Insight

August 10, 2022

The Inflation Reduction Act’s Health Care Provisions

Executive Summary

The Senate-passed Inflation Reduction Act (IRA) included several health care provisions that will:

- Extend American Rescue Plan Act subsidies for the Affordable Care Act exchanges for another three years.

- Fundamentally shift how Medicare pays for drugs with price setting for Parts B and D, inflation penalties for Parts B and D, and out-of-pocket cost caps on insulin.

- Alter Medicare Part D’s structure to cap out-of-pocket costs for beneficiaries and expand eligibility for Low-Income Subsidies in Medicare Part D.

- Repeal the Trump Administration’s 2019 Prescription Drug Rebate Rule.

Introduction

On Saturday, the Senate passed the Inflation Reduction Act (IRA), the latest take on Democrats’ previous spending package known as Build Back Better, via reconciliation by a vote of 51-50. Along with climate and tax provisions, the IRA included several health care provisions that will:

- Extend American Rescue Plan Act (ARPA) subsidies for the Affordable Care Act (ACA) exchanges for another three years.

- Fundamentally shift how Medicare pays for drugs with price setting for Parts B and D, inflation penalties for Parts B and D, and out-of-pocket cost caps on insulin.

- Alter Medicare Part D’s structure to cap out-of-pocket costs for beneficiaries and expands eligibility for Low-Income Subsidies (LIS) in Medicare Part D.

- Repeal the Trump Administration’s 2019 Prescription Drug Rebate Rule.

The IRA makes significant changes to the U.S. health care system that will have impacts for years to come. Below is a brief explanation of the legislation’s key provisions.

Affordable Care Act Premium Tax Credits

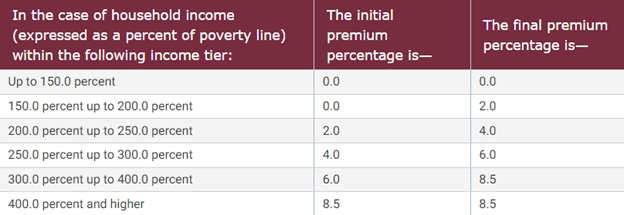

Passed as part of ARPA, the ACA premium tax credits will now be extended for another three years, through 2025. These premium tax credits will ensure that beneficiaries getting their insurance coverage through the marketplace exchanges will receive subsidies so that a second-lowest cost Silver plan will cost the individual no more than 8.5 percent of household income. While the initial premium tax credits for the ACA were lower than in ARPA and were not provided to individuals making 400 percent of the federal poverty level (FPL), ARPA increased the amount of the subsidy and expanded the number of individuals eligible to receive it. Figure 1 below illustrates the subsidy amounts for a given percentage of the FPL.

Figure 1. Table of Premium Tax Credits

Source: The Legal Information Institute at Cornell Law School

Medicare Drug Pricing Requirements

The IRA also includes language that will require Medicare to set prices for select drugs, a process the legislation calls “negotiation.” Drugs will be initially selected in 2023 and the prices set will be applied beginning in 2026. Drugs must be selected by the Centers for Medicare and Medicaid Services (CMS) and an agreement reached with the manufacturer two years before the new price will apply. Drugs eligible for selection are defined as those among the 50 single-source drugs with the highest total expenditures in either Part B or Part D and are at least seven years past their Food and Drug Administration approval date, with the initial price applicability year (IPAY) for certain small biotech drugs delayed until 2029. Specifically, CMS is directed to select 10 eligible Part D drugs for IPAY 2026; for IPAY 2027, CMS must select 15 eligible Part D drugs; for IPAY 2028, CMS must select 15 eligible Part D and Part B drugs; for IPAY 2029 and all subsequent years, CMS must select 20 eligible Part D and Part B drugs.

The IRA sets a “maximum fair price” (MFP) for all drugs selected that will based on a specified percentage. The specified percentages are as follows: For selected drugs that have been approved for less than 12 years (“short-monopoly drugs”), 75 percent of the non-federal average manufacturer price (AMP); for drugs approved between 12–16 years prior to being selected (“extended monopoly drugs”), 65 percent of AMP; and for drugs that have been approved for 16 or more years (“long-monopoly drugs”), 40 percent of AMP.

For IPAY 2026, the MFP will be set to the specified percentage of the average non-federal AMP for the selected drug in 2021 increased by the percentage increase of the consumer price index for all urban consumers (CPI-U). For IPAY 2027 and beyond, the MFP is required to be the lesser of the specified percentage of the 2021 non-federal AMP of the selected drug increased by the percentage increase of CPI-U, or the specified percentage of the average non-federal AMP for the selected drug the year prior to selection. Or, if it would result in a lower price, the MFP for Part B drugs is the price paid by Part B the year prior to being selected, and for Part D drugs would be the average of the prices negotiated by Part D plans net all price concessions received by the plans.

