Research

May 11, 2018

The Impact of Raising the Threshold for Medicare Part D Catastrophic Coverage

Executive Summary

The Affordable Care Act temporarily slowed the growth rate of the catastrophic coverage threshold for Medicare Part D, allowing more people to enter the catastrophic coverage phase where the federal government covers most of the costs. This temporary reduction will end in 2020 and the threshold will again reflect the true growth in beneficiary expenditures. The Bipartisan Budget Act of 2018 (BBA) made further changes to Part D. These changes will affect different stakeholders in different ways, but the primary effect has been to increase overall expenditures in catastrophic coverage.

- The federal government, which pays 80 percent of the costs in the catastrophic phase, has faced substantial cost increases because of the lower threshold, and raising it should slow the rate at which those costs increases.

- Beneficiaries with the highest costs have benefitted from the lower threshold, as entering the catastrophic phase more quickly lowers their out-of-pocket (OOP) costs. But those who have not entered catastrophic coverage have seen their premiums rise without any savings in OOP expenditures.

- The lower threshold has saved drug manufacturers money, and raising it will cost them more. The higher threshold in combination with the increase in the coverage gap manufacturer rebates mandated by the BBA will increase their costs even further.

- The impact to insurers has been less straightforward and continues to evolve as their liability for costs in the coverage gap has continually been changing since 2010 and will continue to do so through 2019. Most of the savings insurers have gained in the coverage gap thus far have been offset by increased expenditures in catastrophic coverage.

Introduction

The Medicare Part D prescription drug program provides Medicare beneficiaries with robust insurance coverage for outpatient prescription drugs. All Part D plans are offered by private insurance companies that negotiate with drug manufacturers to provide patients with access to discounted prices. The federal government subsidizes these plans heavily and regulates them regarding coverage and affordability.

The Affordable Care Act (ACA) temporarily slowed the growth rate of the catastrophic coverage threshold within the Part D program, yet this change is set to expire in 2020. The catastrophic coverage threshold is the point at which the government begins to pay most of the cost of medication, with the intent of preventing those costs from overwhelming beneficiaries or insurers.

This paper examines the financial impact this change has had on the various stakeholders over the past few years and what effect its expiration will have in 2020. It analyzes these shifts particularly in light of recent provisions in the Bipartisan Budget Act of 2018 (BBA) which have further changed the Part D program.

Background

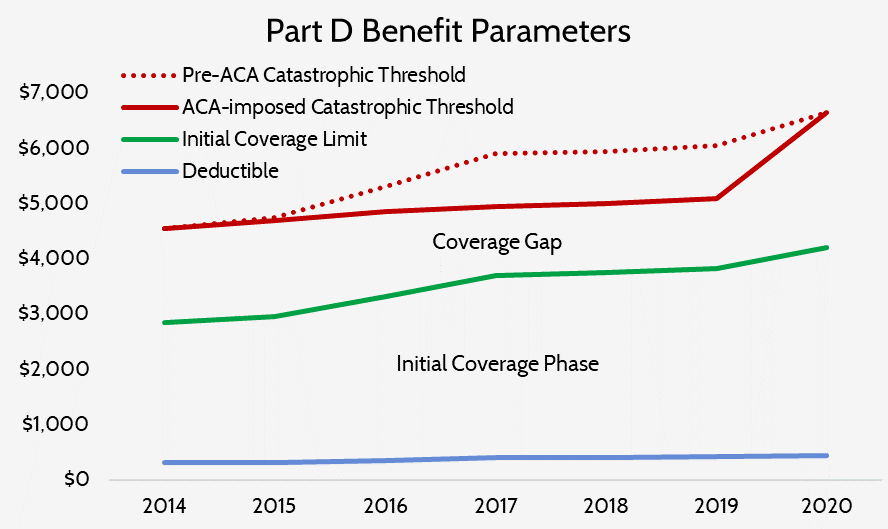

Part D prescription drug plans have four phases of insurance coverage:

- The deductible, where the beneficiary must cover all costs until the deductible is reached;

- The initial coverage phase, where beneficiaries pay 25 percent of the cost of their drugs and insurers pay the other 75 percent, until total expenditures reach the initial coverage limit;

- The “coverage gap,” so named for the structure of this phase prior to the ACA when the beneficiary resumed full responsibility for the cost of their drugs until reaching the catastrophic coverage threshold (the ACA and the BBA have significantly altered coverage in this phase, as explained below); and

- The catastrophic or reinsurance phase, where beneficiaries pay 5 percent of all remaining costs until the end of the plan year, insurers pay 15 percent, and the government pays 80 percent.

