Research

January 7, 2025

Competition in Air Transportation

Executive Summary

- On October 24, 2024, the Department of Justice and the Department of Transportation issued a request for information on competition in air transportation.

- Since the airline deregulatory era began in 1978, inflation-adjusted airfares have tumbled as increased competition resulted in more airlines competing for routes and innovative business models have been brought to the market.

- Efforts to revert to heavy regulation of the airline industry could limit choices available to consumers and lead to higher prices.

Introduction

On October 24, 2024, the Department of Justice (DOJ) and the Department of Transportation (DOT) issued a request for information (RFI) on competition in air transportation. The agencies were seeking information on consolidation, anticompetitive conduct, and anything else that impacts the availability and affordability of air travel.

The deregulatory era of the airline industry that began in 1978 unleashed a competitive market for airline travel. The competition for routes among airlines has intensified, new innovative business models have been brought to the market, and the inflation-adjusted cost of flying has fallen.

Efforts to reregulate the airlines could result in fewer choices and higher prices for consumers.

Airline Deregulation

In 1938, President Franklin Roosevelt signed the Civil Aeronautics Act (CAA) to act as the aviation industry’s economic and safety regulator. In 1940, the CAA was split into two agencies, the CAA and the Civil Aeronautics Board (CAB). The CAB was responsible, in part, for the economic regulations of the airlines, including how many airlines could fly a route and the fares charged by the airlines.

After decades of limited choice and expensive air travel, President Jimmy Carter signed the Airline Deregulation Act of 1978. The Airline Deregulation Act removed the CAB’s ability to fix prices and set routes in favor of a competitive market. The Reason Foundation provides a more comprehensive regulatory history of the airline industry.

Recent Regulatory Action

On July 9, 2021, President Joseph Biden signed the Executive Order on Promoting Competition in the American Economy (EO). The principal concern of the EO was market concentration, which the president asserted had become “excessive” and “threaten[ed] economic liberties, democratic accountability, and the welfare of workers, farmers, small businesses, startups, and consumers.” Since the signing of the EO, much of the federal antitrust enforcement agenda has focused on the further consolidation of markets. Past research by the American Action Forum refutes the assertion that markets have become more concentrated over time and demonstrates that market share is not the proper way to assess competition.

The DOJ recently has been involved in several enforcement actions against the airlines to limit consolidation in the industry. The agency successfully unwound the American Airlines and JetBlue Northeast Alliance and blocked the merger between JetBlue and Spirit Airlines. After the DOJ successfully blocked the JetBlue and Spirit merger, Spirit Airlines filed for bankruptcy.

Current Regulatory Barriers in Airline Competition

As is often the case, regulatory barriers inhibit the consumer benefits of intense competition. Excessive regulations often erect barriers to entry that benefit incumbent firms. Currently, the perimeter and slot rule in effect at Ronald Reagan Washington National Airport (DCA) restricts competition by protecting other D.C.-metro area airports. These protections have reduced competition among airlines, resulting in higher ticket prices, longer flight times, increased delays, and fewer choices for consumers. On October 16, 2024, the DOT tentatively awarded five new slots for routes outside DCA’s perimeter rule.

Current State of Airline Competition

Competition among airlines can be measured with several methods. The first method considered here is competition for city-pairs. Airlines shuttle customers from city to city, often serving multiple airports in large metropolitan areas. These routes are referred to as origin and destination city-pairs. Airlines compete intensely for these routes.

The second method is the business model. Historically, the airline industry was dominated by a few global network carriers (GNC), including United Airlines, Delta Air Lines, and American Airlines. The ticket price on these GNCs regularly includes, among other things, bags, meals and snacks, seat selection, and in-flight entertainment (WiFi, television screens, etc.). Ultra low-cost carriers (ULCC), by contrast, charge a price for the seat and ancillary fees for bags, in-flight drinks and snacks, and pre-selecting a seat. Low-cost carriers (LCC) are a middle ground between the GNC and the ULCC. Ticket prices for these airlines may include fees for baggage, drinks and snacks, pre-selected seats, and even in-flight entertainment.

