The Shipment

July 24, 2025

Tariffs Still Real in U.S. Trade Deals

(Not So) Fun Fact: Another round of trade talks between the United States and China is set to take place in Sweden from July 27–30, coming roughly two weeks before the current August 12 tariff pause deadline.

Three Trade Deals in One Day but Tariffs Remain High

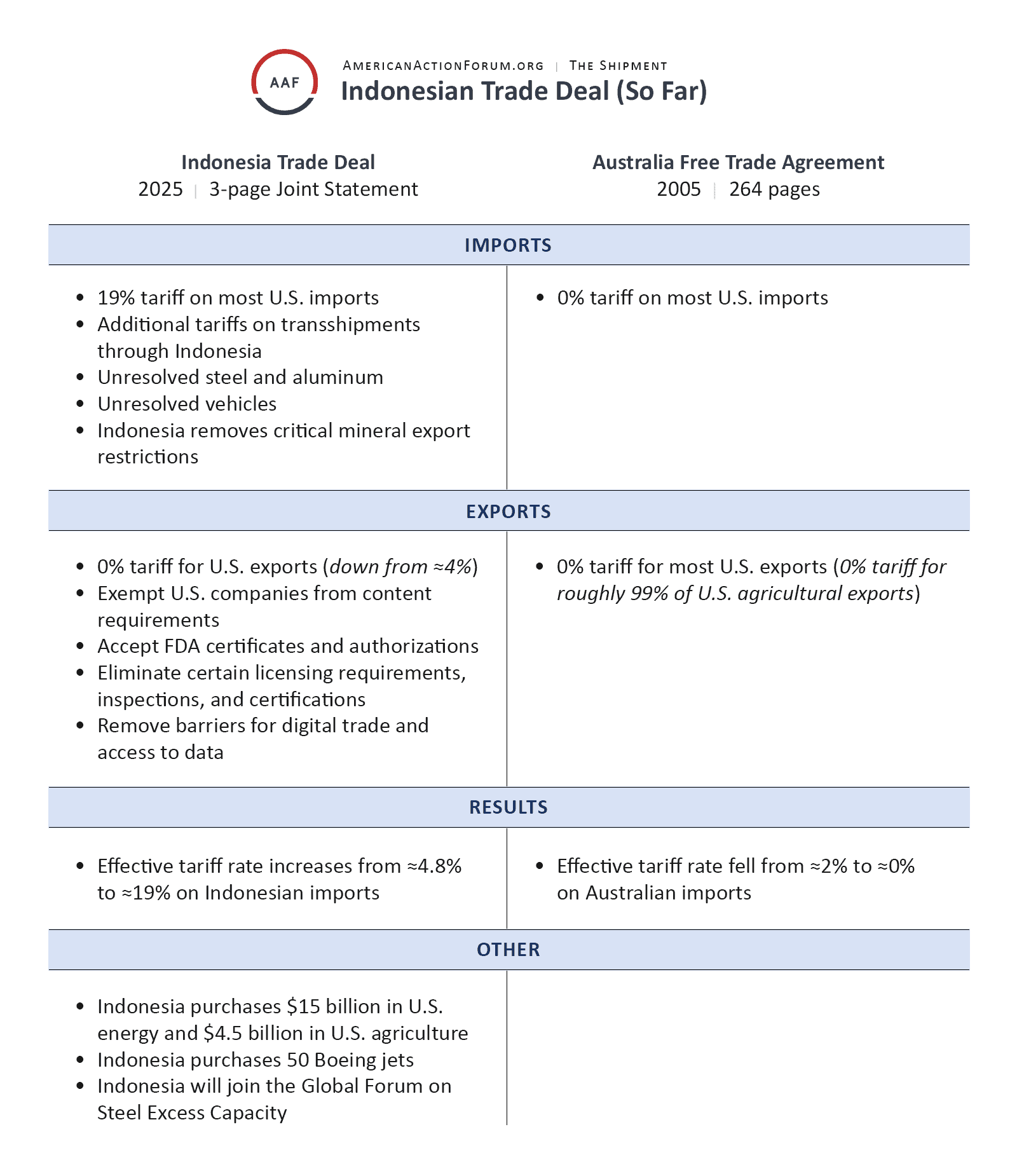

What’s Happening: President Trump announced a trade deal with Japan Tuesday night, coming just a day after an election in which the Japanese prime minister lost a ruling majority. According to the president’s post, Japan has agreed to invest $550 billion in the United States and open its markets to U.S. exports. The United States, in return, agreed to lower its baseline tariff, as well as the tariff on Japanese automobiles, from 25 to 15 percent. Another deal was struck earlier on Tuesday, when Philippine President Ferdinand Marcos Jr., in a White House meeting, agreed to open markets to U.S. exports and eliminate tariffs. In the same meeting, the United States lowered its tariff from 20 to 19 percent and reiterated a commitment to greater cooperation. In an interesting – if not widely publicized – sidenote, a day later, Secretary of State Rubio announced $60 million in foreign aid for the country. Finally, the Indonesia trade deal was brought back into the spotlight despite it being struck a week ago. While there are no new terms to the agreement, there is now an official joint statement and fact sheet published on the White House website that provide more detail and clarity as to what non-tariff barriers may finally be addressed going forward.

Why It Matters: Factoring in the recent reductions in tariff rates and the tariff letters that are expected to take effect on August 1, the Shipment estimates the annual cost of “Liberation Day” part two for U.S. consumers and businesses to be just over $400 billion. This cost estimate is higher than previous research, which put the cost of “Liberation Day” tariffs between $366.5–$391.6 billion, due mainly to the larger 30-percent tariff on the European Union (EU). The three recent trade deals are a step in the right direction in lowering the effective tariff rate of the United States, although they maintain a relatively high tariff baseline that will eventually have a negative impact on the U.S. economy. It is fair to say that these deals are small steps toward opening up market access for U.S. firms, and specifically the terms laid out for Indonesia, which should reduce non-tariff barriers if implemented (see the chart below). At the same time, it is fair to point out that these deals are not truly reciprocal. If the United States has a 19-percent tariff while Indonesia plans on eliminating its tariffs, there is an obvious imbalance to the detriment of U.S. consumers who will end up facing higher prices.

