Research

April 15, 2026

Tariff Exemptions: The Hollowing Out of Trump’s Trade Regime

Executive Summary

- Immediately following the Supreme Court’s decision to strike down President Trump’s International Emergency Economic Powers Act tariffs, the president issued across-the-board 10-percent tariffs under Section 122 of the Trade Act of 1974; yet as with the IEEPA tariffs, he exempted wide swaths of consumer-facing imports such as electronic and food products.

- This research compares tariff exemptions under IEEPA and Section 122, finding that the president exempted more than 60 percent of U.S. imports from Section 122 tariffs compared to 38 percent under IEEPA; this wider net of exemptions under Section 122 has lowered the overall U.S. tariff rate from around 14 percent to 10 percent.

- The Trump Administration’s increasingly broad tariff carveouts signal a retreat from hardline tariff rhetoric as consumer affordability concerns grow, meaning tariff costs may have reached their high-water mark in 2025.

Introduction

Immediately following the Supreme Court’s decision to strike down President Trump’s International Emergency Economic Powers Act (IEEPA) tariffs, the president issued across-the-board 10-percent tariffs using his authority under Section 122 of the Trade Act of 1974. As with IEEPA tariffs, the president exempted wide swaths of consumer-facing imports such as electronic and food products to ease concerns over rising prices. This research examines exemptions under IEEPA and Section 122 and finds that more than 60 percent of U.S. imports are exempt from Section 122 tariffs compared to 38 percent at the height of IEEPA exemptions. The wider net of exemptions under Section 122 has lowered the overall U.S. tariff rate from around 14 percent to 10 percent. The Trump Administration’s increasingly broad tariff carveouts signal a retreat from hardline tariff rhetoric as consumer affordability concerns grow, meaning tariff costs may have reached their high-water mark in 2025.

The Past: Exemptions During the IEEPA Regime

On “Liberation Day,” the Trump Administration implemented IEEPA tariffs ranging from 10–50 percent on all U.S. trade partners (read more here). This raised the effective U.S. tariff rate from around 3 percent to roughly 14 percent by the time the Supreme Court ruled against President Trump’s use of IEEPA authority. The administration supplemented the IEEPA regime using Section 232 of the Trade Expansion Act of 1962 to impose tariffs as high as 50 percent on various imports in the name of national security. While IEEPA tariffs have been struck down as of February, Section 232 tariffs remain in place.

From the onset of “Liberation Day,” more than 1,000 different imports were exempted from IEEPA including energy products, bullion, and minerals unavailable in the United States. Roughly 20 percent of total U.S. imports fell under general IEEPA exemptions. Products subject to Section 232 tariffs were also exempted, including pharmaceuticals, steel, aluminum, semiconductors, copper, and lumber. Throughout 2025, the administration expanded tariff exemptions to include other imports such as electronics, critical minerals, and agricultural products.

This research estimates that roughly 38 percent of U.S. imports were exempted in the wake of “Liberation Day.” This figure includes U.S. imports exempt from IEEPA but subject to a current or future Section 232 tariff. Excluding goods that fall under Section 232, close to 27 percent of imports faced neither a newly implemented Section 232 nor IEEPA tariffs (see Figure 1).

Figure 1: IEEPA Tariff Exemptions as a Percentage of U.S. Imports Since “Liberation Day”

| Exempt from IEEPA |

37.5% |

| Exempt from IEEPA, Not Subject to Section 232 |

27.3% |

Source: The White House, United States International Trade Commission (April 2–December 31, 2025)