Simply put, some airlines use an all-in pricing model where others unbundle their offerings to varying degrees.

Number of Competitors

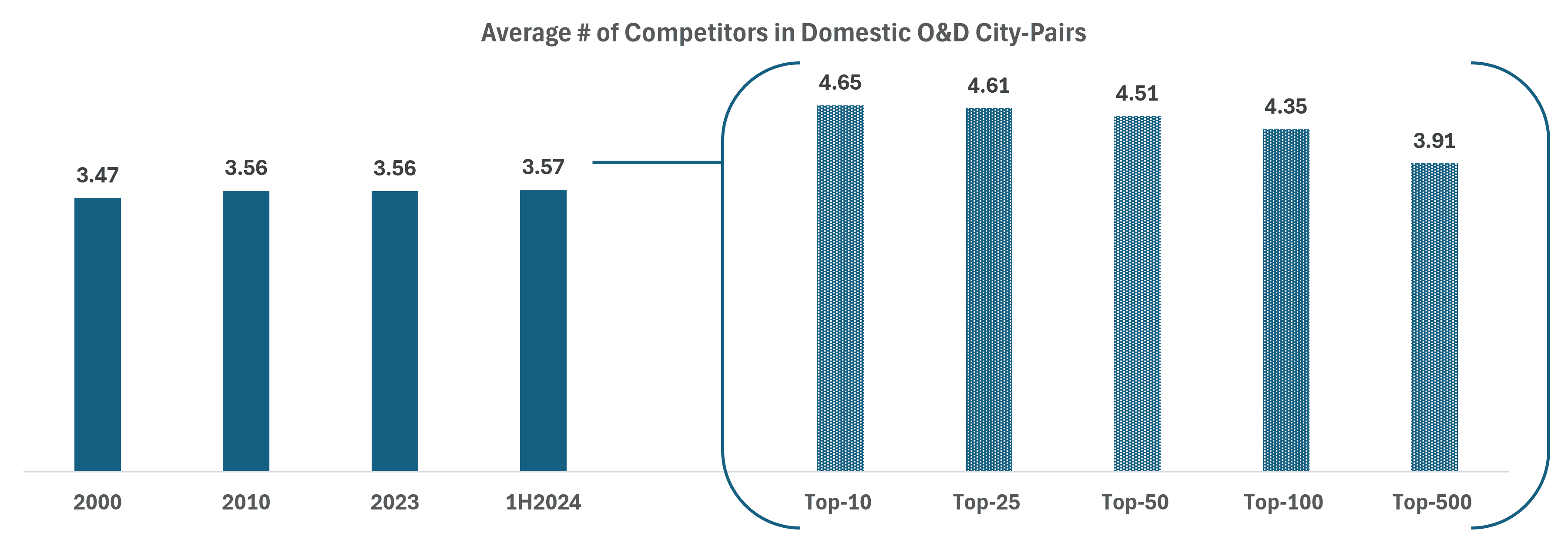

The late 1990s through the early 2010s brought a flurry of airline mergers and acquisitions, including mergers involving U.S. global network carriers United Airlines, American Airlines, and Delta Air Lines. While these mergers reduced the number of independently operating airlines, they did not reduce the level of competition in the industry. In fact, AAF research showed that the number of competitors with at least a 5 percent market share for each city-pair increased from 3.47 to 3.57 between 2000 and the first half of 2024. Moreover, the city-pairs serving the greatest number of passengers faced even more competition. The top 10 busiest city-pairs had an average of 4.65 competitors in the first half of 2024. A more detailed breakdown can be found in Figure 1.

Figure 1

*Data reflect the number of competitors with at least 5 percent market share for a city-pair; Bureau of Transportation Statistics DB1B Market Database

Competition of Business Models

Critical to understanding the level of competition in airlines is answering the question: Are all airlines the same? They are not. Airlines use varying business models to attract customers. These different business models are a form of competition. Some airlines charge a ticket price that is all-inclusive of baggage fees, seat selection, drinks and snacks, and in-flight entertainment. Others unbundle these features to offer the lowest possible price for the seat and charge for additional amenities for which the customer is willing to pay. Other business models lie somewhere in between.