The ACA included a provision to close the coverage gap gradually in several steps. First, the federal government provided all beneficiaries who entered the coverage gap in 2010 a $250 rebate, paid from the Medicare Prescription Drug Account.[1] Next, beginning in 2011 drug manufacturers were required to pay a rebate of 50 percent of the negotiated price for all brand-name drugs that a beneficiary took while in the coverage gap phase of her insurance. The beneficiary covered the remaining 50 percent of the cost. Then, starting in 2013, insurers began paying some of the costs formerly covered by beneficiaries. Insurers’ liability gradually increased each year, starting at 2.5 percent in 2013 until reaching (under the ACA’s plan) 25 percent in 2020. As the insurer liability increased, the patient liability decreased by the same amount. Thus, by 2020 (under the ACA) the patient would pay 25 percent, insurers 25 percent, and drug manufacturers 50 percent. At the same time, the ACA set up a parallel track for covering generics that gradually increased insurer liability for those medications to 75 percent by 2020, with patients covering the remaining 25 percent by then.

The ACA also required that the 50 percent manufacturer discount be included in the calculation of a patient’s out-of-pocket (OOP) costs, an inclusion that created the “True” OOP threshold (TrOOP). This calculation is used to determine when the patient moves into the catastrophic coverage phase. Including the manufacturer rebates in the TrOOP allows the beneficiary to reach catastrophic coverage more quickly, where their cost-sharing is reduced to 5 percent.

The BBA altered this process for closing the coverage gap. A primary change was that the BBA accelerated the process by one year, such that beneficiaries would pay 25 percent coinsurance in the coverage gap beginning in 2019, rather than 2020. Further, the BBA extended the mandatory manufacturer rebates to makers of biosimilars and increased the rebate amount from 50 percent to 70 percent. The additional rebate will be used to reduce the insurer’s liability for brand-name drugs and biosimilars in the coverage gap to only 5 percent. The BBA did not make any changes to the coverage of generic medicines.

The Part D “Cliff”

The statute establishing the Part D benefit design provides that the threshold of each coverage phase should grow at the rate of overall beneficiary spending. The ACA, in addition to making the changes to the coverage gap outlined above, included a provision that temporarily slowed the growth rate of just the catastrophic coverage threshold for the years 2014-2019.[2] In 2014, the new formula produced no change from what the threshold would have been before the ACA, and in 2015 the threshold was only $50 less than what it otherwise would have been. But in 2016 the threshold was $450 lower and by 2019 it will be nearly $1,000 lower, as shown in the chart below. This temporarily slowed growth rate has effectively shortened the coverage gap and, as a result, increased the number of beneficiaries who reach catastrophic coverage. In 2020, the threshold will return sharply to where it would have been had this temporary change never been included in the ACA. As a result, the catastrophic coverage threshold is scheduled to increase from $5,100 in 2019 to $6,650 in 2020—a 30 percent increase.

Analyzing the Impact on the Various Stakeholders

Some stakeholders have benefitted from this temporary change while others have not, and conversely, its expiration will benefit some and not others. The forthcoming impacts are different now than they otherwise would have been given the aforementioned provisions included in the BBA. The BBA’s changes to the coverage gap provisions will result in high-cost beneficiaries moving through the coverage gap and into the catastrophic coverage phase more quickly, as explained here. The financial impact to each stakeholder then depends on that stakeholder’s share of the liability for a beneficiary’s costs in the coverage gap relative to the catastrophic coverage phase. Unfortunately for policymakers who may be considering potential legislative responses, these competing interests include those of beneficiaries and taxpayers: what reduces costs for some beneficiaries increases costs for the federal government (i.e. taxpayers), as explained below.