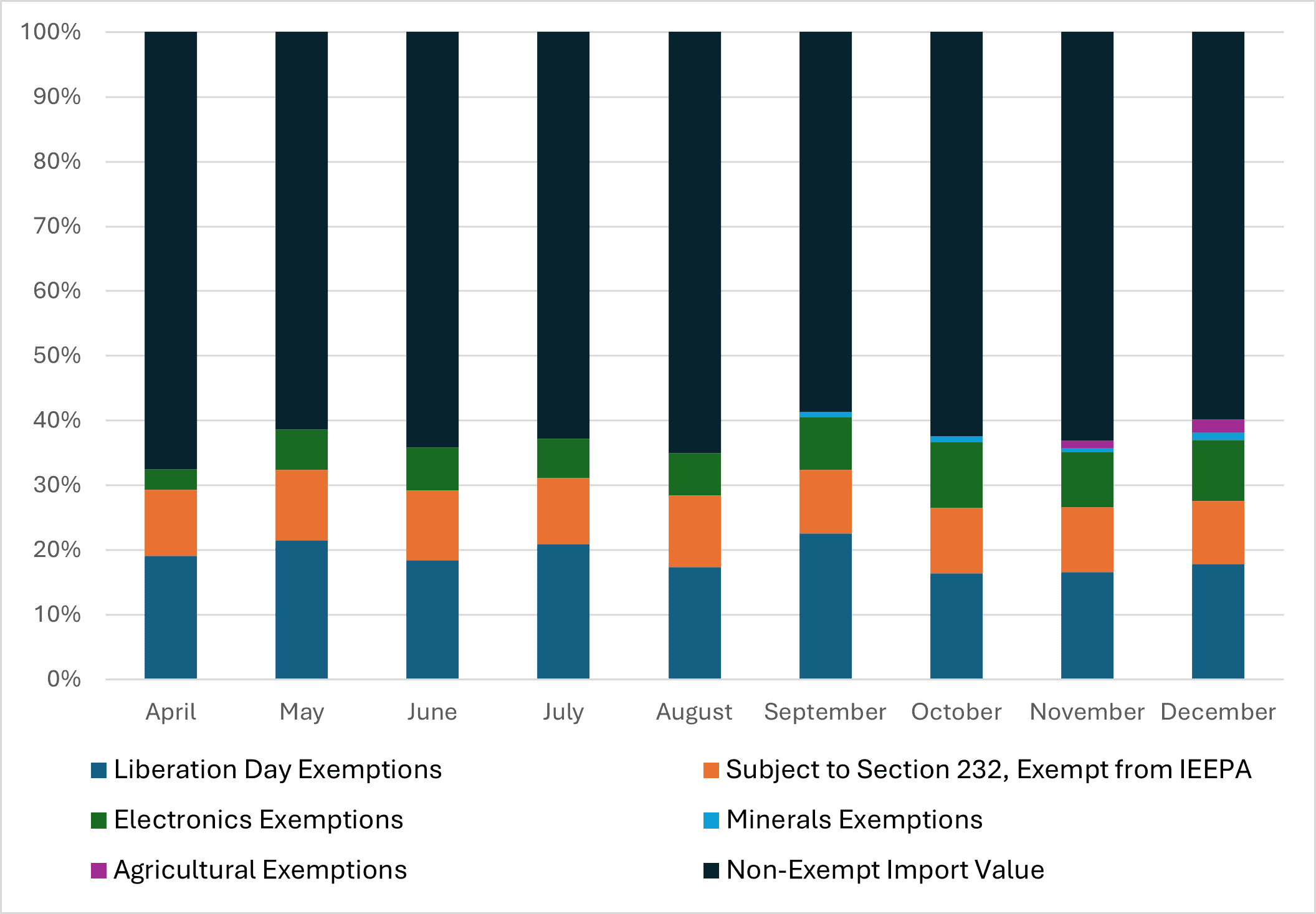

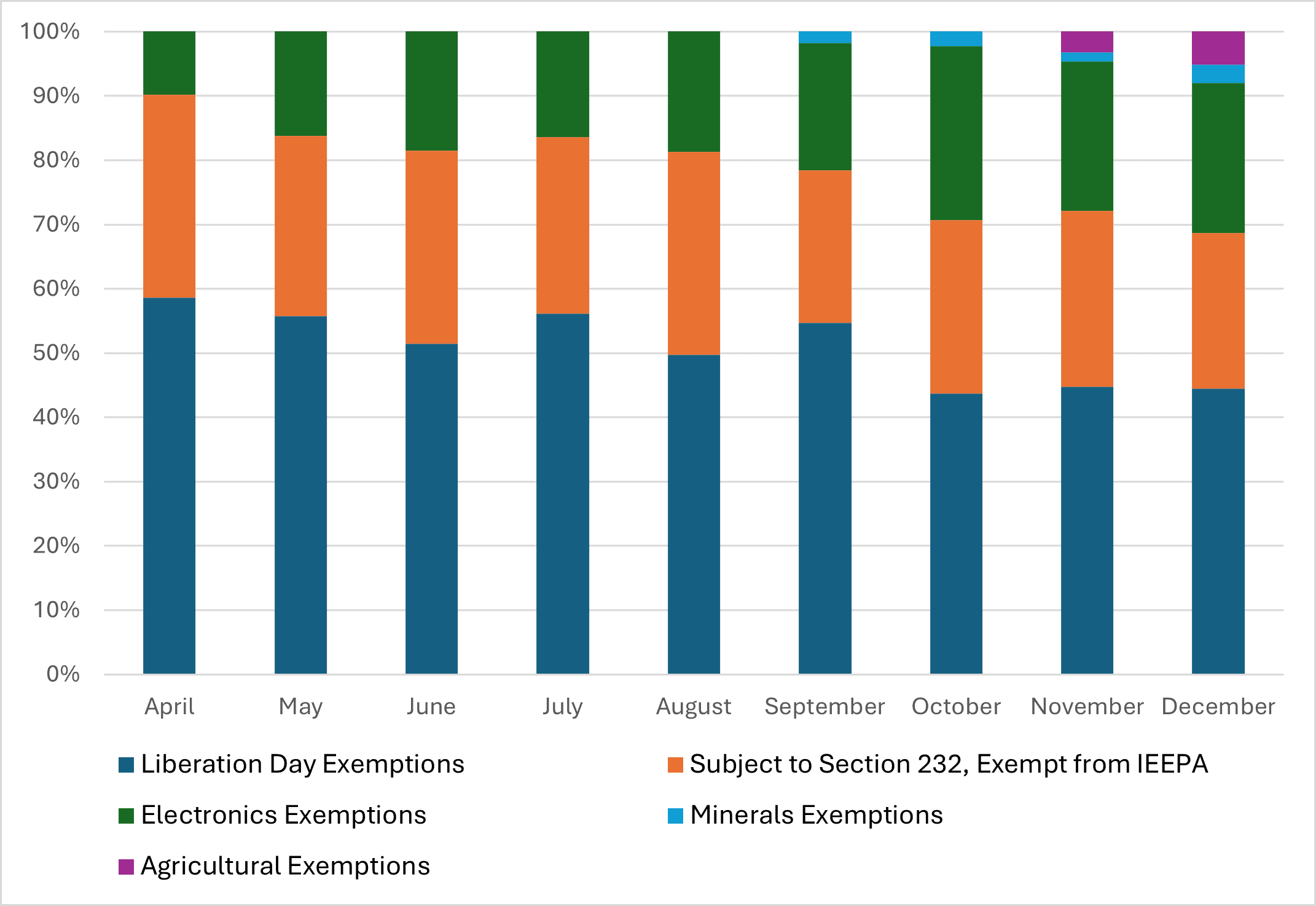

Figure 2 shows IEEPA tariff exemptions as a percent of total monthly U.S. import value. Starting on “Liberation Day” in April, each additional exemption is factored in from the day it was introduced. Certain imports fall under multiple exemption lists, meaning there is a slight overlap among categories. To avoid this, Figure 3 uses the general IEEPA exemptions from “Liberation Day” as the base exemption. Each additional exemption announcement represents the newly exempted import value rather than that category’s total exemption value. The chart also displays goods subject to Section 232 tariffs but exempt from IEEPA tariffs (orange).

Figure 2: IEEPA Exemptions as a Percent of Monthly U.S. Import Value (2025)

Source: The White House, United States International Trade Commission

The Present: Section 122 Exemptions

On February 20, 2026, the Supreme Court ruled that President Trump’s use of IEEPA to impose tariffs exceeded presidential authority, thereby striking down the IEEPA tariff regime. Immediately after, the Trump Administration turned to Section 122 of the Trade Act of 1974 which allows the president to implement tariffs up to 15 percent on imports for a maximum of 150 days. The president elected to impose 10-percent Section 122 tariffs which took effect on February 24 and drop the U.S. effective tariff rate to around 10 percent. Section 122 tariffs will expire July 24 unless they are renewed by Congress; they may be struck down sooner if the ongoing court case challenging their legal footing is decided expeditiously.

The exemptions from Section 122 tariffs are largely drawn from and expand upon those of the IEEPA regime, essentially grouping them all into the same basket. For the 150 days of Section 122, this research estimates that approximately 62 percent of U.S. imports will be exempted. Some of these goods will still be subject to new and upcoming Section 232 tariffs, meaning 47 percent of imports will be exempt from Section 122 and 232, a nearly 20 percentage point increase from the previous IEEPA exemptions.

Figure 3: 150 Days of Section 122 Tariff Regime Exemptions as a Percentage of U.S. Imports

| Exempt from Section 122 |

61.7% |

| Exempt from Section 122, Not Subject to Section 232 |

46.6% |

Source: The White House, United States International Trade Commission (February 24–July 24, 2026)