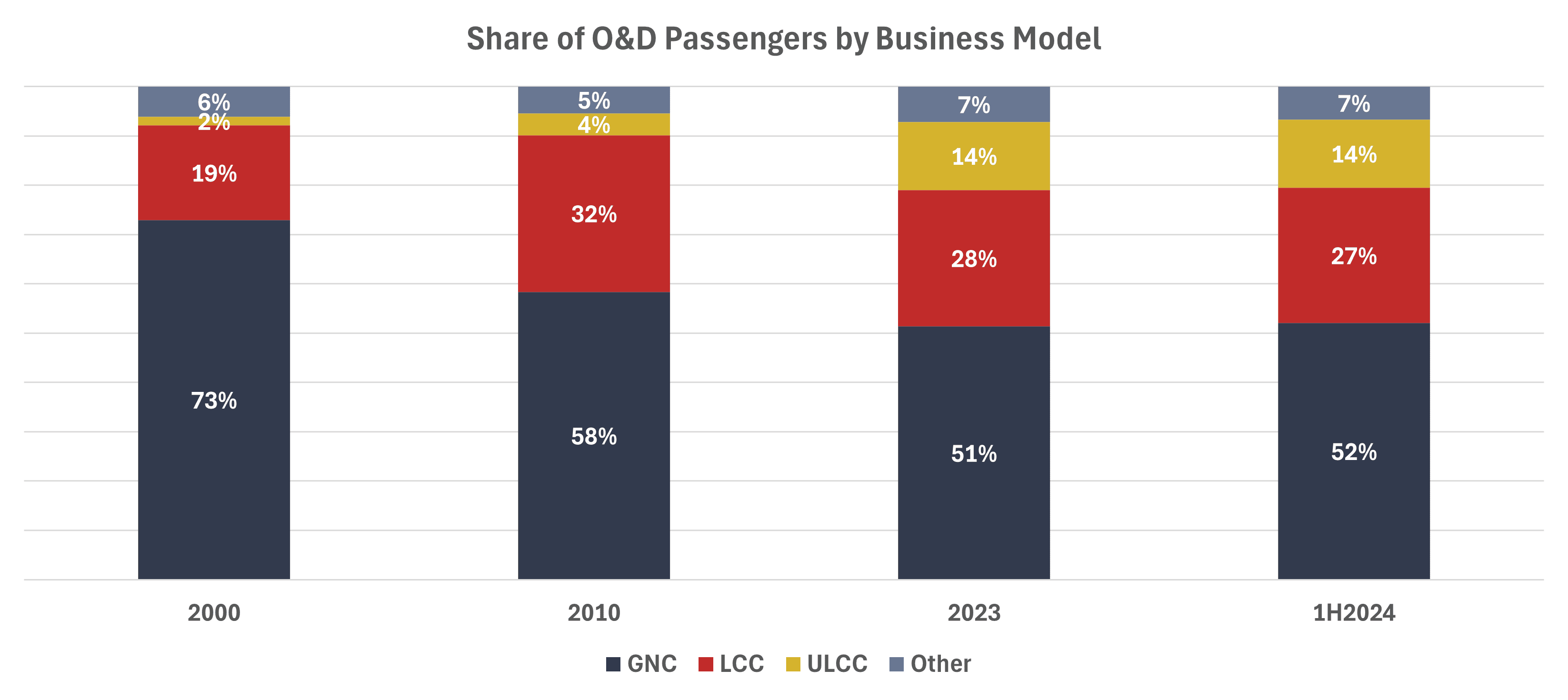

The rise of LCC and ULCC carriers in the early 2000s put pressure on the existing business models of the GNCs. To survive, many GNCs merged. Yet despite the consolidation, the share of passengers across city-pairs served by the GNC business model declined from 73 percent in 2000 to 52 percent in the first half of 2024, as shown in Figure 2.