Methodology

Because the subject of this paper is the effect of changes to the catastrophic coverage threshold, the estimates in this analysis are based on expenditures for those enrollees who reach the catastrophic coverage phase. Specifically, the figures in this analysis are based on 2015 average per-capita expenditures (the most recent publicly available) for non-LIS high-cost enrollees.[3] To estimate expenditures beyond 2015, a steady annual growth rate in per capita expenditures of 10.4 percent, equal to the annual growth rate in expenditures for non-LIS high-cost enrollees from 2010 to 2015, was assumed.[4] Expenditures in the coverage gap were calculated based on each stakeholders’ share of costs in each year, assuming the same ratio of brand-name to generic expenditures included in the CMS Part D Call Letter each year (a 9:1 ratio is assumed in 2020).[5] The expenditure threshold for each phase of coverage in 2019 and 2020 are as projected in the most recent Medicare Trustees Report.[6] Expenditures in catastrophic coverage were calculated based on each stakeholders’ liability for those costs.

Impact on Beneficiaries

High-cost enrollees are those beneficiaries who incur prescription drug costs high enough to reach the catastrophic phase of coverage. The number of high-cost enrollees has been growing rapidly, at an average annual rate of 9 percent between 2010-2015 and reaching 3.6 million in 2015.[7] While nearly three-fourths of high-cost enrollees were individuals eligible for the low-income subsidy (LIS)—which greatly limits these individuals’ OOP costs throughout each phase of coverage—growth in the number of non-LIS enrollees has averaged 21 percent annually.[8] If that trend has held steady, by 2020 an estimated 1.68 million non-LIS beneficiaries would be expected to reach catastrophic coverage. What’s more, with the BBA’s increased manufacturer rebates accelerating how quickly beneficiaries reach their TrOOP limit, this number would be expected to increase even further. Nevertheless, the looming increase in the catastrophic coverage threshold is so large that it will likely reduce the number of beneficiaries who reach catastrophic coverage, relative to the current projection.