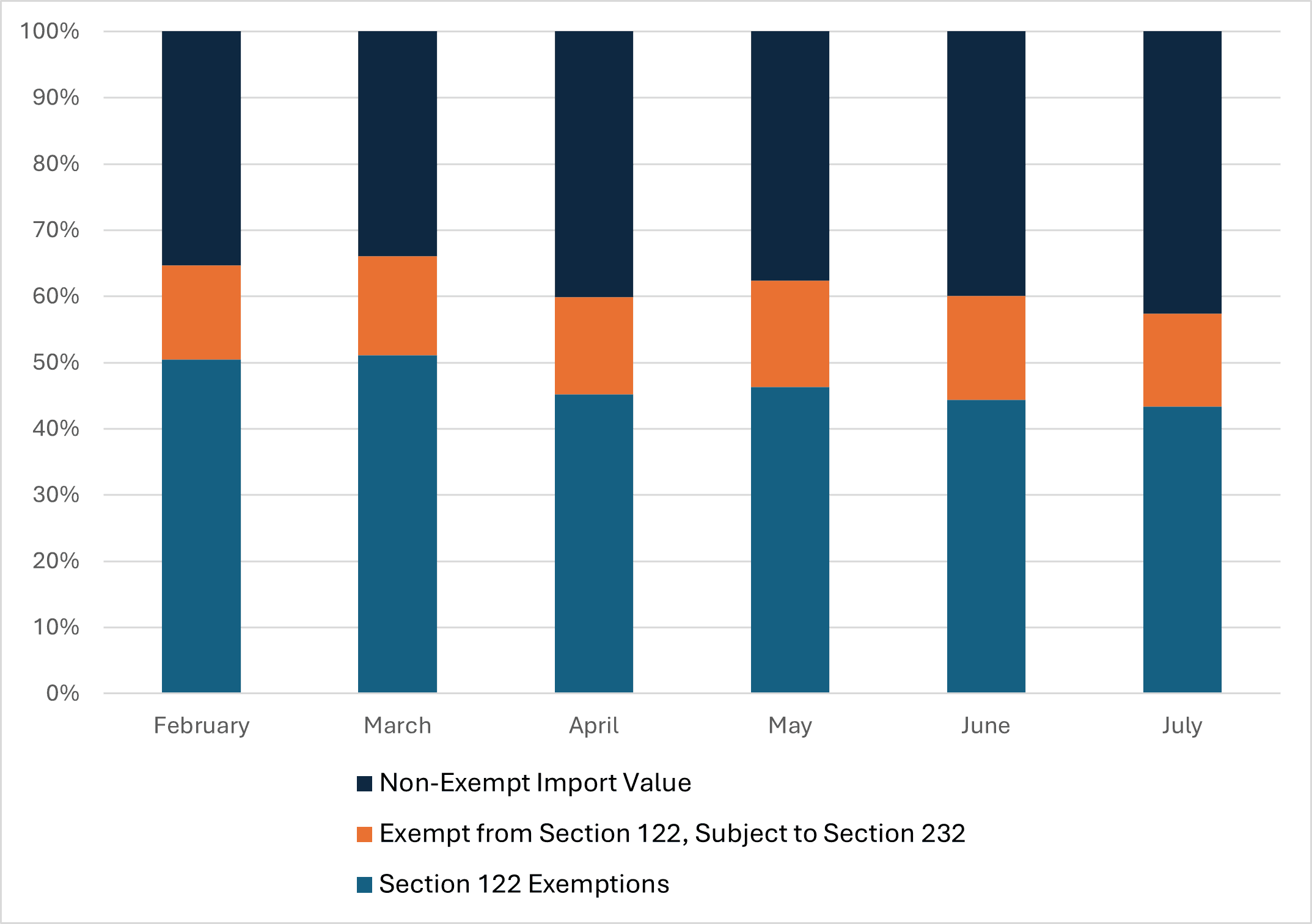

Figure 4: Estimate of Section 122 Exemptions as a Percent of Monthly U.S. Import Value

Source: The White House, United States International Trade Commission

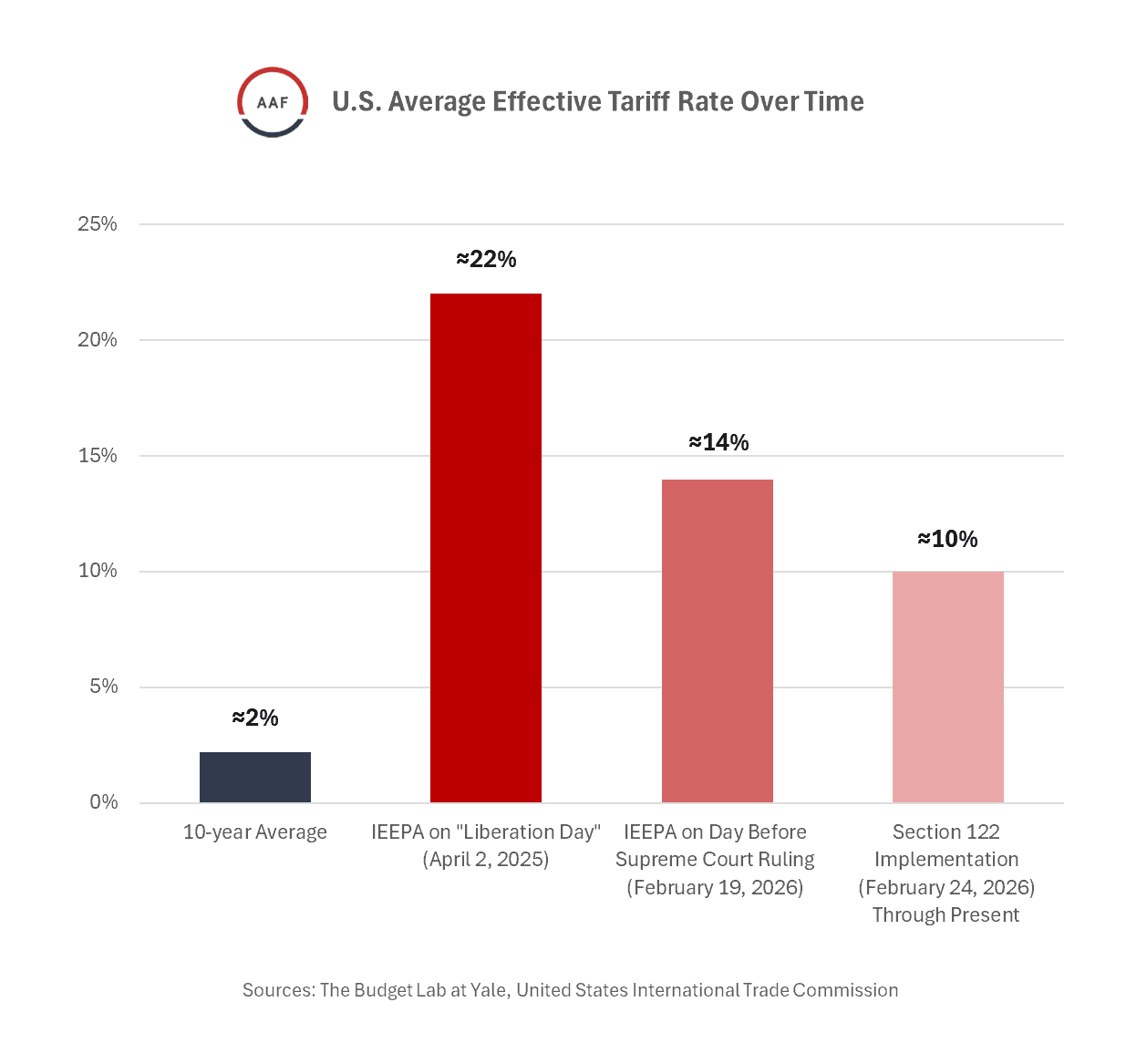

To illustrate the scale of the IEEPA exemptions compared to Section 122 exemptions, Figure 5 displays each regime’s exemptions if they both hypothetically lasted for a full year. This research’s analysis of the IEEPA regime is over the course of roughly nine months, while Section 122 is expected to last just five months. This chart provides a common frame of reference to illustrate how Section 122 provides far more extensive exemptions. Similarly, Figure 6 shows the changes in the overall effective U.S. tariff rate at various important points in time since before President Trump took office in January 2025.