Figure 2

*Source: Bureau of Transportation Statistics DB1B Market Database

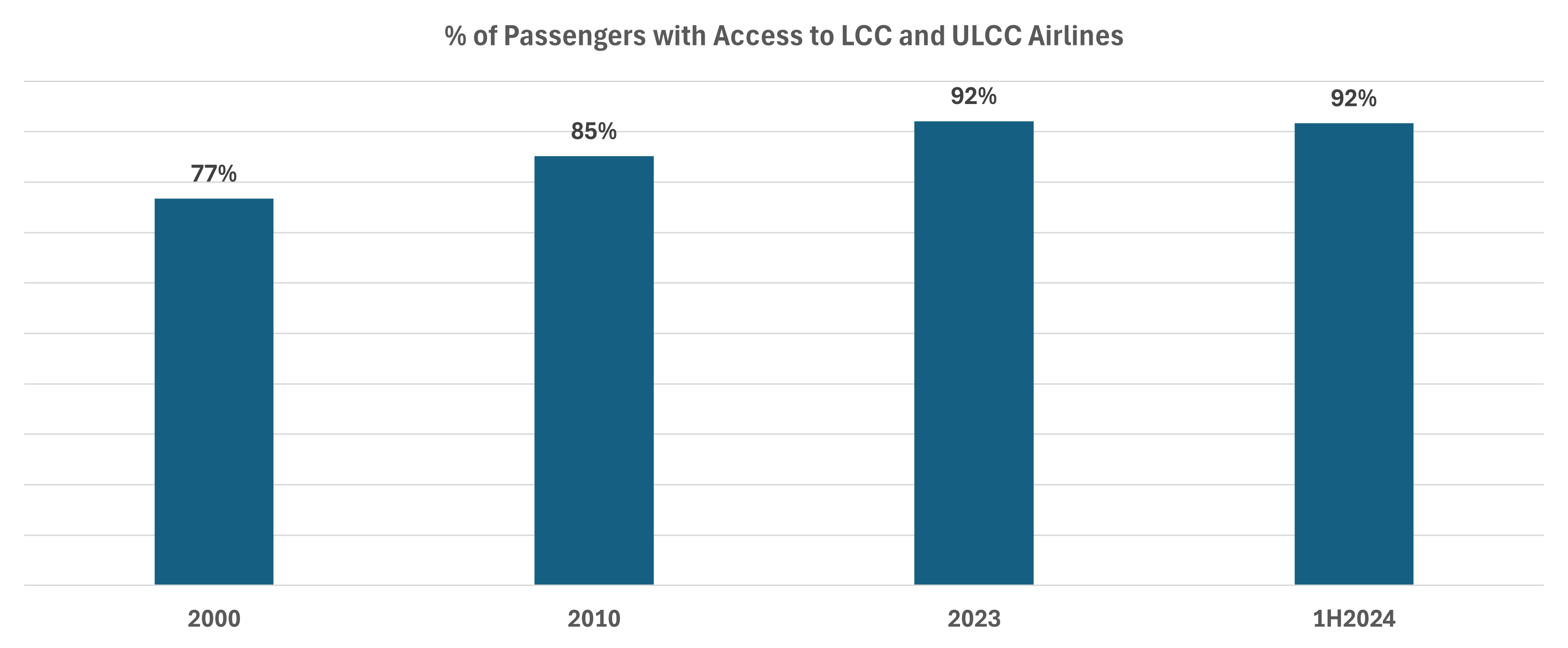

Furthermore, the number of passengers with access to LCC and ULCC business models has increased. As shown in Figure 3, just 77 percent of passengers had access to an LCC or ULCC in 2000. In the first half of 2024, that share increased to 92 percent.

Figure 3

*Source: Bureau of Transportation Statistics DB1B Market Database

GNC response to unbundled business model

The unbundled business model of the LCCs, ULCCs, and even some of the GNCs has received recent attention in Congress. A congressional report released on November 26, 2024, found that the “strategy of ‘unbundling’ ancillary products from the base price of a ticket was once largely limited to low-cost carriers, but airline revenue from ancillary fees has become an important source of revenue for airlines across the industry.” The report also found that GNCs introduced “Basic Economy” fares to compete with LCCs and provided an example in which Delta offered this unbundled option specifically on routes where it competed with ULCC Spirit Airlines. This response clearly shows that GNCs had to alter their business models to respond to the market demand for unbundled air travel.