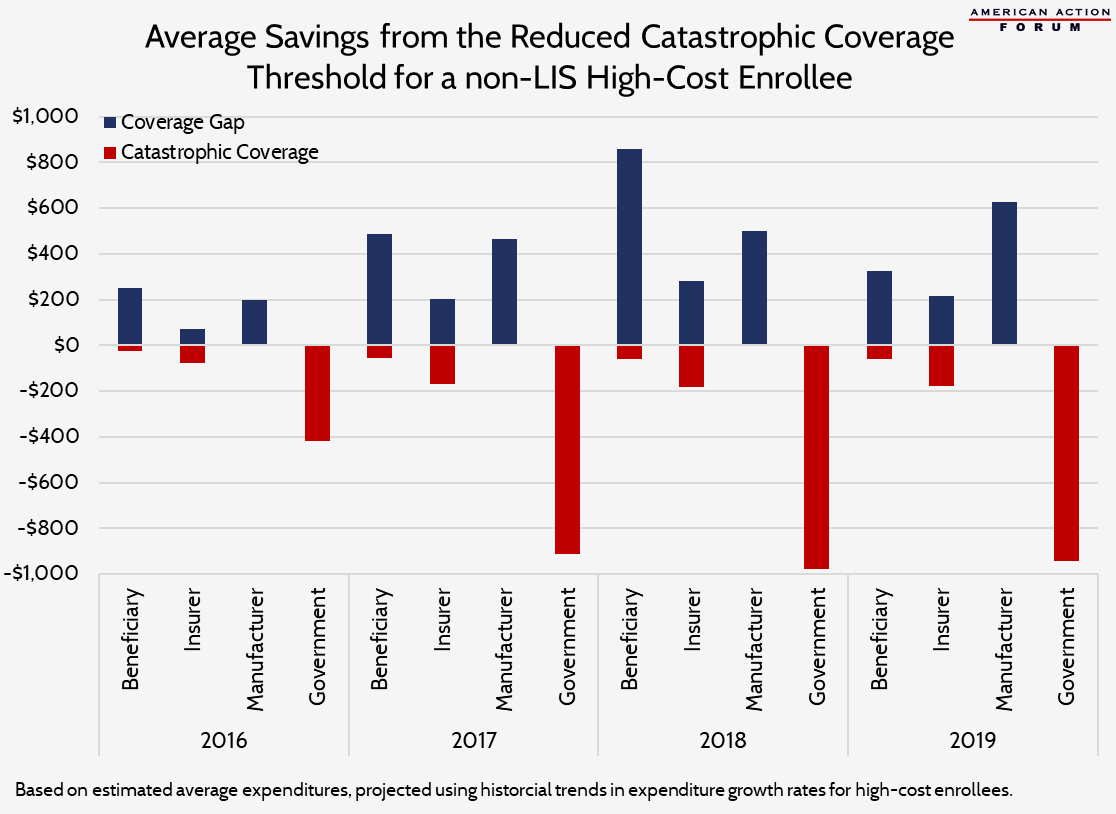

Because each beneficiary pays 25 percent coinsurance in the coverage gap compared with five percent in the catastrophic coverage phase, beneficiaries have certainly benefitted from this temporary reduction in the catastrophic coverage threshold. From 2016 to 2018, non-LIS high-cost beneficiaries have saved $1,594 in the coverage gap and spent an extra $144, on average, in catastrophic coverage, for a net estimated savings from the reduced threshold over this period of $1,450, relative to what they otherwise would have paid. The BBA’s changes starting next year that increase beneficiaries’ calculated TrOOP—which will similarly push them through the coverage gap more quickly—will result in additional savings for the highest-cost enrollees.

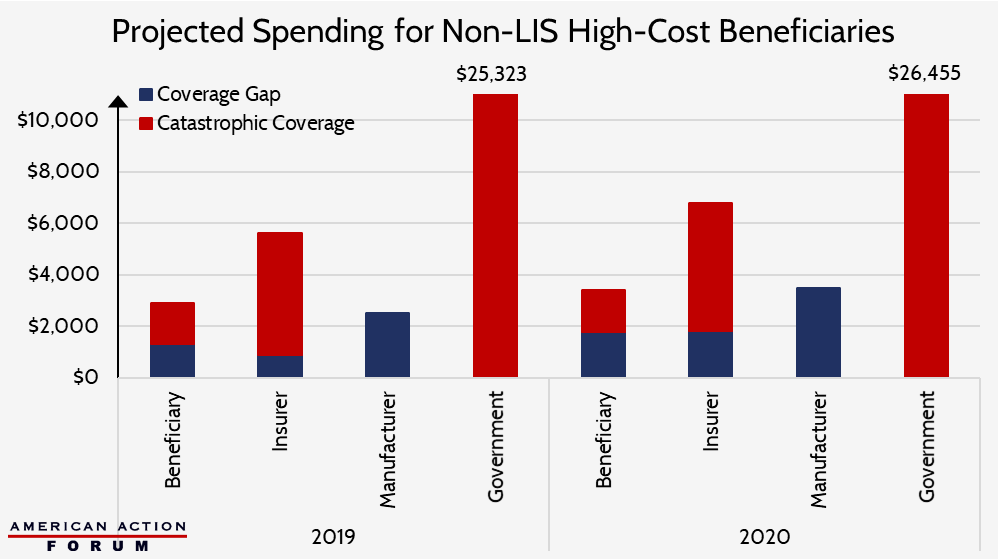

With the temporary reduction in the catastrophic coverage threshold expiring in 2020, however, those savings will be short-lived for many of these beneficiaries, as they will suddenly be less likely to move into catastrophic coverage. An elevated threshold that would cause a beneficiary to stay in the coverage gap longer, paying a coinsurance rate that is five times what they would pay beyond the coverage gap, will undoubtedly increase beneficiaries’ OOP costs. If the catastrophic coverage threshold increases as scheduled in 2020, from $5,100 in 2019 to $6,650, beneficiaries that do reach that threshold will pay an extra $461 in the coverage gap, and $71 more in the catastrophic phase (well below their typical cost growth in the catastrophic phase). This one-year OOP cost increase will be more than the total estimated increase in annual OOP expenditures for non-LIS high-cost enrollees between 2015 and 2018. However, because these individuals are expected to pay nearly $300 less in 2019 than what they will pay OOP in 2018 (because of the BBA’s changes to the coverage gap), their OOP expenditures in 2020 should only be about $400 more than their 2018 expenditures.

