Insight

June 23, 2026

Mega-merger Proposed to Power Data Center Alley

Executive Summary

- On May 18, NextEra Energy agreed to acquire Dominion Energy in a roughly $67-billion deal, poised to create the world’s largest regulated electric utility by market capitalization.

- The agreement comes amid an unprecedented surge in power demand from artificial intelligence data centers, accelerating the need to modernize existing grid infrastructure and scale new generating capacity.

- The merging parties will need to navigate myriad state and federal regulators that will likely scrutinize the merged firm’s ability to exercise market power in wholesale markets and could condition final approval on the divestiture of select generating assets.

Introduction

On May 18, NextEra Energy agreed to acquire Dominion Energy in a roughly $67-billion deal that would create the world’s largest regulated electric utility by market capitalization.

The agreement comes amid an unprecedented surge in power demand from artificial intelligence (AI) data centers. To meet this demand, the industry faces an immediate need to modernize existing grid infrastructure and build new generating capacity.

The merging parties will need to navigate myriad state and federal regulators that will likely scrutinize the merged firm’s ability to exercise market power in wholesale markets and could condition final approval on the divestiture of select generating assets.

The Merging Firms

Dominion Energy

Dominion Energy is a regulated electric utility that services 3.6 million customers in Viriginia, North Carolina, and South Carolina, alongside regulated natural gas services to 500,000 customers in South Carolina. At the end of 2025, the firm’s portfolio included 30.7 gigawatts (GW) of electric generating capacity, 10,800 miles of electric transmission lines, and 80,400 miles of electric distribution lines. Dominion Energy also develops and operates regulated offshore wind and solar power assets and is the largest producer of carbon-free electricity in New England.

Dominion’s presence in Virginia has positioned the firm as the primary energy provider to the AI data center industry. With Ashburn, Virginia at the epicenter – home to 133 of the state’s 609 data centers – Northern Virginia’s Loudoun and Fairfax counties host the largest concentration of AI data centers globally, earning the region the nickname “Data Center Alley.” According to Dominion, 28 percent of electricity sales through its wholly owned subsidiary, Virginia Power, directly service data centers. The company has connected an average of 15 data centers annually since 2013.

NextEra Energy

NextEra Energy is the largest electric power and energy infrastructure company in North America. It owns Florida Power & Light Company – the United States’ largest electric utility – which supplies power to approximately 12 million people across Florida. At the end of 2025, NextEra Energy had approximately 80 GW of net generation and storage capacity, using a mix of natural gas, wind, solar, and nuclear generation facilities, and battery storage facilities.

NextEra Energy also owns NextEra Energy Resources (NEER) – one of the largest energy infrastructure development companies – comprised of competitive energy and regulated transmission businesses. NEER owns, develops, constructs, manages, and operates generation facilities in wholesale energy markets in the United States and Canada as well as rate-regulated electric transmission assets throughout North America

NextEra Energy Transmission (NEET) is another subsidiary of NextEra Energy that owns, develops, finances, constructs, operates, and maintains transmission assets across North America.

Electricity Markets

Electricity markets are a mix of regulated and deregulated retail and wholesale markets. Apart from a nuclear power plant located in Connecticut, Dominion is a vertically integrated utility. This means it operates in every stage of the electricity supply chain – from generation to transmission and distribution – and functions as a regional monopoly under the oversight of state public utility commissions. These regulatory commissions set retail electricity prices based on operating and investment cost recovery plus a designated rate of return to fund future infrastructure.

Dominion Energy is also a member of PJM Interconnection, a deregulated Regional Transmission Organization (RTO). PJM operates energy, capacity, and ancillary service markets to determine wholesale electricity prices, serving 65 million people across 13 states and the District of Columbia.

While NextEra’s Florida Power and Light operates similarly as a vertically integrated, regulated utility, its service area lacks an RTO. Conversely, its NEER division operates entirely within competitive wholesale markets using long-term power purchase agreements. Under these agreements, buyers – typically utilities, corporations, or industrial facilities – purchase all of the electrical output from a specific infrastructure project at a pre-negotiated price.

