Weekly Checkup

June 22, 2018

Association Health Plans: There’s No Devil in the Details

This week the Department of Labor rolled out a final rule expanding access to Association Health Plans (AHPs). AHPs allow various groups—say, plumbers in the Chicago metro area—to join together, potentially across state lines, for the purpose of getting a better deal on health insurance. The rulemaking is part of the administration’s efforts to make good on President Trump’s October 2017 executive order aimed at “promoting choice and competition” in the health insurance market. What should we make of this change?

In a statement accompanying the release of the final rule, Secretary of Labor Alexander Acosta praised the president for “expanding affordable health coverage options for America’s small businesses and their employees,” and declared that “Association Health Plans are about more choice, more access, and more coverage.” On the other hand, The New York Times warned in a headline that the “New Trump Rule Rolls Back Protections of the Affordable Care Act.” Senate Minority Leader Chuck Schumer, quoted in the same piece, argued that the new rule would lead to “junk health insurance” returning to the market place and that the rule is “the latest act of sabotage of our health care system by the Trump administration.”

So, are AHPs a threat to quality health care in America? Hardly. AHPs are, in effect, a way of bringing the same type of health insurance available to the employees of large employers to small businesses and the self-employed. AHPs are regulated in the same way as the large group insurance market. No one argues that insurance obtained through the employer-sponsored large group is junk insurance, so it’s at best a stretch to suggest so about AHPs.

There are, however, some reasonable concerns about AHPs. For one, states will need to be vigilant in their oversight to ensure those sponsoring AHPs can actually meet their obligations. Insurers raise valid points about the potential for abuse by fly-by-night operators. More important, there are legitimate concerns from some quarters that if AHPs are successful, they could remove healthy, low-risk enrollees from ACA Exchange plans, further eroding the stability of that market and increasing premiums for the remaining individuals. Yet it seems that AHPs would be more attractive to enrollees (and small employers) who are currently using the Small Business Health Insurance Program (better known as SHOP) exchange to obtain coverage. That marketplace never really took off, and if AHPs siphon off enrollees from it, that won’t effect the individual market Exchanges.

The potential results of AHPs on the individual market are hard to predict, but they certainly could influence the risk pool for the worse. The answer, however, is not to block AHPs. Rather, policymakers should implement a robust reinsurance program or other risk mitigation tools in the ACA Exchanges to offset any negative effects—a policy that would be a positive addition to the marketplace even in the absence of AHPs.

Chart Review

Tara O’Neill Hayes, Deputy Director of Health Care Policy

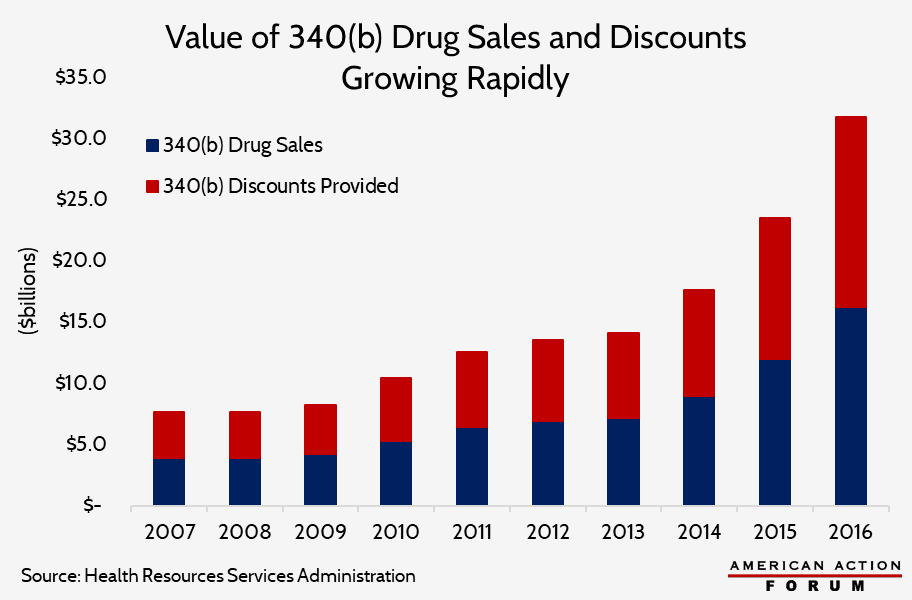

The 340(b) drug discount program has grown rapidly over the past several years, primarily due to the Affordable Care Act’s (ACA) expansion of the program’s eligibility requirements. As a result, the cost of the discounts also has grown dramatically. This growth and other changes in the ACA that increased costs and reduced revenues for drug manufacturers are likely key drivers of the increased drug prices observed in the years since the ACA’s implementation, as explained here.

From Team Health

Understanding the Policies that Influence the Cost of Drugs – Tara O’Neill Hayes correlates the implementation of several Affordable Care Act policies with rising drug prices and explains how these policies likely contributed to the price growth.

Worth a Look

RealClearHealth: Health Care Transparency Deserves a Serious Bipartisan Effort

Axios: Minnesota may see ACA premiums drop