The Shipment

June 11, 2026

The Oil Problem – Higher Inflation and Lower Growth

Rising Inflation and Slowing Growth

What’s Happening: Yesterday, the Bureau of Labor Statistics (BLS) released the monthly Consumer Price Index (CPI) update, showing inflation data for U.S. consumers for May. Monthly CPI was up 0.5 percent, while year-over-year CPI rose a staggering 4.2 percent, largely driven by rising energy prices. Although each of these CPI reads matched expectations, this data marks the sharpest year-over-year uptick in consumer prices since April 2023, and the highest year-over-year CPI increase in either this or the first Trump Administration. The conflict with Iran has been primarily responsible for rising oil and gas prices due to approximately 20 percent of the world’s supply coming through the Strait of Hormuz. This has caused the CPI energy category to rise 23.5 percent year over year, with gasoline up 40.5 percent and fuel oil up nearly 60 percent. The data also shows that many food categories such as certain vegetables, coffee, and beef products rose by double digits. While few product categories saw a year-over-year decline in prices, eggs dropped by 35 percent, smartphones fell by 11 percent, and prescription drugs were down by 2 percent, to name a few. The overall trend of rising prices, however, has raised the likelihood that the Federal Reserve maintains or hikes interest rates. This troubling CPI report comes around the same time as news that first-quarter real gross domestic product (GDP) growth was revised downward from 2.0–1.6 percent. There is widespread fear that the conflict in Iran will further exacerbate the impact of rising prices and lower growth for the global economy. As of this morning, the World Bank lowered its global growth forecast for the year from the 2.6-percent January estimate to 2.5 percent, which is notably lower than the 2.9-percent growth of 2025.

Why It Matters: The mixture of higher prices and slower GDP growth is a recipe for stagflation – an economic state characterized by reduced prosperity, purchasing power, and employment. As the Shipment noted in early March, the price of oil has a large impact on the global economy and a tangible impact on U.S. inflation, unemployment, and GDP. According to Apollo Global Management, a persistent oil shock that keeps prices at $100 a barrel through 2027 would result in headline inflation rising 0.7-percentage points, unemployment rising 0.1-percentage points, and real GDP falling by 0.1-percentage points. In mid-April, fears surrounding global growth became more acute as the International Monetary Fund lowered its growth projections for 2026. A recent World Economic Forum survey shows a sharp uptick in chief economists’ expectations of a severe global impact from the Strait of Hormuz closure. Given a severity scale of 0 to 100, economists’ view of the current situation rose from around 41 to 72 – assuming the strait opens this month. If the strait remains closed for much longer, the ranking rises to 83.5 which – for reference – approaches the COVID-19 pandemic, which ranked at 100. The same survey shows that many economists expect attributes of stagflation to primarily hit the Middle East, Europe, and Africa, while the United States is impacted but remains relatively resilient. Furthermore, the World Bank’s June report published today warns that if energy disruptions continue to last then global growth could slow to a meager 1.3 percent.

Rising consumer prices is not welcome news for the Trump Administration, which has attempted to address Americans’ concerns over affordability. The Real Clear Polling average for President Trump’s approval rating on the economy currently sits at 34.1 percent, which is particularly notable as inflation and the cost of living are the top concerns among American families. The Trump Administration’s continued ramping up of tariff policy with new Section 301 tariffs will not ease the affordability crisis and is likely to exacerbate the issue for import-reliant categories. The Shipment estimates that upcoming 301 tariffs will raise annual costs for businesses and consumers by roughly $58 billion, despite the administration’s consumer-facing tariff exemptions. Setting aside the economic costs, 47 percent of Americans want tariffs to be lowered compared to just 10 percent who want a higher tariff wall and 22 percent who want them to remain the same. Other polls show that nearly 60 percent of people disapprove of how the president is handling tariffs and trade policy, which is interconnected with inflation and the cost of living. The administration can learn from contrasting trade policies for two food products: eggs and tomatoes. The administration heavily promoted a 600-percent surge in egg imports to help solve skyrocketing U.S. egg prices, which have since plunged 65 percent since their May 2025 peak. Meanwhile a roughly 17-percent anti-dumping tariff was placed on Mexican tomatoes in July 2025, which make up 90 percent of fresh tomato imports and 60 percent of the total U.S. supply. While tariff costs are not the primary reason for the nearly 40-percent tomato price hike since July 2025, the more stringent trade policy is certainly a factor as tomato imports from Mexico fell 27 percent in 2025 and are down over 12 percent in 2026.

Looking Ahead: Inflation will stay elevated for the remainder of the conflict with Iran as traffic through the Strait of Hormuz remains well below pre-conflict levels. The on-again, off-again negotiations and military strikes that have been happened over the last few weeks mean there is still a great deal of uncertainty as to when the United States and Iran reach a lasting settlement. The United States economy is in a far better place than most others around the world due to booms in artificial intelligence investment and relative energy independence, but this is not enough to fully avoid the ramifications of a global economic downturn, recession, or a period of stagflation.

In Other News

Updates on USMCA: The United States-Mexico-Canada Agreement (USMCA) talks are becoming increasingly important as the summer review window comes to a close. The United States and Mexico – which held their first meeting in late May – plan to hold additional negotiating rounds June 16–17 in Washington, D.C. The United States and Canada have not yet engaged in formal negotiations, nor have Canada and Mexico held separate negotiations. The United States Trade Representative (USTR) recently noted that Canada’s retaliatory tariffs on U.S. exports – very rare among U.S. trade partners – represent a major hurdle in U.S.-Canada negotiations. The joint review deadline is set for July 1, 2026, but this can be considered more of an inflection point than a final deadline for all negotiations. This is because failure to reach a decision means the agreement remains active, but with an annual renewal cycle until its expiration in 2036. Just yesterday, on June 10, 2026, President Trump spoke to officials stating he may “not be looking to renew” the USMCA agreement. His comments came as the United States continues to run trade deficits with both Mexico and Canada. Despite President Trump’s latest remarks, Canada and Mexico have both previously extended support to renew the agreement with additional negations to improve the deal. If any country declines to confirm this extension, the agreement enters a cycle of annual reviews for the next decade.