Figure 5: IEEPA and Section 122 Annualized Exemptions (Percent of U.S. Imports)

|

IEEPA Full Year of Exemptions |

Section 122 Full Year of Exemptions |

|

| Exempt from Baseline Tariff |

42.1% |

62.4% |

| Exempt from Baseline Tariff, Not Subject to Section 232 |

32.2% |

47.8% |

Source: The White House, United States International Trade Commission

Figure 6: U.S. Average Effective Tariff Rate Over Time

USMCA Compliance

An equally important component of the administration’s tariff carveouts has been the United States-Mexico-Canada Agreement (USMCA). Since the opening days of the IEEPA regime, goods that are USMCA-compliant have faced a 0-percent tariff, which has been one of the most consequential tariff exemptions thus far. It has exempted well over 80 percent of imports from Mexico and Canada.

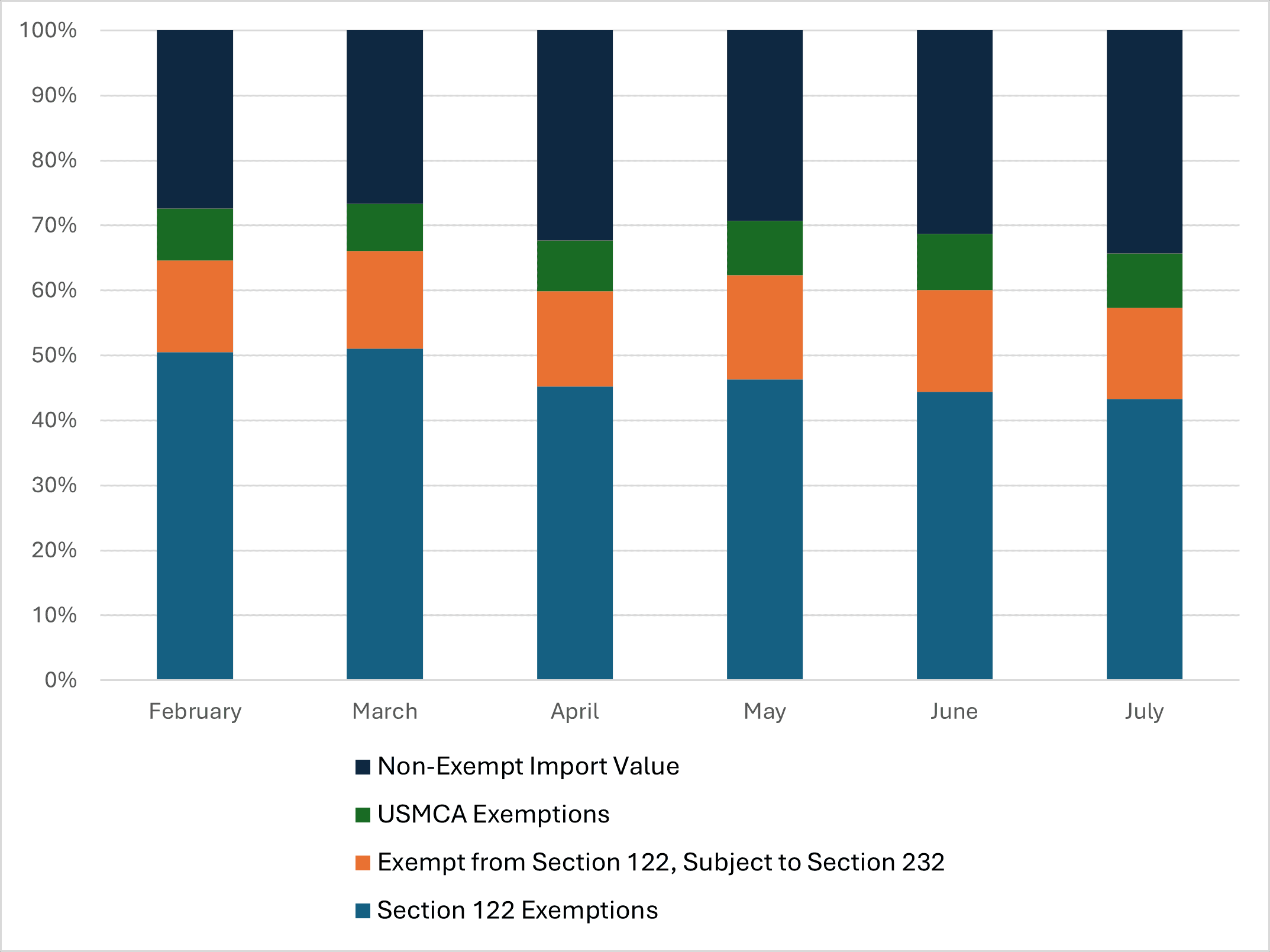

According to this research, USMCA compliance brought total IEEPA tariff exemptions from 38–51 percent of U.S. goods imported since “Liberation Day.” Under the new Section 122 tariff regime, the USMCA compliance rate approaches 90 percent for both Canada and Mexico. When factoring in USMCA, total Section 122 exemptions increase from 62 percent to roughly 70 percent of U.S. imports. Figure 7 displays the estimated exemptions stemming from USMCA compliance for the 150 days of Section 122. The second line of the table shows the estimated tariff exemptions that are unique to USMCA compliance and avoid any overlap with general Section 122 exemptions. Additionally, the table shows that roughly 55 percent of imports will be exempt from both Section 122 and Section 232 tariffs.