Effects of Competition

Increased competition is often associated with lower prices, greater choice, and more innovation. Since the airline industry was deregulated and empowered to respond to the demands of the market, it has delivered on all these characteristics. As previously discussed, over time, increased competition resulted in newer business models that provided customers with new options for flying. Further, as shown in Figure 4, inflation-adjusted airline fares have tumbled 38 percent since Q1-1995 while the current dollar price has climbed 28.8 percent.

Figure 4

*Source: National-Level Domestic Average Fares Series, Department of Transportation

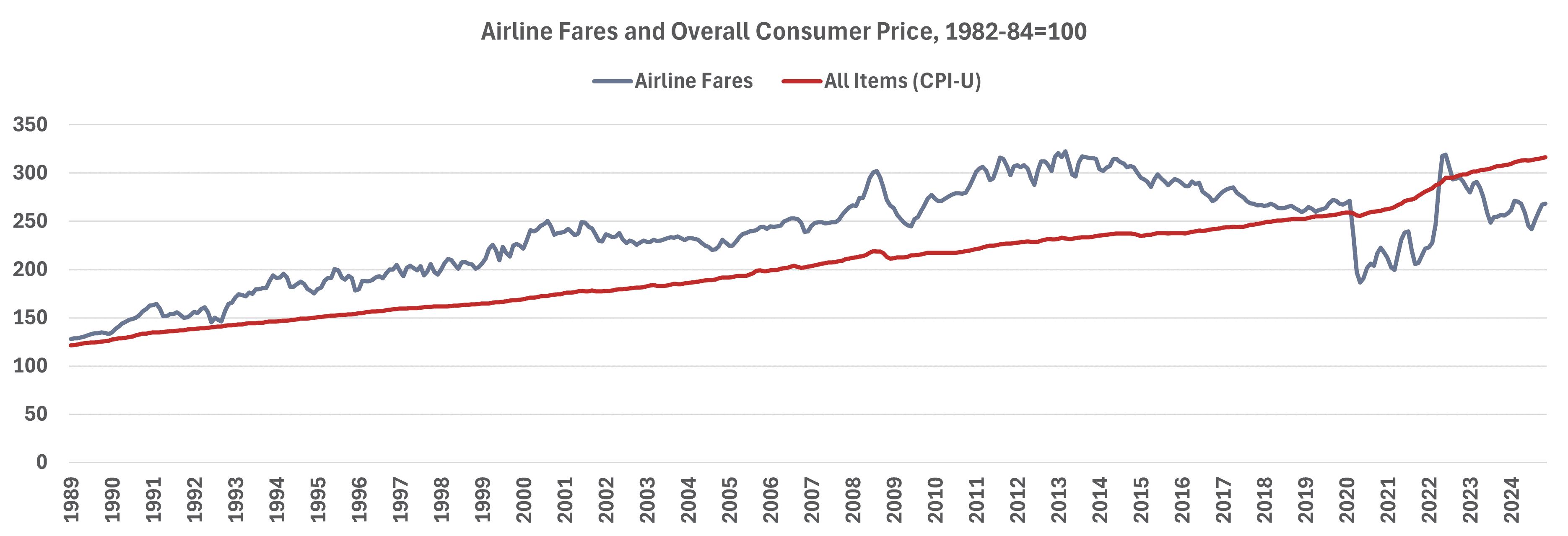

Moreover, airline fare inflation has grown at a slower pace than overall inflation. Since January 1989, airline fare inflation has increased 109 percent while overall consumer prices have grown 161 percent, as shown in Figure 5.

Figure 5

*Source: Bureau of Labor Statistics Consumer Price Index Data

Conclusion

The DOJ and DOT’s RFI was intended to better understand the competitive state of the airline industry and to study whether consolidation, anticompetitive conduct, or other business activities impact the availability and affordability of air travel. The data show that competition in the airline industry is strong and has intensified over the past two-and-a-half decades.

Efforts to reregulate the airline industry threaten to unravel the progress made through competitive markets, limiting consumer choices and increasing the cost of air travel.