The Shipment

May 14, 2026

Tariff Court Cases and China Trade Negotiations

(Not So) Fun Fact: The recent ruling against the Trump Administration’s Section 122 tariffs – initially applied to just three importers – has been paused until the higher courts produce a ruling that may apply to importers more broadly.

Another Day, Another Tariff Regime in Limbo

What’s Happening: On May 7, the U.S. Court of International Trade ruled against the Trump Administration’s 10-percent Section 122 tariffs, stating in a 2–1 decision that these tariffs have been unlawfully imposed. The court explained that the administration has failed to adequately identify a balance-of-payments deficit, which is required by law in order to impose tariffs under Section 122. Instead, the administration justifies these tariffs by pointing primarily to the merchandise trade deficit, ignoring the flow of payments and investments that go the other way (read here for more info). Notably, the court chose to apply the ruling only to the three importers with standing in this specific case, meaning they would be exempt from 122 tariffs and entitled to refunds. On May 8, the Trump Administration announced that it appealed the ruling, sending the case to the U.S. Court of Appeals for the Federal Circuit. On May 11, the appeals court decided to temporarily pause the trade court’s ruling, thereby keeping Section 122 tariffs in place for all importers until the case moves up the ladder. For now at least, this follows the same pattern as the previous International Emergency Economic Powers Act (IEEPA) tariffs which were rejected by the court of appeals before the case eventually reached the Supreme Court. While the trade court ruling applied to just the few importers involved in the case, it is possible the appeals process produces a ruling that applies more broadly.

Why It Matters: Although the ruling from the U.S. Court of International Trade is now temporarily paused, it likely represents the first nail in the coffin of the Trump Administration’s second tariff regime. The Shipment expects the Section 122 tariffs to follow a similar trajectory as the previous IEEPA regime which was unanimously (3–0) struck down by the U.S. Court of International Trade, ruled against again by the U.S. Court of Appeals for the Federal Circuit (7–4), and finally ruled unconstitutional by the Supreme Court (6–3). The current 122 tariff regime was always meant to be a temporary response to the end of IEEPA since Section 122 tariffs have a 150-day limit. Unless Congress renews these (an unlikely prospect), all Section 122 tariffs are set to expire in July regardless of what a higher court might decide in the near future. The focus will now be on whether the court of appeals or Supreme Court rule against the administration’s use of Section 122 to include all U.S. importers, opening the door for universal refunds in a similar fashion to the current IEEPA refund process.

The Shipment estimates that Section 122 tariff costs (and future refunds) could amount to approximately $25–$30 billion (assuming the tariff regime remains in place for the full 150 days). Other estimates include We Pay the Tariffs which suggests that U.S. businesses paid close to $8 billion in March alone. GHY – a brokerage provider – puts total Section 122 tariff collections at $25 billion over 72 days of implementation. If these estimates hold true, future Section 122 tariff refunds could total up to $50 billion. Initially, the three importers with standing in the case were expected to receive refunds (with interest), but they are now expected to continue paying tariffs until the higher courts make a final ruling. Based on the court filing, the Shipment expected their refunds would be less than $1 million in total. This just scratches the surface of the Section 122 tariff regime which puts significant weight on whether the higher courts apply a final ruling to all importers impacted by Section 122 tariffs.

Looking Ahead: The end of the administration’s Section 122 tariff regime is almost certainly near, as it is scheduled to end on July 24 – barring unexpected congressional action or legal chicanery from the Trump Administration to try to reimpose these duties. If the legal case against IEEPA is any indication, it may be a long road ahead before the fate of Section 122 refunds is decided. It took 93 days between the Court of International Trade’s ruling on IEEPA and the decision from the U.S. Court of Appeals for the Federal Circuit. It then took 68 days more for the Supreme Court to hear the case and an additional 107 days before IEEPA was finally struck down. Assuming a similar timeline, U.S. importers might not find clarity until January 2027. In the meantime, importers may have to file their own cases against the government to find Section 122 tariff relief.

