Insight

June 30, 2020

Has the Trump Administration Reached ‘Peak Deregulation’?

Executive Summary

- The Trump Administration released its Spring 2020 Unified Agenda of Regulatory and Deregulatory Actions, which shows the number of significant deregulatory actions dropping below the number of significant regulatory actions for the first time.

- This drop in planned deregulatory actions could be a sign that the administration is no longer pursuing deregulation with the same intensity as it did earlier.

- It could also be a sign, however, that the administration enacted the easiest deregulatory actions earlier and is running out of obvious deregulatory measures it can enact.

Analysis

It is no secret that the Trump Administration has emphasized deregulation as the hallmark of its regulatory policy. Indeed, the final accounting for three consecutive regulatory budgets shows it achieved net regulatory savings among executive agencies.

New data released by the Office of Information and Regulatory Affairs (OIRA), however, shows that the administration may have already reached its deregulatory apex, at least in terms of the number of significant deregulatory actions in the pipeline.

The latest version of the semiannual Unified Agenda of Regulatory and Deregulatory Actions, technically the Spring 2020 edition, was released on June 30. It contains nearly 2,700 “active actions,” or rulemakings expected to be worked on over the next year.

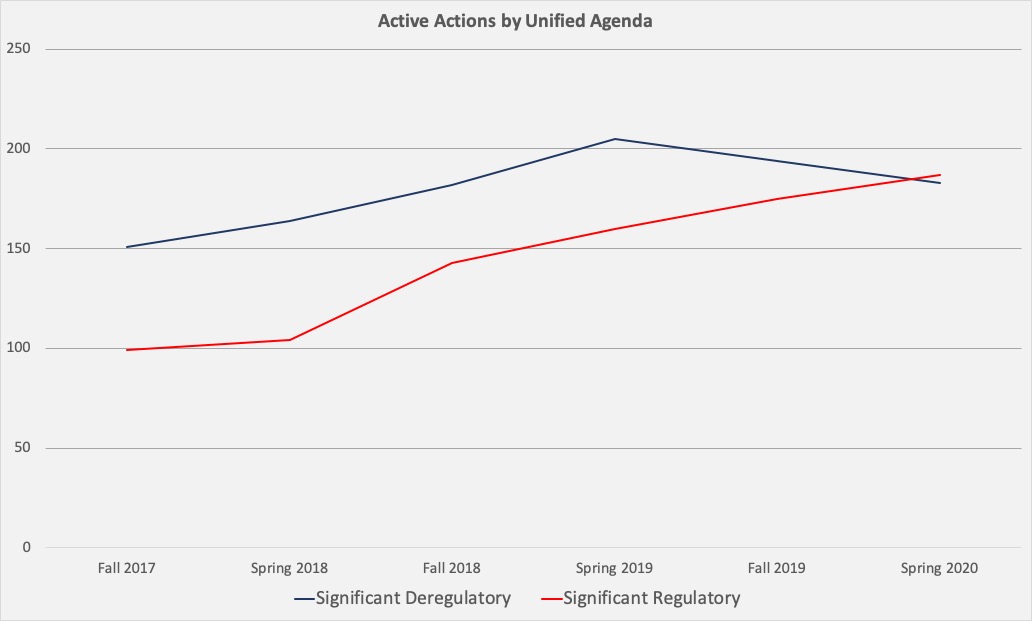

What jumps out in the data is that the number of active actions that are tagged as both “significant” (those with economic impacts of at least $100 million annually or raise novel policy issues) and “deregulatory” (those with net savings) are outnumbered by those tagged as both significant and “regulatory” (those with net costs). Looking historically since OIRA began tagging actions as deregulatory or regulatory in the Fall 2017 edition, this Unified Agenda marks the first time that has occurred.

Comparing counts of significant deregulatory actions and significant regulatory actions over those last six agendas, the Trump Administration appears to have hit its peak of deregulatory actions with the Spring 2019 edition. The chart below shows the number of each significant action since OIRA began tracking.

While the number of significant deregulatory actions has declined since its apex in the Spring 2019 agenda, significant regulatory actions have increased with each edition. One possible explanation for this difference is that the administration has continually completed more significant deregulatory actions than significant regulatory ones. The administration has completed 193 significant deregulatory actions versus 105 significant regulatory actions cumulatively, based on the data in each edition.

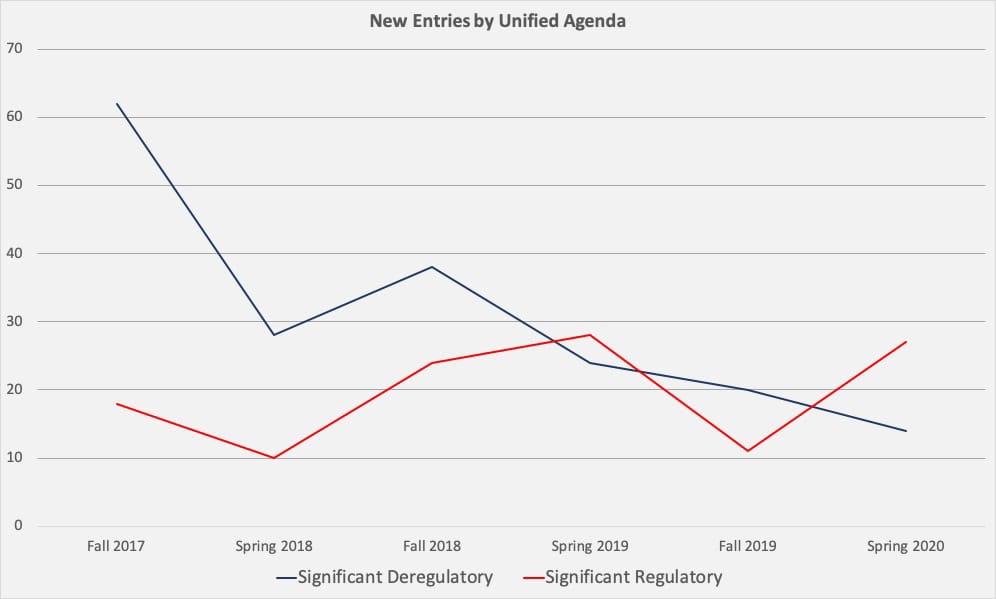

Others will point out, however, that the continued rise in the number of significant regulatory actions is evidence that the Trump Administration is losing its deregulatory bona fides. That view may have some merit. Looking only at the new significant entries in each edition, or those appearing for the first time, regulatory actions are outpacing deregulatory actions.

Looking beyond the raw counts of the Unified Agenda and returning focus to the fiscal year (FY) 2020 regulatory budget similarly shows two ways of looking at the issue. As of last week, the Trump Administration had finalized $170 billion in net savings so far in FY 2020, more than tripling the cumulative savings of the three prior FYs combined. All of that sum comes from the size of the Safer, Affordable Fuel-Efficient Vehicles Rule, which accounted for $199.5 billion in savings. Remove that rule, and the administration’s executive agencies would be net regulatory by nearly $30 billion.

The truth likely lies somewhere in between. The Trump Administration clearly had a number of deregulatory actions in mind early in its first term and has completed many of those. They have, therefore, picked the low-hanging fruit, and finding additional candidates for cutting red tape is proving more difficult. There is no denying, however, the rise of significant regulatory activity as the administration progresses.