Examining the Japanese trade deal more closely, some interesting questions and concerns arise. Details of Japan’s $550 billion investment remain scarce, with no industries outlined or timeline declared. President Trump’s initial post declared that the United States would receive “90 percent of the profits” from this investment. This could mean the U.S. government will somehow be receiving profits from whichever Japanese companies begin new projects in the United States, a major shift for a market economy. It could also mean that the Japanese government itself will invest in some way, which would essentially amount to a transfer payment from Japan, one of the most indebted countries in the world. A later post declared that the United States would receive 90 percent of the $550 billion investment, with no mention of profits. Commerce Secretary Lutnick stated that this investment amounts to a fund for U.S. projects that President Trump will oversee. On another note, the lowering of tariffs on automobile imports from Japan was a major announcement as this represents the first reduction of a Section 232 tariff thus far. Put simply, tariffs on autos, steel, aluminum, copper, and pharmaceuticals may be negotiable going forward. It also means that Japanese automakers will be better positioned to sell in the U.S. market than U.S. automakers that manufacture abroad and import their products.

Looking Ahead: The August 1 tariff pause deadline is next week. As of today, there are five deals on the books, none of which include top trade partners or tariffs below 10 percent. Deals with the EU, Canada, and Mexico remain to be seen while South Korea is in the midst of trade talks today. Both the EU and Canada have retaliatory tariffs at the ready in the event trade talks fall through, which includes a 30-percent tariff on over $100 billion in U.S. exports to the EU. In weeks past, the EU was willing to accept a 10-percent tariff baseline as long as certain sectors were given lower rates. Reports yesterday indicate that there is progress toward a U.S.-EU trade deal that results in a 15-percent tariff baseline for EU products, with no mention of specific sectors although carve-outs are likely. Information regarding the status of negotiations has been ever changing, so stay tuned.

![]()