The Long-awaited U.S.-China Meeting Comes at Last

What’s Happening: President Trump landed in China on Wednesday to discuss with Leader Xi matters ranging from bilateral trade relations to recent geopolitical developments. This marks the first meeting between the two since last October when they held a summit in South Korea that resulted in a one-year trade war truce. This follow-up between the world’s largest economies comes after a few delays due to the U.S.-Iran conflict – a topic that has already come up as both parties seek to reopen the Strait of Hormuz free from attacks or tolls. From what has been reported so far, Xi has told the CEOs who arrived with Trump that “China’s door will only open wider” to U.S. companies. This comes alongside reports that the two countries are discussing a joint “board of investment” as well as a “board of trade,” both of which may manage future bilateral economic ties. Additionally, China may end up purchasing planes from Boeing, as well as energy and agricultural products – a process the country has already begun by restoring licenses for U.S. beef shipments. It is unclear what President Trump might provide Xi in return for certain Chinese purchase commitments; it is possible, however, that tariff cuts on $30 billion worth of imports may be coming.

Why It Matters: When the trade truce was struck during the last meeting, several concessions were made to maintain normalcy in the U.S.-China economic relationship. The United States dropped some International Emergency Economic Powers Act (IEEPA) tariffs, put certain Section 301 investigations on hold, refrained from placing port fees on Chinese ships, and removed Chinese companies from the U.S. Entity List. In return, China reversed its export controls on rare earths, suspended the 15–24 percent retaliatory tariffs on certain U.S. imports, refrained from placing its own port fees on American ships, and imposed new export controls on precursor chemicals used to produce fentanyl. This time around, the cards at play are slightly different. China maintains its mining, manufacturing, and refining dominance over rare earths and related battery components, but various countries have made a concerted effort to reduce reliance on China for critical minerals. While it will take years for the United States and its allies to develop a separate supply chain, China almost certainly realizes that if it does not make efforts to keep countries reliant on these resources it will lose this negotiating leverage going forward. At the same time, the United States is still the world’s largest market for China, yet over the past year China has been expanding trade with other countries to fill the potential U.S. void. Despite U.S. tariff threats, other countries have struck trade agreements to grow more economically connected to China, meaning the United States may slowly lose its ability to rely on market power as leverage.

The end of IEEPA tariffs has limited President Trump’s immediate negotiating leverage over China, meaning the fentanyl and “Liberation Day” tariffs can no longer be dropped in exchange for concessions. The administration will have to rely almost entirely on impending Section 301 investigations if it seeks to use a tariff bargaining chip. The military actions taken by the United States this year have also changed the negotiating calculus. In the past, China received close to 15 percent of its oil from Iran and another 4 percent or so from Venezuela. Iranian exports have now come to a relative standstill, and Venezuelan oil exports are now heavily influenced by U.S. policy. With the Strait of Hormuz closed, an additional 40 percent of Chinese oil imports from Gulf countries are virtually cut off. At the moment, the United States is the only country that can allow Iranian exports to flow or potentially reopen the strait (militarily or through diplomacy), which may provide an opportunity during Trump-Xi talks. It is likely that China will commit to purchasing more U.S. goods as President Trump is particularly keen on reducing U.S. trade deficits with China. These goods will most likely be agricultural products such as beef, soybeans, and potentially industrial equipment but it is also possible that China commits to purchase more U.S. energy out of growing necessity and uncertainty in the Middle East.

Looking Ahead: The Shipment expects there to be some sort of announcement from President Trump following the conclusion of talks in China this week. Whether the announcement is a substantive shift in U.S.-China economic relations or a minor footnote in a continued trade truce remains to be seen. In the past, China has agreed to purchase more from the United States – soybeans, for instance – but failed to live up to its end of the bargain. Thus, the administration will need to closely monitor any commitment made by China in these negotiations going forward.