Figure 7: Exemptions From USMCA Compliance as a Percentage of U.S. Imports

|

150 Days of Section 122 |

|

| Total USMCA Exemptions |

23.8% |

| USMCA Exemptions, Excluding Section 122 Exemption Overlap |

8.0% |

| Total Exemptions (USMCA + Section 122) |

69.7% |

| USMCA + Section 122, Not Subject to Section 232 |

54.6% |

Source: The White House, United States International Trade Commission

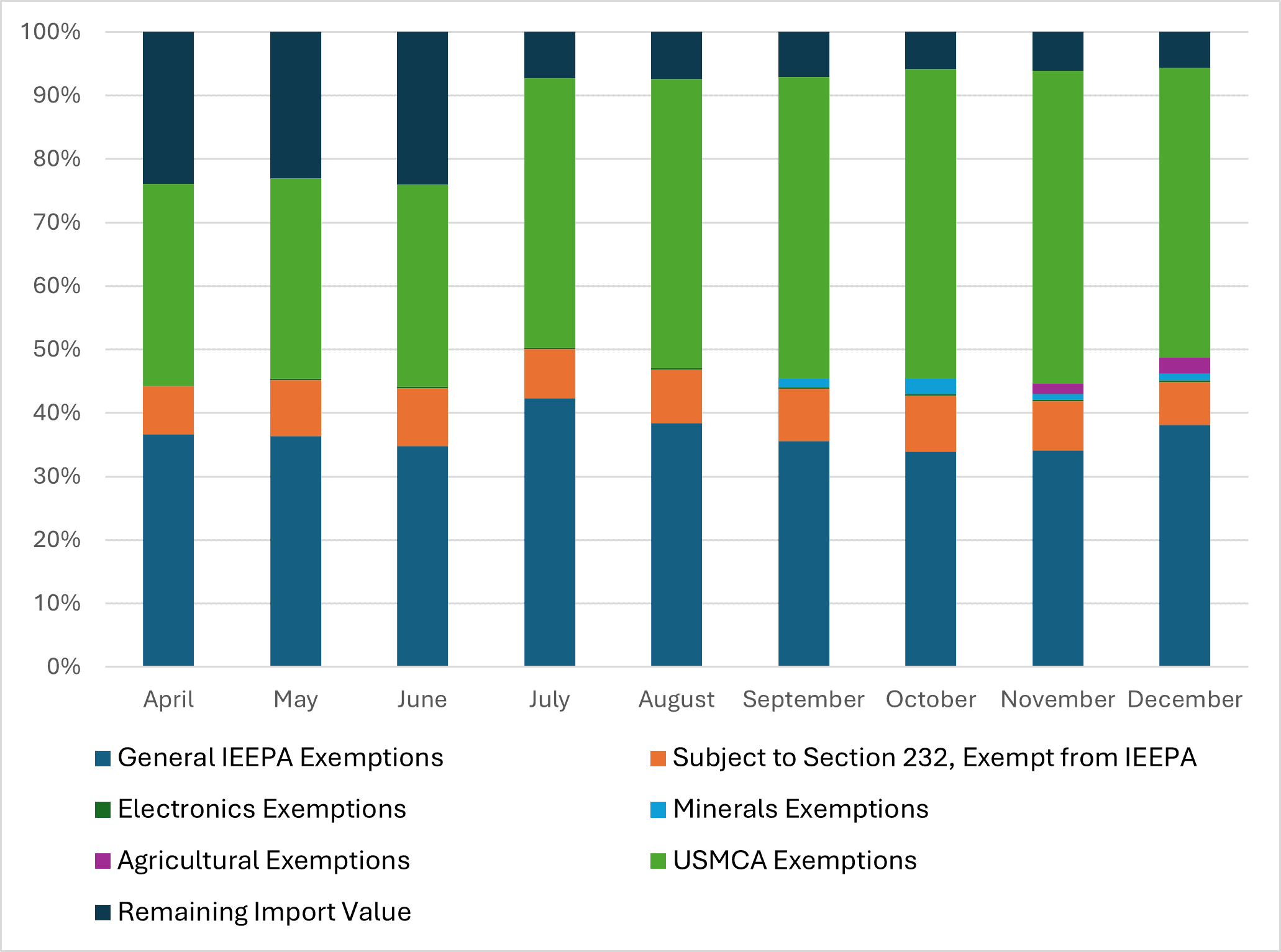

Figure 8: USMCA and IEEPA Exemptions as a Percent of Monthly Import Value (2025)