Manufacturers that do not comply with the price-setting process, including not engaging in the process or agreeing to an MFP, will be charged an increasingly large excise tax the longer the manufacturer is in non-compliance. For the first 90 days, the excise tax for the selected drug not in compliance is 65 percent; for days 91–180, the excise tax is 75 percent; for days 181–270, the excise tax will be 85 percent; and for any days after, the excise tax will be 95 percent. Manufacturers who are found to have violated the terms of the agreement or who fail to offer the MFP to a Medicare beneficiary will face civil monetary penalties up to 10 times the difference between the MFP and the price charged. Manufacturers can only avoid these penalties by either complying with set prices or by pulling the drug entirely from Medicare coverage.

Inflation Penalty

Under the IRA, single-source Part B drugs and all Part D drugs excluding certain low-spend drugs will be subject to a penalty if the drug’s price increases faster than inflation. This penalty will take the form of a rebate to Medicare on all units sold in Parts B and D at an amount over the allowed price increase.

For Part B drugs, the rebate is calculated as the total number of units sold in Part B multiplied by the amount the Part B payment rate in the applicable quarter exceeds the inflation-adjusted benchmark Part B payment rate for the quarter. Part B drugs that are currently approved would have Q3 of 2021 as their benchmark quarter, while drugs approved after December 1, 2020, would have the third full quarter after their approval as a benchmark quarter.

For Part D drugs, the rebate will be the amount equaling the total number of units sold in Part D multiplied by the amount that the volume-weighted average annualized AMP for a given year exceeds the inflation-adjusted, volume-weighted average annualized AMP for the benchmark year. The benchmark year for currently approved Part D drugs is 2021. Part D drugs approved after October 1, 2021, will use the first calendar year following approval as their benchmark year.

Part D Benefit Redesign

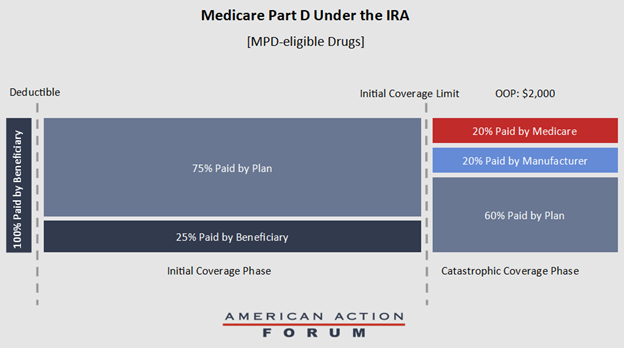

Beginning in 2025, Medicare Part D will undergo a substantial redesign with the introduction of a lowered out-of-pocket maximum for beneficiaries and the elimination of the coverage gap. Specifically, beneficiaries will not pay more than $2,000 out-of-pocket in a given year on Part D drugs in the initial coverage phase, after which the beneficiary will enter the catastrophic phase immediately and, starting in 2024, no longer be responsible for any cost sharing of their covered prescription drugs in the catastrophic phase.

The IRA establishes the Manufacturer Discount Program (MDP), which would require a 10 percent discount on the Part D negotiated price for a beneficiary in the initial coverage phase, and a 20 percent discount for beneficiaries in the catastrophic phase. Drugs eligible for this discount include all Part D drugs except those subject to the price-setting requirements mentioned above. If a beneficiary in the initial coverage phase is dispensed a drug subject to the price-setting requirements, Medicare must provide the plan with a subsidy equal to 10 percent of the drug’s MFP.

Medicare would reduce its reinsurance payments to 20 percent in the catastrophic phase for Part D drugs eligible for the MDP, and 40 percent for drugs not eligible for the MDP. These changes mean that, in the catastrophic phase, plan sponsors will be responsible for 60 percent of the costs, as opposed to the current level of 15 percent and, for MPD-eligible drugs, manufacturers will be responsible for 20 percent of the costs and Medicare will be responsible for the final 20 percent (See Figure 2).

Figure 2. Part D Benefit Under the IRA for MPD-eligible Drugs

The IRA also limits premium rate increases for Part D for the years 2024–2029 at 6 percent year-to-year. In 2030 and subsequent years, CMS will recalculate base premiums using the original Part D premium formula. The IRA will also repeal the Trump Administration’s 2019 Prescription Drug Rebate Rule. While the rule was continuously delayed and never implemented, the Congressional Budget Office stated the repeal will provide $122 billion in savings between 2022–2031 compared to the rebate rule being implemented. Additional changes to Part D include: Limiting copays for insulin to $35 a month for beneficiaries, allowing beneficiaries to choose to pay out-of-pocket costs on a monthly basis subject to a cap, known as “smoothing;” expanding LIS-eligible beneficiaries from those below 135 percent of the FPL to those below 150 percent of the FPL starting in 2024; and covering all vaccines recommended by the Advisory Committee on Immunization Practices with no cost sharing to beneficiaries.