Figure 1: U.S. Trade with China (January 2024–March 2026)

Source: United States International Trade Commission

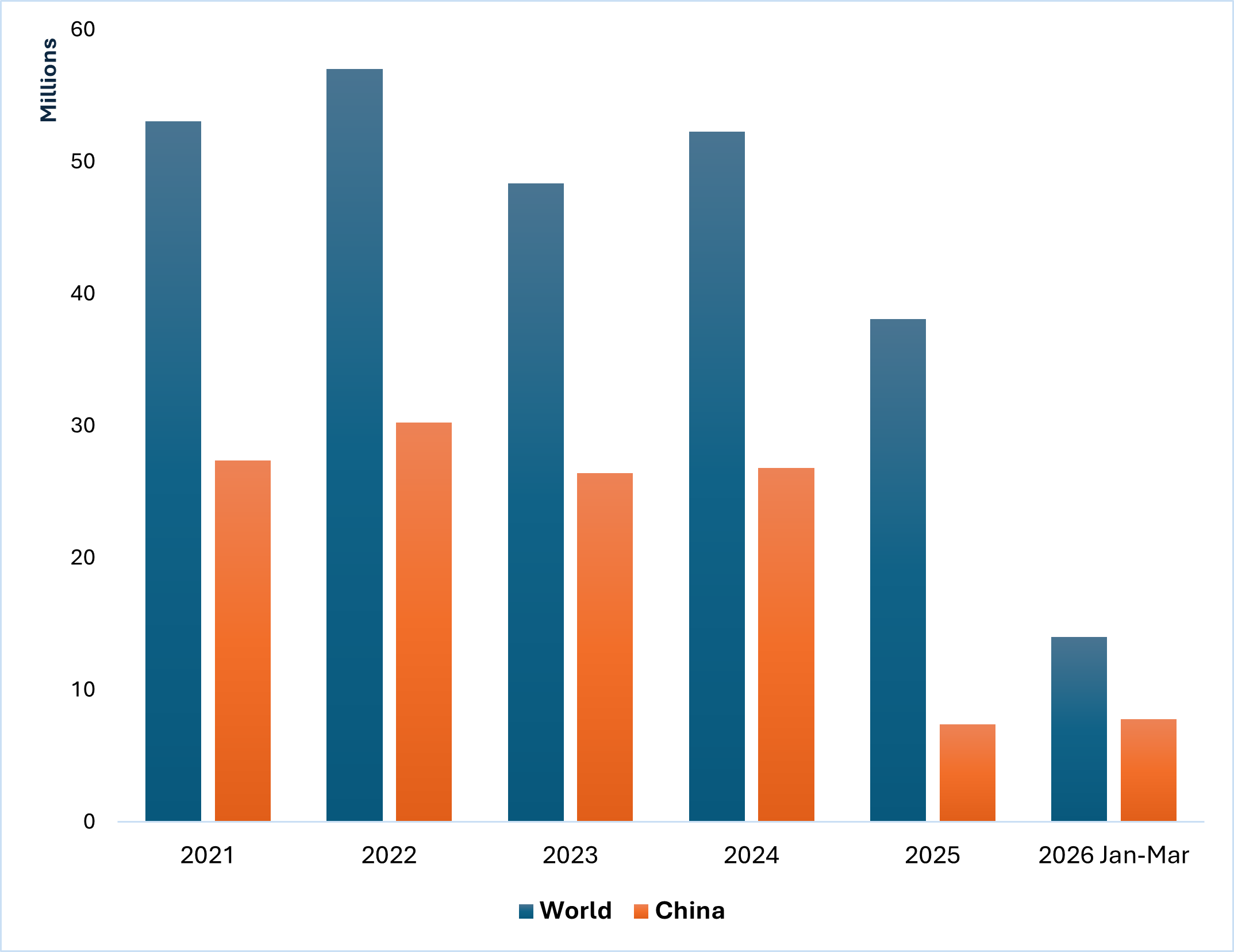

Figure 2: U.S. Exports of Soybeans

