The Shipment

August 7, 2025

Are We Liberated Yet?

(Not So) Fun Fact: The average price per pound of ground roast coffee has increased 16 percent in U.S. cities this year, with a 2.5-percent increase from the Shipment’s last reporting on June 12.

The Third Tariff Deadline Is the Charm

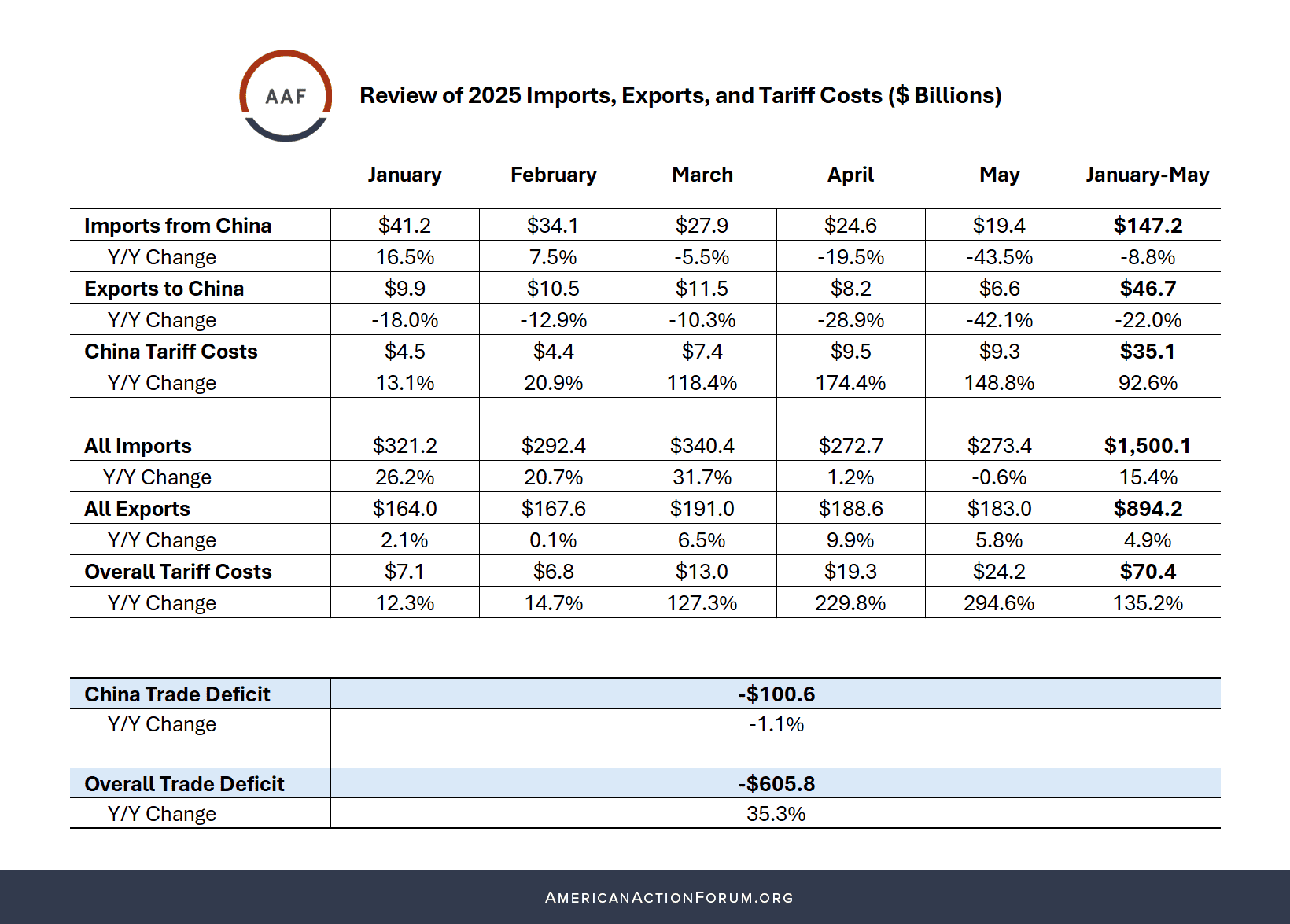

What’s Happening: President Trump’s “Liberation Day” tariffs – updated last week to reflect new rates – are in place as of today. These wide-sweeping tariffs were initially announced on April 2 but delayed until July 9 and again until August 1 to provide more time for trade negotiations and presumably to stave off economic costs. As of now, the European Union, Japan, South Korea, Indonesia, Vietnam, and the United Kingdom have all reached a deal that includes less-excessive tariff rates. Mexico has received an additional 90-day tariff pause until October, while China’s deadline is August 12. Ongoing negotiations may result in another 90-day extension, with tariff rates on Chinese imports set to potentially rise above 100 percent if talks fall through. Meanwhile, several notable U.S. trade partners haven’t shown much progress on reaching an agreement. The Trump Administration imposed a 25-percent tariff on India due to its continued importation of Russian energy products, a 35-percent tariff looms over Canada, and Switzerland is racing to find an off-ramp from the U.S. 39-percent tariff. Furthermore, a 100-percent tariff on semiconductors was announced in the Oval Office yesterday, although the president stated that companies with domestic manufacturing plants would be exempt.

Why It Matters: Last week’s adjustment to “Liberation Day” tariff rates, combined with the 50-percent tariff on India, raises the Shipment’s anticipated annual tariff costs to over $380 billion, which would be passed on to U.S. businesses and consumers. That figure tops last week’s estimate of $366 billion but falls in line with past American Action Forum research, which put the annual cost range between $366.5–$391.6 billion. While inflation has not yet risen significantly, there are warning signs that tariffs are beginning to negatively impact the U.S. economy. Last week’s jobs report was weaker than expected and downward revisions to May and June showed nearly 260,000 fewer jobs were created than previously estimated. Adjusting for each industry’s total employment, these revisions primarily impacted trade-related sectors including retail trade, transportation and warehousing, and durable goods. Construction jobs were also sharply revised downward, possibly due to companies pausing projects as a result of uncertainty surrounding the impact of tariffs on input costs or other economic headwinds.

Additionally, there are certain goods that are beginning to display inflationary pressures, including beef, frankfurters, fresh fruits, coffee, linens, cookware, and certain clothing. Many of these goods experienced a monthly price jump of between 2 and 5 percent. It is important to keep in mind that these economic tremors are being felt primarily after the imposition of a universal 10-percent tariff. The full force of the Trump Administration’s tariffs has been on hold since April 2, which means much higher rates are about to kick in.

Looking Ahead: Whether tariff rates will be maintained at current levels or more deals are struck remains to be seen. Despite hope that negotiations would result in a mutual opening of markets and lowering of costly trade barriers, tariffs have been baked into all recent trade deals at relatively high levels compared to 2024. As of yesterday, the prospect of more trade deals seems slim. Switzerland was unable to sway the president to lower tariffs, India issued a statement that it will “protect its national interests” and Brazil, too, may impose retaliatory tariffs. Canada also appears to be out of luck for now, even though the country gave up its digital services tax weeks ago in exchange for a tariff pause and better trade terms. The market seems to have shrugged off “Liberation Day” part two as the S&P 500 began the day in the green, a completely different reaction from that after April 2. If this is any indication, financial markets must be anticipating a temporary economic impact or a reversal of hardline tariff policy. It could also be the case that another major selloff is unlikely, with investors waiting to see how tariffs work their way into future earnings and data reports.

![]()