Source: The White House, United States International Trade Commission

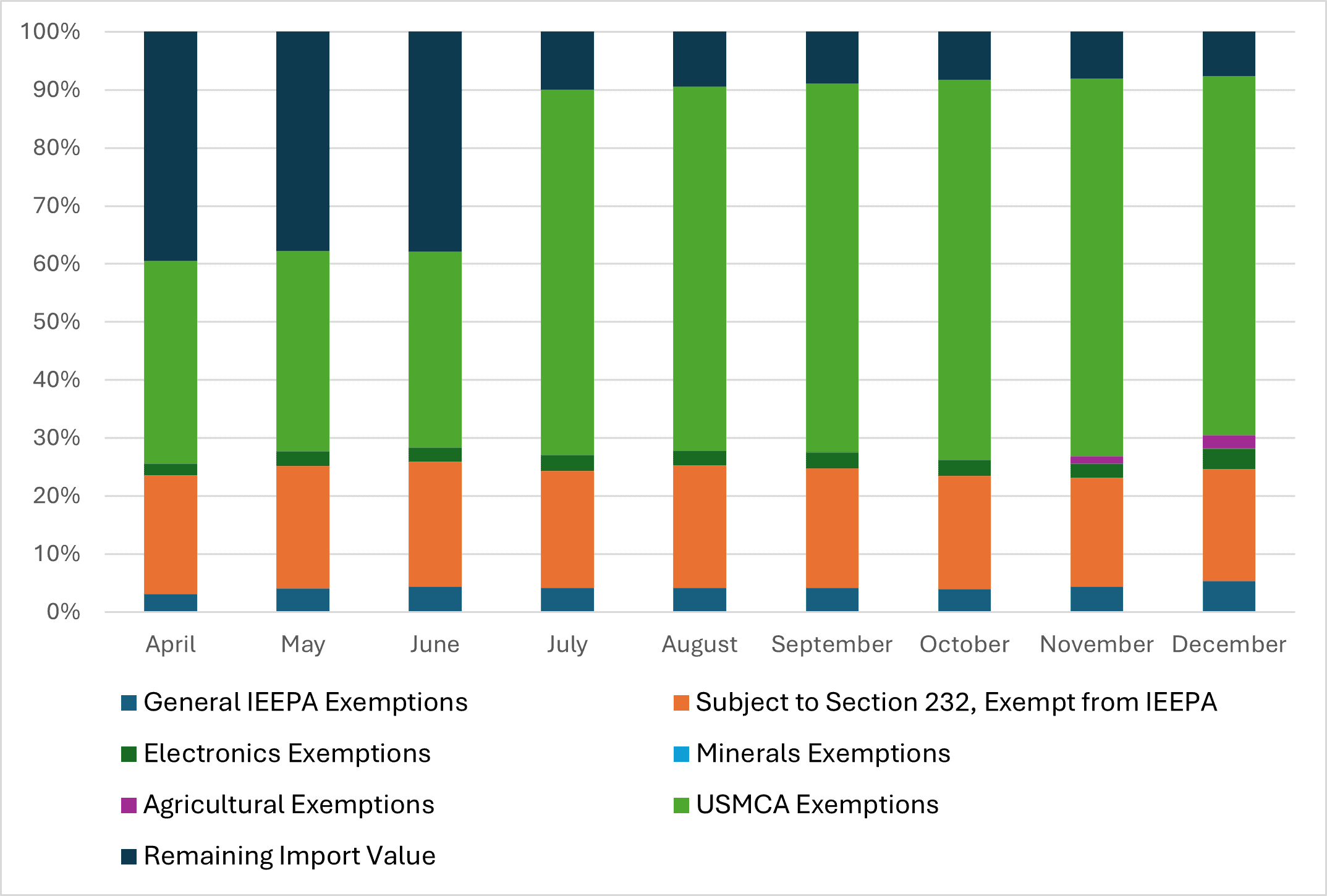

Figure 9: Estimate of USMCA and Section 122 Exemptions, Percent of Monthly Import Value

Source: The White House, United States International Trade Commission

What and Who Are Exempted?

Many of the administration’s tariff exemptions are in sectors dominated by consumer products and intended to address concerns over rising prices. For example, the administration exempted wide swaths of U.S. agricultural imports due to consumer discontent with high beef, coffee, and other grocery prices. Similarly, critical minerals and other imports not found or produced in high enough quantities within the United States have also been exempted, in part due to supply chain disruptions stemming from the trade war with China.

Big businesses have been the primary direct beneficiaries of exemptions, possibly reflecting their lobbying power and visibility with the administration. For example, electronics and semiconductor exemptions benefited Apple, Nvidia, and other companies investing tens of billions of dollars in the United States. (As with any other business tax relief, market competition generally leads businesses to pass some portion of tax savings on to their customers.)

The Future: The 2026 Tariff Outlook

With the Section 122 tariff regime set to end on July 24, it is important to consider what the next iteration of President Trump’s tariff policy might be and what that means for tariff exemptions. There are two main possibilities for the future. The first is that the administration tries to extend the Section 122 regime an additional 150 days either through a congressional vote or by re-implementing a second wave of Section 122 tariffs after the first wave expires. Given the aforementioned 150-day limit, if the administration imposed a second round of Section 122 tariffs, it would almost certainly face legal scrutiny and not be a durable option. With that said, it is possible the administration could attempt to impose a second Section 122 regime at the maximum 15 percent tariff rate in the hopes it is treated as an entirely separate entity rather than a cheeky re-implementation.