Source: United States International Trade Commission

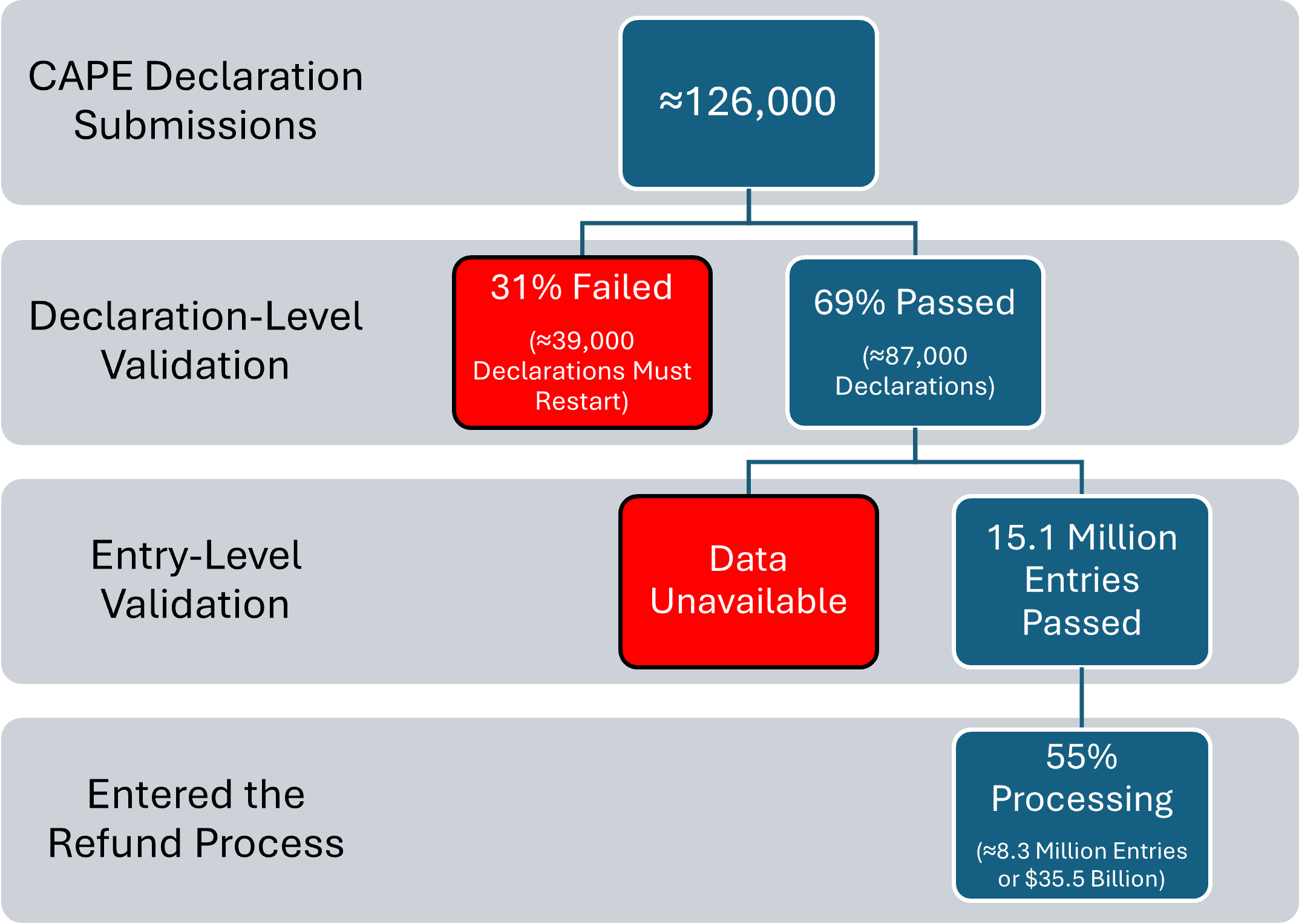

Figure 3: Status of the IEEPA Tariff Refund Process (As of May 11, 2026)

Source: United States Court of International Trade Court Filings