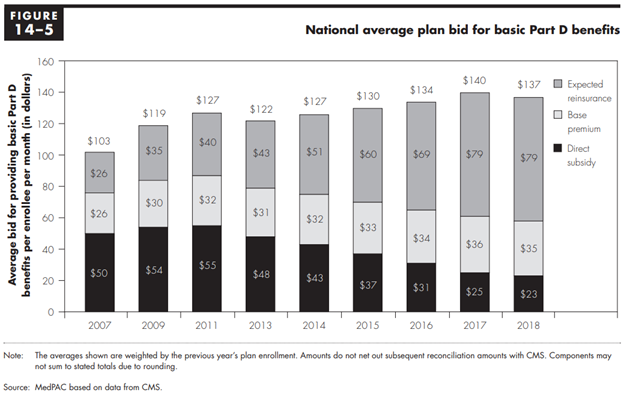

The ACA’s changes have indirectly affected costs for the two-thirds of non-high-cost beneficiaries, as well. The federal government subsidizes the Part D program primarily through direct premium subsidies and by providing reinsurance in the catastrophic coverage phase. By law, the government must subsidize three-fourths of total program expenditures. As the government’s reinsurance costs have increased, the direct premium subsidy has necessarily had to decrease, as shown in the chart below from the March 2018 MedPAC Report to Congress.[9] Thus, beneficiaries are receiving less of a subsidy for their monthly premiums as a result of each change that accelerates beneficiaries into catastrophic coverage. This impact is most pronounced for lower-cost beneficiaries who never reach catastrophic coverage, since their primary benefit from the Part D program is the subsidization of premiums.

Impact on the Federal Government

The federal government’s reinsurance costs move in the opposite direction of those for high-cost beneficiaries and have certainly increased as a result of this temporary slowdown in the growth rate of the catastrophic threshold. Once patients move into catastrophic coverage, the federal government provides reinsurance by paying 80 percent of the costs incurred by beneficiaries. The more patients that reach that phase, and the more quickly they reach it, the higher the cost to the government. The government’s reinsurance costs have been growing rapidly in recent years, now accounting for more than two-thirds of the government’s subsidy of the basic benefit, up from just over one-third in 2010. [10] Reinsurance costs have grown at an average annual rate of 24 percent since then, more than double the annual rate of growth prior to that.[11] Between 2016-2018, the federal government has paid an estimated $2,304 in additional reinsurance costs, on average, for each non-LIS high-cost enrollee as a result of the reduced threshold. In 2019, the government is expected to pay an additional $544 in reinsurance costs for high-cost beneficiaries because of the increased manufacturer rebates and nearly $1,000 more because of the ACA’s reduced threshold. In 2020, when the catastrophic threshold increases to $6,650, the government’s reinsurance cost per beneficiary will still rise, but the increase is expected to be $1,132, on average, if historical expenditure trends continue, compared with an estimated $2,432 increase from 2017 to 2018. Moreover, aggregate reinsurance costs will grow less quickly as less beneficiaries will reach catastrophic coverage.

For the more than 12 million high-cost LIS beneficiaries, the government’s costs are spread throughout each coverage phase. The federal government pays all or most of an LIS beneficiary’s prescription drug costs, including their premiums and most of their out-of-pocket liabilities. For the more than 2.6 million LIS beneficiaries that currently reach the catastrophic coverage phase, the government pays less to cover the beneficiary’s OOP costs in the coverage gap under the reduced threshold, but those savings are offset by increased expenditures in catastrophic coverage.

Impact on Drug Manufacturers

With the ACA’s imposition of mandatory rebates in the coverage gap, drug manufacturers have benefitted from a shorter coverage gap, saving $1,162 per high-cost enrollee from 2016 to 2018, relative to what they otherwise would have had to pay without the reduced threshold. Now that the BBA will require drug companies to pay rebates of 70 percent, an extended coverage gap will prove even more costly than it otherwise would. Without passage of the BBA or the ACA’s reduction in the catastrophic coverage threshold, drug manufacturers would have paid $2,670, on average, in mandatory coverage gap rebates for each high-cost enrollee in 2019. Increasing the rebate amount to 70 percent, without the ACA’s changes to the threshold, would increase their cost $477 per enrollee, but the reduced threshold will save manufacturers $625 next year, resulting in an average rebate cost of $2,523. In 2020, when the threshold reduction provision expires, drug manufacturers will pay average rebates of $3,488 for each high-cost beneficiary, nearly $1,000 more than what they will pay in 2019.