According to Resources for the Future, a nonprofit, environmental, energy, and natural resources research organization, wholesale electricity markets are split into three distinct auction types:

Energy Markets

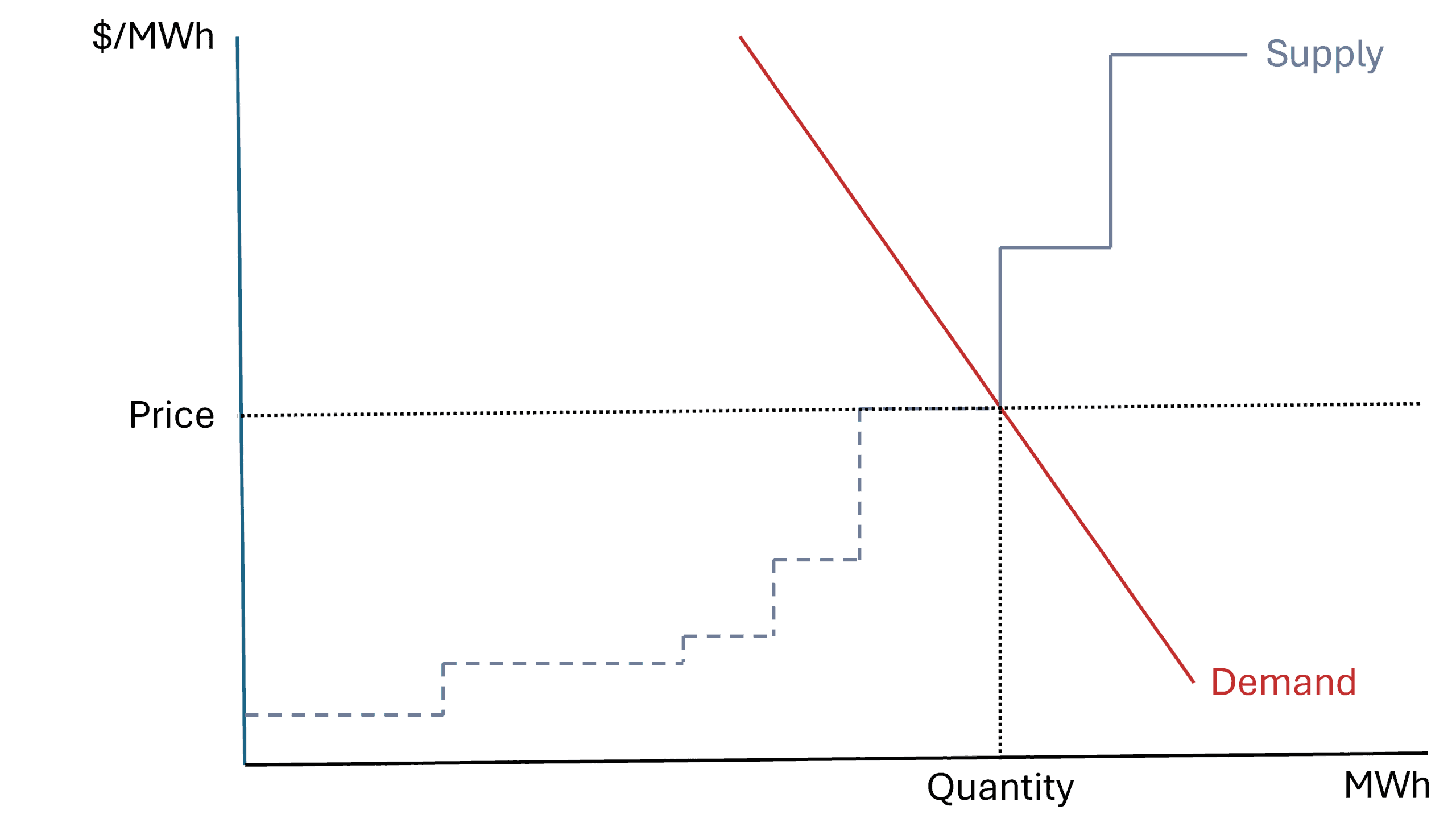

Energy markets are auctions that coordinate real-time and near-term electricity production. RTOs operate both day-ahead markets based on anticipated demand, and real-time markets that adjust for changes in demand. As shown in Figure 1, suppliers offer to sell a specific quantity of electricity while distributors bid for that electricity to meet demand. The market-clearing price, which is when the quantity of electricity supplied equals the quantity demanded, is received by the generators. The sell-side price for electricity is largely determined by the fuel source, with renewables typically demanding the lowest price. The RTO will then dispatch the power sequentially from least to most expensive.

Capacity Markets

The North American Electric Reliability Corporation – an independent organization that oversees and regulates the reliability of the power grid – requires energy retailers to support enough generating capacity to meet forecasted load plus a reserve margin to maintain grid reliability. Many RTOs run capacity auctions, so retailers secure their capacity requirements while enabling generators to recover fixed costs that are not covered in energy markets.

