because it is not purely a benchmark increase and does not necessarily translate into a true representation of expected costs evenly across plans or counties. CMS’ fact sheet makes clear that the 2.54-percent figure reflects underlying risk-score growth (CMS estimates 2.45-percent coding trend), while the proposed payment stack still includes sizable downward offsets tied to risk model/normalization and diagnosis-source policy. At the same time, insurers have reported persistently elevated utilization and cost pressure in MA, and major carriers have been shrinking offerings or exiting counties in response to higher medical spending and reimbursement strain.

What Comes Next in the 2027 MA Rate Cycle

The next phase of the 2027 MA rate cycle is the compressed but consequential period between the Advance Notice and the final Rate Announcement, which must be published by April 6, 2026. The main takeaway is that the current notice should still be read as provisional. Important factors are still in flux, including the rebasing/re-pricing line, which remains pending finalization of the average geographic adjustment index. In other words, the broad direction of policy is visible, but the final distribution of payment effects is not yet locked in. Several important components are either interacting heavily (especially risk model revision and normalization) or not yet finalized (most notably rebasing/re-pricing, which is still listed as TBD pending finalization of the average geographic adjustment index).

Before final rates are released, the most important policy question is not simply whether the national percentage moves up or down, but where and how CMS’ methodology changes are likely to land. CMS is updating the county benchmark foundation by refreshing the FFS data window and repricing historical claims to current payment rules, while also incorporating policy adjustments that affect how local costs are represented in the rate book (including provider payment-related updates and targeted corrections for unusual billing patterns). CMS then applies additional benchmark adjustments after the geographic index is calculated – including statutory carve-outs and credibility adjustments for smaller counties – so the final impact can vary meaningfully across markets even when the national summary looks modest.

That is why the final stage of review is less about debating the headline number in isolation and more about evaluating how CMS’ policy choices will translate into market-level effects. The central questions include whether the final benchmark methodology supports plan stability across counties, how strongly the payment-calibration changes affect plan revenues and benefits, and whether CMS’ emphasis on payment accuracy and program integrity can be implemented without increasing disruption in already fragile markets. By the time CMS publishes the final Rate Announcement, the technical values will be set – but the larger policy significance will be how those values shape bidding behavior, benefit design, and participation decisions heading into 2027.

Conclusion

The CY 2027 MA payment table is an important rate signal for the future of the Medicare Advantage program, although it doesn’t tell the full story about the bottom line, expected average growth rate. The fact sheet’s 0.09-percent expected average change is the net of benchmark growth, quality-payment effects, risk-model and normalization changes, and diagnosis-source policy – and CMS separately notes that the displayed total does not include underlying MA coding trend, while the expected average payment change rises to 2.54 percent when coding practices and population changes are considered. That is why the component-by-component breakdown matters: it shows where CMS is recognizing underlying Medicare cost growth, where it is refining quality incentives, and where it is tightening payment calibration and documentation standards to improve payment accuracy in MA.