Insight

March 19, 2026

U.S. LNG Exports Unlikely to Mitigate Global Supply Shock

Executive Summary

- In the wake of the current Middle East conflict, natural gas prices have spiked globally while remaining relatively stable in the United States; this price disparity is primarily due to the fragmentation of the global natural gas market.

- The United States is the leading global exporter of liquefied natural gas (LNG) and is at export capacity; further, export is logistically challenging, meaning it is difficult to scale those exports quickly.

- With conflict around the Strait of Hormuz causing an approximate 20-percent shortfall in the world natural gas market, this insight analyzes U.S. production and export capacity and concludes that the United States is unlikely to offset supply disruptions in the near future.

Introduction

Following the start of the ongoing Middle East conflict, natural gas prices are rising drastically in Europe and Asia, reaching as high as $19 per million British thermal units (MMBtu), while U.S. natural gas prices have been relatively flat at around $3 per MMBtu.

The United States is the world’s leading exporter of natural gas, selling 8.9 trillion cubic feet (Tcf) of natural gas to the rest of the world in 2025. Unlike the global oil market, however, the natural gas market is fragmented. Intercontinental natural gas trade requires a capital-intensive liquefied natural gas (LNG) value chain that includes specialized liquefaction at the source and regasification at the destination. This creates high barriers to market integration and leads to differential prices across regions.

With the effective closure of the Strait of Hormuz causing an approximate 20-percent shortfall in the world natural as market, this insight analyzes U.S. production and export capacity and concludes that the United States is unlikely to offset Persian Gulf supply disruptions given the fully utilized U.S. export capacity.

The Global LNG Market Is More Fragmented Than the Crude Oil Market

While the global crude oil market operates as a largely integrated system with minimal regional price variance, the natural gas market remains significantly more fragmented. This pricing divergence is primarily a function of the immense logistical challenges associated with long-distance gas transport.

Unlike oil, which is easily shipped in its natural state, intercontinental natural gas trade requires a capital-intensive LNG value chain that includes specialized liquefaction at the source and regasification at the destination. This creates high barriers to market integration and leads to differential prices across regions.

Disruptions in the Persian Gulf’s Energy Exports

Global trade in natural gas has become a focus of attention in the wake of joint U.S.-Israel military strikes on Iran beginning on February 28, 2026. Tehran retaliated against public and private infrastructure across nine Gulf nations, resulting in a de facto closure of the Strait of Hormuz. American Action Forum’s previous insight provides an overview of Iran’s oil and gas export capabilities, the strategic significance of the Iran-controlled Strait of Hormuz, and the potential impact on the global and U.S. energy markets.

Notably, about one-fifth of the world’s LNG consumption goes through the Strait— about 10.4 billion cubic feet per day (Bcf/d) in 2024, and 11.5 Bcf/d in the first quarter of 2025. Most of the LNG exports come from Qatar, which has announced a complete halt of some of its LNG production due to the military conflicts. Most of the LNG exports that transit the Strait of Hormuz are bound for Asian countries. The disrupted LNG supply has led to surging natural gas prices in both Asia and Europe.