Trade Deficit Update: The U.S. Census Bureau and the U.S. Bureau of Economic Analysis released the International Trade in Goods and Services Report finding that the goods and services deficit for April was down 1.2 percent compared to March. The trade deficit reduction was driven by a 2.6-percent increase in U.S. exports compared to a 2.0-percent increase in U.S. imports, explained partially by the sharp rise in the price of U.S. energy exports. On a year-to-date basis, the goods and services deficit decreased by more than $200 billion – 49.1 percent – compared to the same period in 2025 due to an 11.3-percent increase in exports and a 5.5-percent decrease in imports. Many factors are at play in these figures, including energy prices, precious metal prices, and U.S. tariff policies.

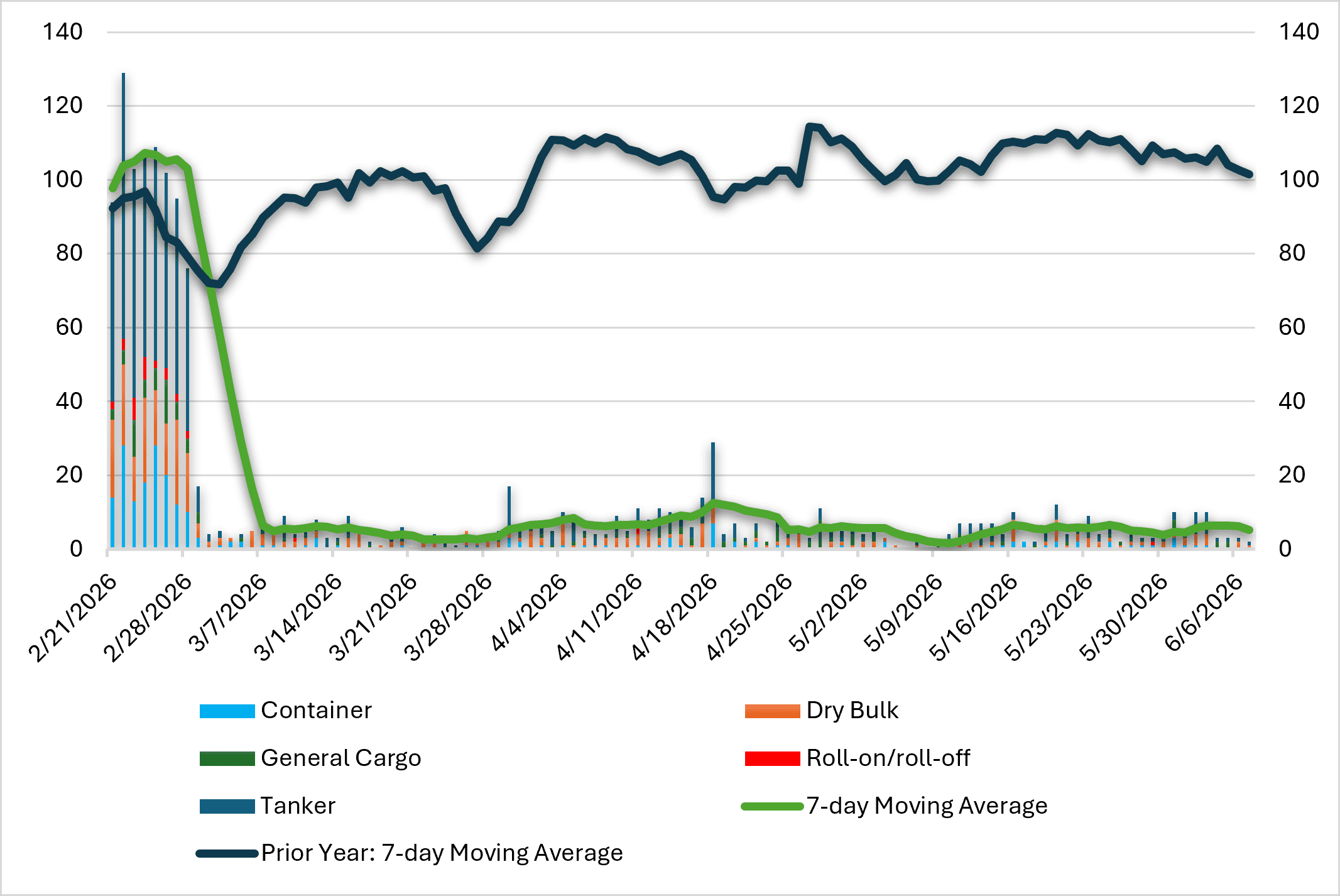

Oil Squeaks Out of the Strait of Hormuz: This week, President Trump announced that the U.S. military had secretly helped 200 ships and 100 million barrels of oil transit the Strait of Hormuz over the past month. This news partially explains why oil prices – while elevated – have remained relatively stable over the past few weeks despite 20 percent of global supply being seemingly offline. While this is beneficial for the global economy and energy prices, 100 million barrels represents about 16 percent of the normal oil volume in a typical month. Currently, reported transits through the strait remain around 5 percent of pre-conflict levels, as has been the case for weeks.

Figure 1: Strait of Hormuz Transit Calls by Number of Ships (Through June 7, 2026)