Impact on Part D Plan Sponsors

The impact on plan sponsors (i.e. insurance companies) is less straightforward because they face costs in both the coverage gap and catastrophic coverage, and their liability is different in the coverage gap based on whether the beneficiary is taking generic or brand-name medicines. Because plan sponsors’ liability for brand-name drugs has just reached 15 percent this year—equal to their share of liability in the catastrophic phase—plan sponsors generally would have benefited until now from a lengthened coverage gap, where they paid only a small share of the costs, if their enrollees used a higher share of brand-name drugs. From 2016 through 2018, Part D sponsors have saved an estimated $121 because of the reduced threshold, on average, per high-cost beneficiary, with increased costs in catastrophic coverage offsetting most of their savings in the coverage gap.

Given the BBA’s changes reducing their liability for brand-name and biosimilar drugs in the coverage gap back down to 5 percent, insurers will certainly benefit from the threshold rising and extending the coverage gap, primarily as a result of fewer beneficiaries ever reaching catastrophic coverage, as explained here. While insurers will substantially benefit directly from the changes in the BBA, the reduced catastrophic threshold diminishes their savings. By 2019, insurers will be expected to save an estimated $40, on average, per high-cost enrollee, compared with estimated savings of $185 per enrollee had the BBA not been passed. In 2020, insurers will spend nearly $1,000 more in the coverage gap—primarily because of their increased liability for generic drugs—and $1,161 more, on average, in catastrophic coverage for each high-cost beneficiary than they spent in 2019. Like the government, though, insurers will save substantially in catastrophic costs as fewer beneficiaries reach that phase of coverage.

Conclusion

The Part D program has justifiably been lauded for keeping costs below expectations since its inception. If the current trend of rapidly increasing reinsurance costs continues, however, that praise may no longer be warranted. It is clear from the evidence that part of the reason for the growth in reinsurance costs is due to the provision in the ACA that temporarily slowed the growth rate of the catastrophic coverage threshold, which caused more beneficiaries to enter catastrophic coverage and to do so more quickly. This change to the threshold, in combination with allowing the mandatory drug manufacturer rebates in the coverage gap to count toward beneficiaries’ TrOOP, exacerbated the problem.

With the catastrophic threshold returning to a level reflective of the growth in beneficiary expenditures in 2020, the problem of increasing costs will be somewhat mitigated for the government (i.e. taxpayers). High-cost beneficiaries, in contrast, will face significant increases in their OOP expenditures, relative to increases over the past several years, which may be difficult for many of them to afford. Of course, the increased manufacturer rebates mandated by the BBA will offset some of these cost increases for beneficiaries, but will simultaneously reduce the savings the government would otherwise gain in reduced reinsurance costs when the catastrophic threshold rises. Subsequently, those rebates do not reflect a long-term solution to the problem of ever-growing reinsurance costs in the Part D program.

[1] The Medicare Prescription Drug Account is the Part D account of the Federal Supplementary Medical Insurance (SMI) Trust Fund from which Part D benefits are paid.

[2] Section 1101(d)(1) of the Health Care and Education Reconciliation Act of 2010

[3] MedPAC Report to Congress, March 2018, pg 425: http://www.medpac.gov/docs/default-source/reports/mar18_medpac_ch14_sec.pdf

[4] MedPAC Report to Congress, March 2018, pg 424: http://www.medpac.gov/docs/default-source/reports/mar18_medpac_ch14_sec.pdf

[5] Centers for Medicare and Medicaid Services, Announcements and Documents: https://www.cms.gov/Medicare/Health-Plans/MedicareAdvtgSpecRateStats/Announcements-and-Documents.html

[6] 2017 Medicare Trustees Report: https://www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-Trends-and-Reports/ReportsTrustFunds/Downloads/TR2017.pdf

[7] Department of Health and Human Services Office of Inspector General, January 2017: https://oig.hhs.gov/oei/reports/oei-02-16-00270.pdf

[8] MedPAC Report to Congress, Chapter 14, pg. 423: http://www.medpac.gov/docs/default-source/reports/mar18_medpac_ch14_sec.pdf

[9] MedPAC Report to Congress, Chapter 14, March 2018: http://www.medpac.gov/docs/default-source/reports/mar18_medpac_ch14_sec.pdf

[10] http://www.medpac.gov/docs/default-source/reports/mar18_medpac_ch14_sec.pdf?sfvrsn=0

[11] http://www.medpac.gov/docs/default-source/reports/mar18_medpac_ch14_sec.pdf?sfvrsn=0