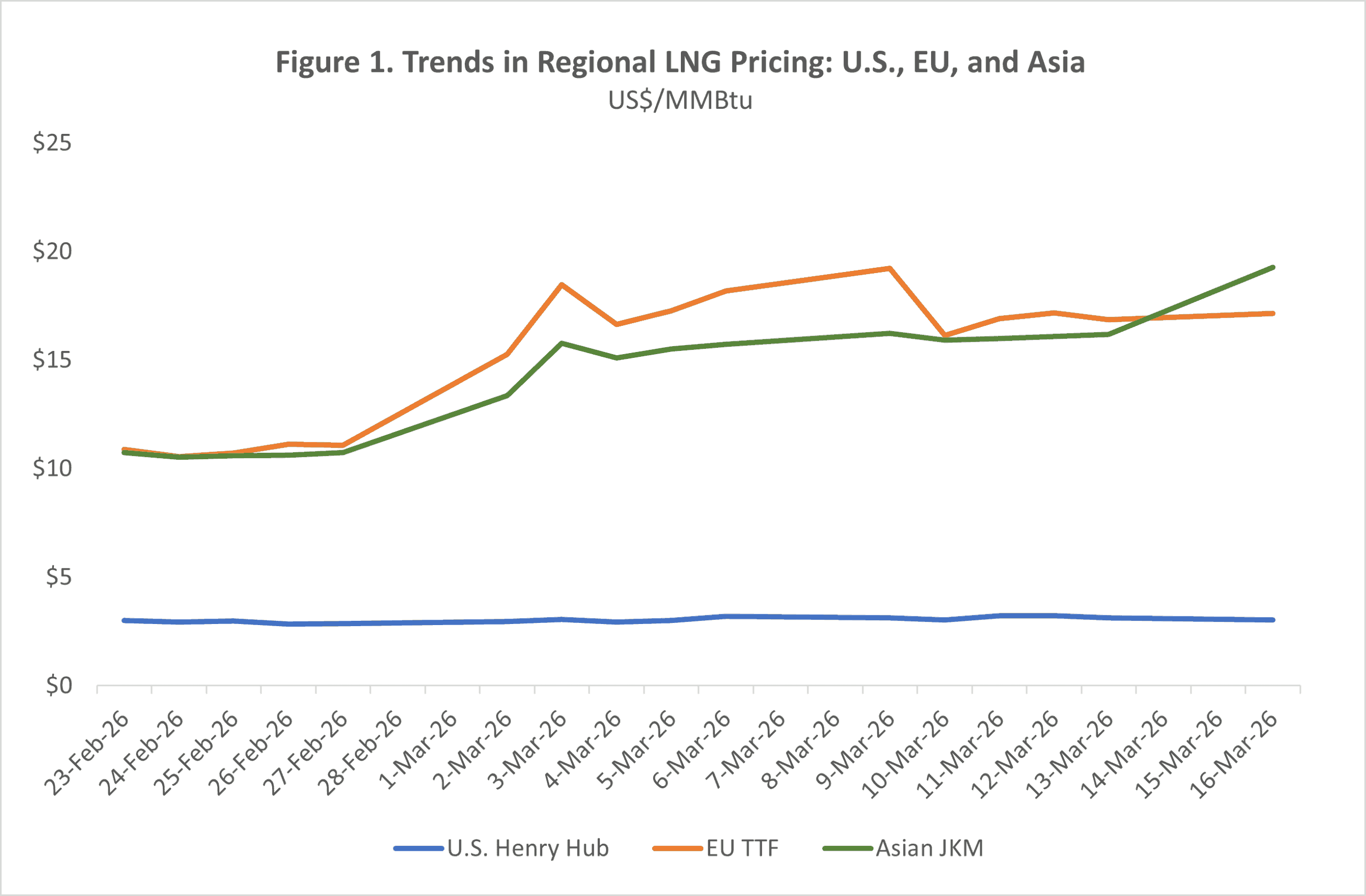

As shown in Figure 1, after the effective closure of the Strait of Hormuz, natural gas prices in the EU and Asia have spiked significantly, with the former rising by 62 percent and the latter increasing by 83 percent between February 23 and March 16. Yet the Henry Hub spot price—the primary U.S. natural gas price benchmark—has stayed relatively flat over the past two weeks. Robust domestic natural gas production has been insulating U.S. consumers from international price volatility.

Source: Business Insider, Investing.com, ICE.com, author’s analysis.

In the latest short-term energy outlook (March 2026), Energy Information Administration (EIA) expects that “U.S. natural gas prices to be relatively unaffected by [the closure of the Strait of Hormuz].” In fact, the EIA lowered its Henry Hub spot price forecast by 13 percent from last month, citing higher-than-anticipated natural gas storage following a mild February.

Additionally, EIA is projecting the spot prices to be about $3.9 per million British thermal units (MMBtu) in 2027, which is 12 percent lower than last month’s forecast. This reflects the expectation that rising oil prices will boost oil output, which will subsequently increase associated gas production (oil and natural gas are sometimes found in the same reservoir).

The United States Is the Leading Global LNG Producer and Exporter

The United States is the world’s largest natural gas producer. As shown in Figure 2, U.S. total dry production (consumer-grade energy) of natural gas surpassed its total consumption in 2017 and reached about 39.3 Tcf in 2025. In 2024, the United States consumed about 80 percent (30.8 Tcf) of its total dry gas production. Natural gas is mainly used for generating electricity in the United States, accounting for 42 percent of the electricity sector’s primary energy consumption.

Source: U.S. Energy Information Administration

America’s marketed natural gas production (raw gas extracted from wells) hit a record-high level of 118.5 billion cubic feet per day (Bcf/d) in 2025, driven by three main producing regions—Appalachia, Permian Basin, and Haynesville—accounting for 67 percent of total production.

As a leading global exporter, the United States exported about 20 percent (approximately 8.9 Tcf) of natural gas to the rest of the world in 2025.

U.S. LNG Export Capacity

An LNG export terminal includes liquefaction facilities used to liquefy natural gas, storage tanks, and infrastructures that load the LNG onto specially designed tankers for shipping.

The Federal Energy Regulatory Commission (FERC) is responsible for authorizing the siting and construction of onshore and near-shore LNG export facilities. The Department of Energy (DOE) grants permission for exports to jurisdictions with which the United States does not have free trade agreements.

According to FERC’s latest data as of March 10, 2026, there are currently eight operating LNG export terminals in the United States: Kenai (AK), Sabine Pass (LA), Cove Point (MD), Corpus Christi (TX), Hackberry (LA), Elba Island (GA), Freeport (TX), and Cameron Parish (LA). Most of them are on the coast of Louisiana and Texas (Figure 3).

Notably, U.S. LNG export terminals are currently operating at capacity—meaning that significant export growth is impossible without substantial export infrastructure expansion.

Source: Federal Energy Regulatory Commission

The existing terminals under FERC’s authority have a total capacity of 14.6 Bcf/d. FERC recently estimated that the United States will bring on a total of 35.04Bcf/d of LNG export capacity (23.7 Bcf/d under construction, 11.4 Bcf/d approved but not yet under construction) in the next few years.

Most U.S. LNG is exported via a “free on board (FOB)” pricing model, which means buyers pay for the LNG cargos at the export terminal without any adjustment for the ocean freight cost, insurance, or credit. LNG exports are typically sold on long-term contracts—about three quarters of them are for 20-year terms. A common feature of these agreements is destination flexibility—the buyer of the LNG cargo can ship them anywhere as long as it has the export authorizations from the DOE and follows U.S. law.

Since the Middle East conflict started, the destination flexibility of U.S. LNG has triggered intense competition between Asian and European buyers. This has led to competitive price bidding, with some cargoes diverted from their original European routes to Asian markets.

Looking Forward

While the United States has emerged as a leading LNG exporter with plans to expand export capacity, current infrastructure bottlenecks mean its ability to mitigate Persian Gulf disruptions in the immediate future is physically capped. Moving forward, the U.S. role in the world’s natural gas market will depend on whether long-term export capacity expansion aligns with the future global demand landscape.