Weekly Checkup

August 3, 2018

Sizing Up Short-Term Insurance

You could be forgiven for thinking that President Trump had delivered a body blow to the Affordable Care Act (ACA) earlier this week when his administration announced a final rule allowing the expanded sale of short term, limited duration plans (STLDs). The reaction from certain corners of the left was practically apocalyptic, while on the right some were similarly too grand in stating the benefits of the changes. The reality is that these changes represent a responsibly measured effort by the administration to help uninsured individuals for whom the ACA doesn’t provide a particularly viable option.

As discussed previously in the Weekly Checkup, STLDs typically provide temporary coverage for individuals who have a break in traditional health insurance for a limited period. Because these plans are outside of the ACA’s regulatory framework, however, they don’t have to conform to the ACA’s rules regarding benefit design and coverage requirements. They also aren’t subject to the ACA’s guaranteed issue requirements or the ban on preexisting condition exclusions.

Under Obama Administration rules, STLDs were restricted to a duration of less than three months, and insurers were barred from renewing them when they expired. The Trump Administration is allowing STLDs to be issued for up to 364 days. Additionally, and importantly, STLDs will now be renewable—at the discretion of the issuer—for up to 36 months.

ACA supporters are concerned STLDs could attract healthy individuals who are currently purchasing coverage on the exchanges, thereby worsening the risk pool. One reason for this fear is that the administration anticipates premiums for these plans will be 50 to 80 percent lower than unsubsidized rates on the exchanges. Most people purchasing insurance through the exchange today, however, are receiving a subsidy, making the lower, but unsubsidized, premium of STLDs less appealing than one might expect. Additionally, the coverage itself is far less generous than what is offered on the exchanges. The Trump Administration has rightly argued that individuals with significant medical needs are unlikely to find this coverage attractive. It’s also worth noting that the number of subsidy-ineligible individuals who have enrolled through the ACA exchanges has steadily declined as premiums have increased. Those who are still purchasing ACA coverage without a subsidy are likely in need of robust coverage, which means they will not be eager to purchase these plans.

AAF’s Jonathan Keisling has summarized a number of studies examining the effect of these plans on the individual market, both on and off the exchanges. While there are some differences in the studies, in general they indicate that between .3 and 5.2 million people will purchase these plans, increasing the total number of people insured in the individual market by between .1 and 2.3 million. Further these plans could result in an average increase in non-STLD plan premiums in the individual market of between 2 and 10 percent.

The expansion of STLDs offers a new choice for people seeking a degree of protection against unforeseen health needs but for whom ACA coverage is cost prohibitive. But the appeal of these plans beyond this group to those already insured will likely be limited.

Chart Review

Tara O’Neil Hayes, Deputy Director of Health Care Policy

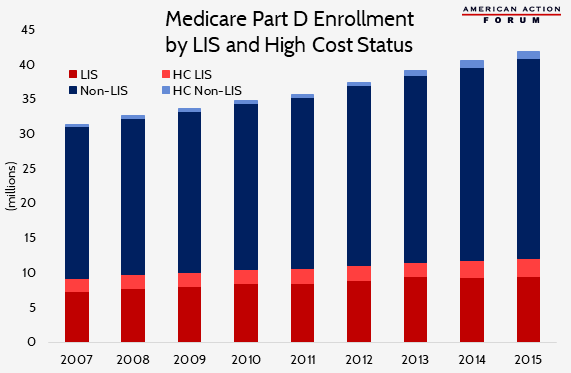

Medicare Part D beneficiaries not eligible for a low-income subsidy (LIS) still account for less than 30 percent of all Part D high-cost enrollees (those beneficiaries who reach the catastrophic coverage phase of their plans). But the share of non-LIS beneficiaries reaching catastrophic coverage has grown much more quickly over the past several years than that of LIS beneficiaries: 21 percent since 2010 versus 6 percent. This difference is not entirely surprising, given that enrollment growth in the Part D program has been greater among non-LIS than LIS individuals: 22 percent compared with 16 percent.

Worth a Look

New York Times: Meet the Rebate, the New Villain of High Drug Prices

Axios: Trump’s effect on ACA premiums