Weekly Checkup

July 2, 2026

Medicare’s $50 GLP-1 Promise Is Bigger Than It Looks

Policymakers like the word “bridge” because it suggests something narrow, temporary, and responsible: a way across a defined gap, not a new road. But the Medicare GLP-1 Bridge launched yesterday is more expansive than its modest name implies. It is not merely a short-term access program for a popular class of drugs. It is the federal government creating a low-price expectation for chronic obesity treatment before policymakers have resolved the permanent Medicare financing question.

The distinction is important. The point is not that Medicare shouldn’t pay for GLP-1s writ large. These therapies are clinically valuable for many beneficiaries. The problem is this: If policymakers believe these drugs belong in Medicare, they should be honest that this “bridge” will create a durable coverage expectation, and the resulting program will be expensive.

The program structure suppresses the market-based price signal beneficiaries see at the pharmacy counter. A $50 monthly copay is obviously more attractive than the cash price of these drugs. But the Bridge is not simply Part D coverage with a generous cost-sharing rule. The Centers for Medicare and Medicaid Services (CMS) states that the Part D deductible does not apply, the $50 payment does not count toward beneficiaries’ true out-of-pocket costs, and Low-Income Subsidy assistance does not apply.

That creates a consumer-cost wrinkle that should not be ignored. A beneficiary who remains on the therapy for the full 18-month demonstration would pay $900 out of pocket. For many seniors, that may be a good deal. For lower-income beneficiaries, a recurring $50 charge outside the Part D cap and outside LIS protections is significant. The Bridge may make GLP-1s less expensive for some, but it does not answer how beneficiary affordability should work if these drugs become a standard Medicare benefit.

The federal cost issue is larger. KFF estimates that 3.8 million Part D enrollees met all Bridge eligibility criteria using 2023 data. If 10–25 percent participate for the full 18 months, federal spending would be $1.3–$3.3 billion. At 50–75 percent participation, spending would rise to $6.7–$10 billion. Those numbers are already large for a temporary demonstration. But they are better understood as a floor than as a ceiling.

The universe of Medicare beneficiaries who may want or medically benefit from GLP-1s likely exceeds 3.8 million people. That narrow, claims-based estimate is filtered through the Bridge’s eligibility criteria and exclusions. KFF found that 13.3 million Medicare beneficiaries met BMI thresholds for obesity or overweight in 2023, and 9.7 million Part D enrollees met the Bridge’s clinical criteria. The estimate falls to 3.8 million only after excluding beneficiaries with certain diagnoses or prior GLP-1 use that could make them ineligible for the Bridge (covered instead by the real Part D benefit). KFF also notes that the obesity and overweight estimate may be conservative because not every beneficiary will have a claims-based diagnosis.

The Bridge estimate is an undercount bounded by temporary rules, a temporary timeline, and 2023 claims data. Coverage eligibility could expand. Uptake could rise. Prescribers could become more comfortable. Beneficiaries could become more aware. New indications could move additional patients into coverage. Oral formulations or improved supply could reduce practical barriers to use. None of that is speculative; Medicare is already seeing rapid GLP-1 growth for currently covered uses. Gross Part D spending on GLP-1s reached $27.5 billion in 2024, a five-fold increase from 2019; GLP-1 claims rose from 4.8 million to 21.8 million over the same period.

The Congressional Budget Office’s (CBO) broader work points in the same direction. It estimated that authorizing Medicare coverage of anti-obesity medications would increase federal spending by about $35 billion from 2026 to 2034, with direct federal costs rising from $1.6 billion in 2026 to $7.1 billion in 2034. CBO also found that expected health savings would be small relative to the direct cost of the medications within that budget window.

Demographics will make the issue harder, not easier. The number of Americans age 65 and older grew from 43.1 million in 2012 to 57.8 million in 2022 and is projected to reach 78.3 million in 2040 and 88.8 million in 2060. Even if prices, eligibility rules, and obesity prevalence remain unchanged, a larger Medicare population means a larger potential coverage base. Those variables are unlikely to remain fixed.

Therefore, the Bridge will not be as temporary as its name implies. GLP-1 therapy is a long-term, chronic therapy intervention. At an entry price of $50 per month, the expiration of the program becomes a patient-facing cliff and a political forcing event. That is the quandary CMS is creating: Ending the Bridge would disrupt access, extending it would increase federal exposure, and moving coverage into Part D would raise hard questions about benefit design, premiums, and legal authority.

The Bridge may be defensible as a limited experiment. But policymakers should not mistake a temporary demonstration for a permanent financing strategy. If the full complement of GLP-1 indications belongs in Medicare (and it very well may given therapeutic promise), Congress and CMS should define the benefit, decide who qualifies, protect beneficiaries transparently, and admit that the bill will be large. A $50 copay may be the number seniors see. It is not the real price of coverage.