The second option is that the administration lets the Section 122 regime expire, instead using Section 232 in conjunction with Section 301 of the Trade Act of 1974 to build a third tariff regime. While Section 232 allows tariffs for national security, Section 301 investigations can lead to tariffs addressing other countries’ unfair trade practices. There are currently multiple Section 301 investigations into 86 countries covering more than 99 percent of the total U.S. import value in 2025. (Note, however, that the current 301 investigations are themselves being conducted in an unprecedented process, and any resulting tariffs could be subject to legal challenge.) The fact Section 301 investigations are ongoing alongside additional Section 232 investigations may signal that this will be the Trump Administration’s approach going forward.

Section 301 and 232 tariffs are more constrained than both IEEPA and Section 122 as they only target certain industries and products and are not meant to be used universally. This means that the administration will likely only apply this tariff regime to a subset of imports rather than roll back its tariff policy via exemptions. With that said, the administration recently overhauled its Section 232 tariffs on steel, aluminum, and copper by lowering tariffs and adding exemptions for various products (read more here). Only time will tell what the third tariff regime might look like, but it will likely avoid imposing tariffs on the products that have been exempted thus far.

Figure 10: Implemented and Ongoing Section 232 Investigations

|

Investigation |

Start Date | Implementation |

Number of Days and Deadline Estimates |

|

Copper |

March 10, 2025 | August 1, 2025 | 144 days |

|

Timber and Lumber |

March 10, 2025 | October 14, 2025 | 218 days |

| Semiconductors | April 1, 2025 | January 15, 2026 |

289 days |

|

Pharmaceuticals |

April 1, 2025 | Announced April 2, 2026 | July 31, 2026, and September 29, 2026 |

| Trucks | April 22, 2025 | November 1, 2025 |

193 days |

|

Critical Minerals |

April 22, 2025 | Ongoing | July 12, 2026 |

| Aircraft and Jet Engines | May 1, 2025 | Ongoing |

May 11, 2026 |

|

Polysilicon |

July 1, 2025 | Ongoing | July 11, 2026 |

| Unmanned Aircraft Systems | July 1, 2025 | Ongoing |

July 11, 2026 |

|

Wind Turbines |

August 13, 2025 | Ongoing | August 23, 2026 |

| Personal Protective Equipment | September 2, 2025 | Ongoing |

September 12, 2026 |

| Robots and Machinery | September 2, 2025 | Ongoing |

September 12, 2026 |

Appendix

Figure 11 displays the various IEEPA exemption categories as a percentage of total IEEPA exemptions for a better understanding of the breakdown.

Figure 11: IEEPA Exemptions by Category (2025)

Source: The White House, United States International Trade Commission

Figure 12: Canada USMCA and IEEPA Exemptions as a Percent of Monthly Import Value

Source: The White House, United States International Trade Commission

Figure 13: Mexico USMCA and IEEPA Exemptions as a Percent of Monthly Import Value

Source: The White House, United States International Trade Commission

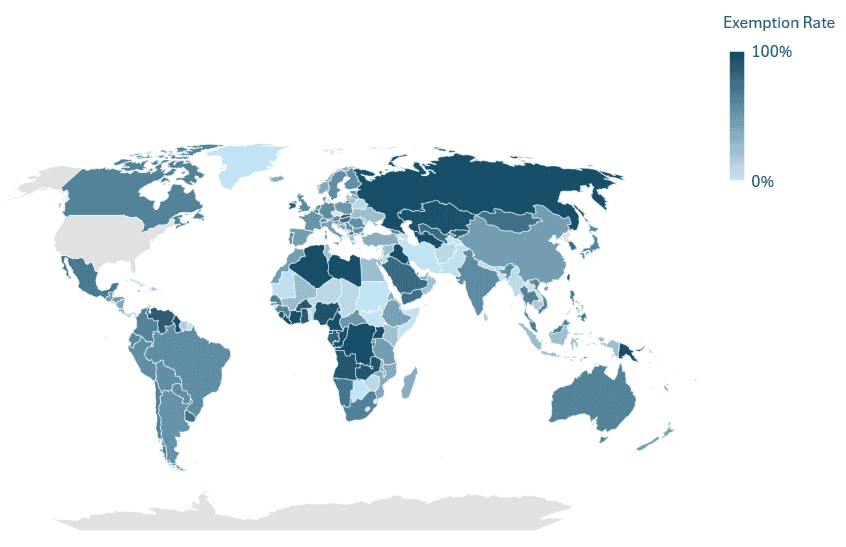

Figure 14: Section 122 Exemptions as a Percentage of U.S. Imports by Country

Source: United States International Trade Commission

Figure 15: Top Section 122 Exemption Values by Country (February–July 2026 Estimates)

|

Country |

Estimated Exemptions ($ Billions) | Exemption Rate |

Share of U.S. Imports |

| Mexico |

$153 |

69% |

10.8% |

| Canada |

$98 |

63% |

6.9% |

| Taiwan |

$66 |

86% |

4.7% |

| Ireland |

$53 |

84% |

3.7% |

| China |

$52 |

45% |

3.7% |

| Vietnam |

$46 |

60% |

3.3% |

| Japan |

$39 |

63% |

2.8% |

| South Korea |

$39 |

71% |

2.7% |

| Germany |

$37 |

57% |

2.6% |

| Switzerland |

$29 |

66% |

2.0% |