In these auctions, generators set a bid price at an amount equal to the cost of keeping a plant operational if needed. Similar to the energy market auction, the bids are arranged from lowest to highest. Once supply meets demand, all generators receive the same market clearing price, which is the price of the final, marginal generator to meet demand.

Ancillary Services

RTOs use ancillary services markets to cover everything outside capacity and energy markets. These services typically include operations that maintain grid frequency and short-term backup power.

The Merger and Regulatory Hurdles

Combining Dominion Energy and NextEra Energy would create the world’s largest regulated electric utility business by market capitalization and one of the world’s largest energy infrastructure companies. While the firms expect the deal to close in 12–18 months, the deal will require a multi-jurisdictional regulatory review and need the approval of:

- The Federal Energy Regulatory Commission (FERC)

- The Nuclear Regulatory Commission

- The Virginia State Corporation Commission

- The North Carolina Utilities Commission

- The Public Service Commission of South Carolina

The firms also notified the Federal Trade Commission and Department of Justice (DOJ) as required under the Hart-Scott-Rodino Antitrust Improvements Act, which has a mandatory 30-day waiting period before a deal can close.

While the legal mandate varies across each state and federal regulator, the focus will be the merger’s effects on competition and consumers.

A horizontal merger – which is the consolidation of companies operating in the same industry at the same stage in the supply chain – of this magnitude typically triggers antitrust scrutiny. Yet the utility operations of Dominion and NextEra span different geographies as separate regulated monopolies. In other words, the firms do not directly compete in the retail power market.

The primary concern of regulators will likely be the wholesale market in the PJM Interconnection Region. The merger between Exelon-Constellation – which closed in March 2012 – can serve as a guide to how regulators, specifically those at the federal level, will evaluate the merger. In the Exelon-Constellation merger, the DOJ alleged that the merged firm would gain control of 28 percent and 22 percent of the generating capacity in the PJM Mid-Atlantic North and Mid-Atlantic South regions, respectively. At this level of capacity, the DOJ claimed that the firm would have the “ability and incentive” to increase its share of “higher-cost capacity” in those markets.

By increasing its share of higher-cost capacity, the firm could “reduce output and raise clearing prices by withholding capacity.” According to the DOJ, the firm could submit “high offers in the PJM auctions for some of the capacity from its higher-cost units such that they are not called on to produce electricity,” forcing PJM to use more expensive sources of electricity to meet demand and resulting in a higher market-clearing price. To restore competition, the DOJ required the merged firm to divest three generating plants to restore competition rather than blocking the deal entirely.

But how does a firm exercise its market power by withholding capacity? Suppose two firms, each with 10 percent of generating capacity in the PJM region, merge. The combined firm will have 20 percent of the region’s total capacity. This capacity will be a mix of inexpensive fuel sources of electricity such as nuclear, solar, wind, and natural gas, and more expensive fuel sources. Because all generators are paid the market-clearing price – which is the most expensive source required to meet demand – there is an incentive to withhold capacity or bid a price to supply electricity that is so high it will not be called upon by PJM. With some of the supply withheld or priced above competitors, PJM will be forced to use more expensive electricity from the merged firm’s competitors, raising the market-clearing price. The merged firm, however, will receive the higher market-clearing price for all the electricity supplied from its cheaper fuel source. Even though it may lose money on the power it withheld or bid too high, it still may be profitable.

It is likely that FERC and the other regulators evaluating the merger will look for specific areas in the PJM region where it may be profitable for a merged Dominion and NextEra to execute this strategy. Like Exelon-Constellation, rather than seeking to block the deal entirely, regulators may require specific generating asset divestitures.

The AI Twist

The build-out of AI data centers has sent electricity demand soaring and is changing the dynamics of utilities. The 24/7 energy demand from data centers has put pressure on utilities to ensure supply is available. According to the Energy Information Administration (EIA), electricity consumption was flat for nearly 15 years, but demand has increased an average of 2.1 percent per year over the last five years. In EIA’s high electricity demand scenario, data center server energy use by 2050 will be more than 16 times that in 2020, 84-percent higher than its baseline case.

The expected increased electricity demand from the data center build-out will require a similar investment in grid infrastructure. Fusing NextEra’s renewable energy development business with the regulated utility model of Dominion could offer a blueprint for how the rest of the industry can bring capacity to the grid.

Conclusion

The electricity industry faces a pivotal moment as it tries to navigate the surging demand from AI infrastructure. The merger between NextEra and Dominion could offer a blueprint for how the industry can bring new capacity to the grid while maintaining reliability.

Regulators need to be mindful of this industry transition as it evaluates the merger’s effect on competition and consumers.