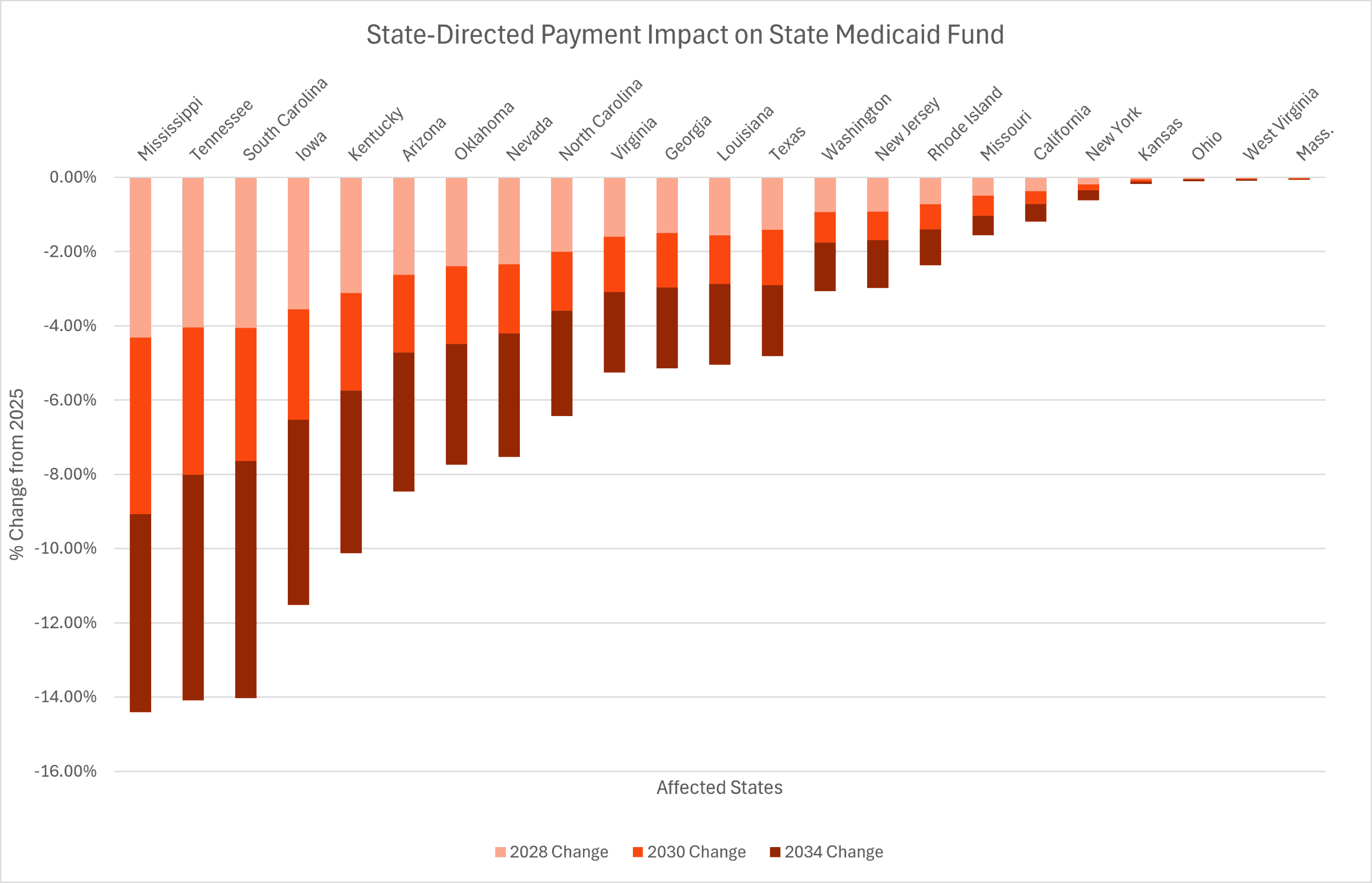

Chart Review: Impact of State-directed Payment Reform on Medicaid Funding

Evan McLaughlin, Health Policy Intern

The One Big Beautiful Bill Act (OBBBA), signed into law July 4, 2025, is projected to reduce federal Medicaid spending by approximately $724 billion below previous projections over the next decade; $169 billion of these savings are through reforms to state-directed payments (SDPs) alone. SDPs are financing arrangements that allow states to direct Medicaid managed care organizations to make additional payments to hospitals, nursing facilities, physicians, and other providers beyond standard reimbursement rates. These payments are intended to help providers improve access to care and support quality improvements.

Because the federal government matches a portion of Medicaid spending, the rapid expansion of SDPs has substantially increased federal Medicaid expenditures, with SDP spending reaching nearly $100 billion in 2024. The OBBBA caps SDPs for inpatient and nursing facilities at 100 percent of the Medicare payment rate in states that expanded Medicaid under the Affordable Care Act, and at 110 percent in states that did not. Existing SDPs are exempt from new payment limits until January 1, 2028, after which the total payment amount will be reduced by 10 percent each year until reaching the applicable Medicare-based limit.

The OBBBA reform will be felt most acutely in states with robust SDP programs. Recent RAND analysis projects that these SDP reductions represent a $241-billion decrease in total state Medicaid funding over the next decade. In that period, Mississippi, Tennessee, and South Carolina are projected to see the biggest reductions in their state Medicaid funds, in the range of 14–15 percent.